Вам также может понравиться

- Principles of Taxation I SyllabusДокумент7 страницPrinciples of Taxation I SyllabusShreyaОценок пока нет

- Right To PrivacyДокумент4 страницыRight To PrivacyShreyaОценок пока нет

- Admin Law ProjectДокумент1 страницаAdmin Law ProjectShreyaОценок пока нет

- Chapter 9 Ratio Analysis PDFДокумент65 страницChapter 9 Ratio Analysis PDFahmadfaiq01Оценок пока нет

- Internship DetailsДокумент1 страницаInternship DetailsShreyaОценок пока нет

- Crpc-Production of Documents// Section 91 and 92 Pil - Brexit Company - Class Action Suits Evidence - Jesica Lal Case Administration - Delhi Haus Khas ActДокумент1 страницаCrpc-Production of Documents// Section 91 and 92 Pil - Brexit Company - Class Action Suits Evidence - Jesica Lal Case Administration - Delhi Haus Khas ActShreyaОценок пока нет

- Chapter 9 Ratio AnalysisДокумент12 страницChapter 9 Ratio AnalysisShreyaОценок пока нет

- Internship DetailsДокумент1 страницаInternship DetailsShreyaОценок пока нет

- Article 23 prohibits traffic in human beings and forced labourДокумент5 страницArticle 23 prohibits traffic in human beings and forced labourShreyaОценок пока нет

- Internship DetailsДокумент1 страницаInternship DetailsShreyaОценок пока нет

- JurisdictionДокумент2 страницыJurisdictionShreyaОценок пока нет

- NMIMS college sports teams contact listДокумент4 страницыNMIMS college sports teams contact listShreyaОценок пока нет

- Critical ThinkingДокумент3 страницыCritical ThinkingShreyaОценок пока нет

- Taxes To Be Subsumed Under GSTДокумент3 страницыTaxes To Be Subsumed Under GSTShreyaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Karnataka Police Establishment BoardДокумент64 страницыKarnataka Police Establishment BoardxfilesindiaОценок пока нет

- ICICI Bank FE West India Online AuctionДокумент15 страницICICI Bank FE West India Online AuctionAnonymous rtDlncdОценок пока нет

- Order in The Matter of Exelon Infrastructure LimitedДокумент22 страницыOrder in The Matter of Exelon Infrastructure LimitedShyam SunderОценок пока нет

- Financial Accounting: A: How To Study AccountingДокумент29 страницFinancial Accounting: A: How To Study Accountingrishi_positive1195Оценок пока нет

- Chapter 05 Quiz Audit EvidenceДокумент26 страницChapter 05 Quiz Audit EvidenceAly Arce100% (1)

- BSBSTR801 Lead Innovative ThinkingДокумент4 страницыBSBSTR801 Lead Innovative ThinkingFasih ur Rehman Abid0% (1)

- Marketing Group 3 - Vietjet AirДокумент10 страницMarketing Group 3 - Vietjet AirAnhОценок пока нет

- Venture Capital Firms in SoCalДокумент4 страницыVenture Capital Firms in SoCalmcarney7100% (1)

- Greene Vs MtGox Preliminary Injunction 8 April 2014Документ354 страницыGreene Vs MtGox Preliminary Injunction 8 April 2014Peter N. SteinmetzОценок пока нет

- PT Kabelindo Murni TBK.: Summary of Financial StatementДокумент2 страницыPT Kabelindo Murni TBK.: Summary of Financial StatementIshidaUryuuОценок пока нет

- RN170907113212734 RpuДокумент13 страницRN170907113212734 RpunadiaОценок пока нет

- Divya Pandya NNДокумент29 страницDivya Pandya NNKrishnaОценок пока нет

- General Environment AnalysisДокумент2 страницыGeneral Environment AnalysisClio Margaret CuevasОценок пока нет

- 66 India Post Case StudyДокумент3 страницы66 India Post Case StudySameer GopalОценок пока нет

- Interim Report On CCLДокумент9 страницInterim Report On CCLanitasingh_kumari5Оценок пока нет

- Average Costing in Oracle R12 EBS SuiteДокумент26 страницAverage Costing in Oracle R12 EBS Suitehsk12100% (1)

- Steinway & SonsДокумент6 страницSteinway & Sonsbilal khanОценок пока нет

- General Electric's Joint VenturesДокумент8 страницGeneral Electric's Joint VenturesRounaq JunejaОценок пока нет

- Application for Assistant Manager Production RoleДокумент4 страницыApplication for Assistant Manager Production RolePuneeth Shetty KnightmarainezzОценок пока нет

- ITC Limited: One of India's Most Admired and Valuable CompanyДокумент23 страницыITC Limited: One of India's Most Admired and Valuable Companykapil gargОценок пока нет

- Hindustan Zinc Limited - Tanisha 08351Документ4 страницыHindustan Zinc Limited - Tanisha 08351Tanisha KalraОценок пока нет

- Tally Acc TermsДокумент22 страницыTally Acc TermsShekhar Chandra SahuОценок пока нет

- Ostriches, Wilful Blindness, and AML/CFTДокумент3 страницыOstriches, Wilful Blindness, and AML/CFTAlan PedleyОценок пока нет

- Rulings2000 DigestДокумент21 страницаRulings2000 DigestArriane MartinezОценок пока нет

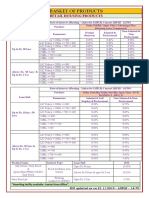

- BASKET OF RETAIL PRODUCTS RATESДокумент3 страницыBASKET OF RETAIL PRODUCTS RATESVirendra K VermaОценок пока нет

- HKSRS 4400 Procedures Financial InformationДокумент8 страницHKSRS 4400 Procedures Financial InformationAgus WijayaОценок пока нет

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Документ3 страницыPhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)Mary Jo Lariz OcliasoОценок пока нет

- Ryanair'S Quality: Rajiv Babu ChintalaДокумент11 страницRyanair'S Quality: Rajiv Babu ChintalaexpairtiseОценок пока нет

- Lista de Empresas Bolivianas Vinculadas en El Caso Panamá PapersДокумент6 страницLista de Empresas Bolivianas Vinculadas en El Caso Panamá PapersLos Tiempos DigitalОценок пока нет

- EEDC Tech InnovationДокумент57 страницEEDC Tech InnovationEmily MertzОценок пока нет