Вам также может понравиться

- Fnce 100 Final Cheat SheetДокумент2 страницыFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Corporate Finance Formulas: A Simple IntroductionОт EverandCorporate Finance Formulas: A Simple IntroductionРейтинг: 4 из 5 звезд4/5 (8)

- Definition of WACCДокумент6 страницDefinition of WACCMMОценок пока нет

- Final exam: Answers to recommended end of chapter questionsДокумент13 страницFinal exam: Answers to recommended end of chapter questionsRajiv KumarОценок пока нет

- Capital Asset Pricing Model Written ReportДокумент7 страницCapital Asset Pricing Model Written Reportgalilleagalillee0% (1)

- Weighted Average Cost of CapitalДокумент12 страницWeighted Average Cost of CapitalJose Arnaldo100% (4)

- Portfolio Management 1Документ28 страницPortfolio Management 1Sattar Md AbdusОценок пока нет

- Chap 011Документ5 страницChap 011dt830280% (5)

- CML Vs SMLДокумент9 страницCML Vs SMLJoanna JacksonОценок пока нет

- SOLTEK SOLAR POWER Specification and PriceДокумент4 страницыSOLTEK SOLAR POWER Specification and PriceAlexis MalicdemОценок пока нет

- LauretaДокумент2 страницыLauretaAsh Manguera50% (2)

- The Capital Asset Pricing ModelДокумент43 страницыThe Capital Asset Pricing ModelTajendra ChughОценок пока нет

- Asset PricingДокумент23 страницыAsset PricingBrian DhliwayoОценок пока нет

- Chapter 23 - AnswerДокумент11 страницChapter 23 - AnswerwynellamaeОценок пока нет

- SIMP-40Документ26 страницSIMP-40Ishtiaq Hasnat Chowdhury RatulОценок пока нет

- FIN352 Part2 Answrs TextДокумент16 страницFIN352 Part2 Answrs TextChessking Siew HeeОценок пока нет

- Cost of Capital, WACC and BetaДокумент3 страницыCost of Capital, WACC and BetaSenith111Оценок пока нет

- NT 3 Financial Leverage and WACCДокумент14 страницNT 3 Financial Leverage and WACCCarmenОценок пока нет

- Calculation of Beta in Stock MarketsДокумент35 страницCalculation of Beta in Stock Marketsneha_baid_1Оценок пока нет

- L1 R50 HY NotesДокумент7 страницL1 R50 HY Notesayesha ansariОценок пока нет

- Markowitz ModelДокумент17 страницMarkowitz ModelgultoОценок пока нет

- Northwestern University J.L. Kellogg Graduate School of ManagementДокумент52 страницыNorthwestern University J.L. Kellogg Graduate School of ManagementlatecircleОценок пока нет

- A 109 SMДокумент39 страницA 109 SMRam Krishna KrishОценок пока нет

- Ch11 Solutions 6thedДокумент26 страницCh11 Solutions 6thedMrinmay kunduОценок пока нет

- Tax Shields and Discount RatesДокумент126 страницTax Shields and Discount RatesArjun M PОценок пока нет

- Seminar 5Документ6 страницSeminar 5vofmichiganrulesОценок пока нет

- Jawaban Buku ALK Subramanyam Bab 7Документ8 страницJawaban Buku ALK Subramanyam Bab 7Must Joko100% (1)

- Textbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Документ13 страницTextbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Atif SaeedОценок пока нет

- Risk and Return Review LectureДокумент42 страницыRisk and Return Review LectureFarmmy NiiОценок пока нет

- Cost of Capital Mahindra - Sohanji - FinalДокумент21 страницаCost of Capital Mahindra - Sohanji - FinalJaiprakash PandeyОценок пока нет

- Portfolio InvДокумент5 страницPortfolio InvDullah AllyОценок пока нет

- FINALS Investment Cheat SheetДокумент9 страницFINALS Investment Cheat SheetNicholas YinОценок пока нет

- In FinanceДокумент8 страницIn FinanceSsahil KhanОценок пока нет

- Chapter 3Документ32 страницыChapter 3Thanh PhamОценок пока нет

- FM 8th Edition Chapter 12 - Risk and ReturnДокумент20 страницFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoОценок пока нет

- Interest Rate Risk: by Erni EkawatiДокумент22 страницыInterest Rate Risk: by Erni EkawatiRidho AnjikoОценок пока нет

- Notes For The Review of The Capital Asset Pricing ModelДокумент8 страницNotes For The Review of The Capital Asset Pricing ModelJeremiah KhongОценок пока нет

- Capital Market LineДокумент8 страницCapital Market Linecjpadin09Оценок пока нет

- Formal CAPM derivation based on assets' market risk and return contributionsДокумент5 страницFormal CAPM derivation based on assets' market risk and return contributionsJohnОценок пока нет

- 6 Asset Pricing ModelsДокумент18 страниц6 Asset Pricing ModelsUtkarsh BhalodeОценок пока нет

- SAPMДокумент83 страницыSAPMSuchismitaghoseОценок пока нет

- Exercises in WACC and Capital StructureДокумент13 страницExercises in WACC and Capital StructureDhanz Onda de LunaОценок пока нет

- How to Value Stocks Using Capital Asset Pricing Theory and the CAPM ModelДокумент41 страницаHow to Value Stocks Using Capital Asset Pricing Theory and the CAPM ModelAdam KhaleelОценок пока нет

- Capm & Apt-1Документ7 страницCapm & Apt-1Trevor MwangiОценок пока нет

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsДокумент36 страницRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuОценок пока нет

- Wacc FormulasДокумент3 страницыWacc FormulasvrrsvОценок пока нет

- ValuationДокумент3 страницыValuationRendry Da Silva SantosОценок пока нет

- Risk and Return AnalysisДокумент28 страницRisk and Return AnalysisNivaashene SaravananОценок пока нет

- Valuation of Firms in Mergers and Acquisitions: Okan BayrakДокумент27 страницValuation of Firms in Mergers and Acquisitions: Okan Bayrakneha1001Оценок пока нет

- Capital Asset Pricing Mode1Документ9 страницCapital Asset Pricing Mode1Shaloo SidhuОценок пока нет

- Summary Chap 12, MKL, Findi Kumala DewiДокумент5 страницSummary Chap 12, MKL, Findi Kumala Dewiresty auliaОценок пока нет

- APTДокумент7 страницAPTStefanОценок пока нет

- BFC5935 - Tutorial 3 Solutions PDFДокумент6 страницBFC5935 - Tutorial 3 Solutions PDFXue XuОценок пока нет

- CAPMДокумент6 страницCAPMAhsaan KhanОценок пока нет

- Module 2 CAPMДокумент11 страницModule 2 CAPMTanvi DevadigaОценок пока нет

- Calculating MNC Cost of Capital for Foreign ProjectsДокумент13 страницCalculating MNC Cost of Capital for Foreign ProjectsAbdul RehmanОценок пока нет

- Portfolio Management: Statical Analysis For Single SecurityДокумент5 страницPortfolio Management: Statical Analysis For Single SecurityJenneey D RajaniОценок пока нет

- Risk and COCДокумент28 страницRisk and COCaneeshaОценок пока нет

- The Cost of CapitalДокумент4 страницыThe Cost of CapitalCharice CortesОценок пока нет

- Financial Management - Topic 6 - CAPMДокумент24 страницыFinancial Management - Topic 6 - CAPMMichael RobertОценок пока нет

- How Do Investment Banks Value Initial Public Offerings (Ipos) ?Документ32 страницыHow Do Investment Banks Value Initial Public Offerings (Ipos) ?mumssrОценок пока нет

- Implementing Basel II - Impact On Emerging EconomiesДокумент17 страницImplementing Basel II - Impact On Emerging EconomiesRevanth NvОценок пока нет

- The - Matrix 1999 DVDRip - XvidДокумент24 страницыThe - Matrix 1999 DVDRip - XvidmumssrОценок пока нет

- AGBR BroucherДокумент1 страницаAGBR BrouchermumssrОценок пока нет

- B G ShirkeДокумент15 страницB G ShirkeAbu AbuОценок пока нет

- Multi-Act MSSP PMSДокумент39 страницMulti-Act MSSP PMSAnkurОценок пока нет

- Tutor 2 (Cost, Volume, Profit Analysis)Документ2 страницыTutor 2 (Cost, Volume, Profit Analysis)aulia100% (1)

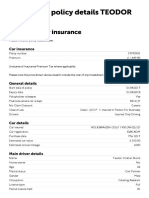

- Policy Details PageДокумент2 страницыPolicy Details PageLuci PoroОценок пока нет

- 06 Growth Rate of Potential GDPДокумент1 страница06 Growth Rate of Potential GDPmiketolОценок пока нет

- Final Project of Working CapitalДокумент118 страницFinal Project of Working CapitalVishal Keshri0% (1)

- Tata Corus AquisitionДокумент30 страницTata Corus Aquisitionshreyas1111Оценок пока нет

- Phiếu Giao Bài Tập Số 3Документ3 страницыPhiếu Giao Bài Tập Số 3Phạm Thị Thúy HằngОценок пока нет

- 2 Conceptual Framework For Financial ReportingДокумент16 страниц2 Conceptual Framework For Financial ReportingIman HaidarОценок пока нет

- Costing 8Документ12 страницCosting 8Ajay SahooОценок пока нет

- Hero Hond: Marketing and Human Resource ManagementДокумент70 страницHero Hond: Marketing and Human Resource Managementdhiraj022Оценок пока нет

- Practice Bonds and Stocks ProblemsДокумент6 страницPractice Bonds and Stocks ProblemsKevin DayanОценок пока нет

- Worksheet 2-Point - Elasticity-of-DemandДокумент4 страницыWorksheet 2-Point - Elasticity-of-DemandFran YОценок пока нет

- Study of Gender PricingДокумент76 страницStudy of Gender PricingKHOUОценок пока нет

- Tugas Pertemuan 2 - Alya Sufi Ikrima - 041911333248Документ3 страницыTugas Pertemuan 2 - Alya Sufi Ikrima - 041911333248Alya Sufi IkrimaОценок пока нет

- Situation Analysis and Marketing PlanДокумент46 страницSituation Analysis and Marketing PlanCharlie KienbaumОценок пока нет

- Cuadernillo IV Parcial Quinto Grado 2022Документ1 страницаCuadernillo IV Parcial Quinto Grado 2022tumbalacasamami5365Оценок пока нет

- Dealers Draft LetterДокумент3 страницыDealers Draft LetterAnil BatraОценок пока нет

- Process CostingДокумент76 страницProcess CostingAnonymous Lz2qH7Оценок пока нет

- A Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Документ25 страницA Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Cato InstituteОценок пока нет

- Ias 18 Revenue Recognition FinalsДокумент8 страницIas 18 Revenue Recognition FinalssadikiОценок пока нет

- CH 1 Cost Volume Profit Analysis Absorption CostingДокумент21 страницаCH 1 Cost Volume Profit Analysis Absorption CostingNigussie BerhanuОценок пока нет

- Quiz 10Документ6 страницQuiz 10Kath RiveraОценок пока нет

- Transaction keys guideДокумент8 страницTransaction keys guideKamleshSarojОценок пока нет

- Causes and Measures of Disequilibrium in Balance of PaymentsДокумент6 страницCauses and Measures of Disequilibrium in Balance of PaymentsMonika PathakОценок пока нет

- IndiGo Q2 FY22 Earnings CallДокумент16 страницIndiGo Q2 FY22 Earnings CallBhav Bhagwan HaiОценок пока нет

- Accounting 1 Review QuizДокумент6 страницAccounting 1 Review QuizAikalyn MangubatОценок пока нет