Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- MGEA02 DoccsДокумент39 страницMGEA02 DoccsShivam Kapila100% (1)

- Log in Sign Up Browse: Answers To The Questions in Question Paper From MBA in TQMДокумент6 страницLog in Sign Up Browse: Answers To The Questions in Question Paper From MBA in TQMthakur_neha20_903303Оценок пока нет

- Assignment On: Banking Companies Act, 1991Документ11 страницAssignment On: Banking Companies Act, 1991Mehedi Hasan100% (4)

- Ficci FinalДокумент22 страницыFicci Finalthakur_neha20_903303100% (1)

- Introduction To Osha: Directorate of Training and Education OSHA Training InstituteДокумент36 страницIntroduction To Osha: Directorate of Training and Education OSHA Training Institutethakur_neha20_903303Оценок пока нет

- Background To Industrial RelationsДокумент38 страницBackground To Industrial RelationsBrand GireeОценок пока нет

- Ficci FinalДокумент22 страницыFicci Finalthakur_neha20_903303100% (1)

- A Presentation On Organizational Change ModelДокумент15 страницA Presentation On Organizational Change Modelthakur_neha20_903303Оценок пока нет

- 1-Importance of A ShmsДокумент43 страницы1-Importance of A ShmsadnanОценок пока нет

- Candlepresentation3 110220224233 Phpapp02Документ39 страницCandlepresentation3 110220224233 Phpapp02thakur_neha20_903303Оценок пока нет

- Breach of Contract & RemediesДокумент44 страницыBreach of Contract & Remediesthakur_neha20_903303100% (1)

- Exec CompДокумент30 страницExec Compthakur_neha20_903303Оценок пока нет

- Gateways To CommunicationДокумент32 страницыGateways To Communicationthakur_neha20_903303100% (1)

- SpeechDCBI 2013 07 05Документ3 страницыSpeechDCBI 2013 07 05Girish AggarwalОценок пока нет

- Managing Diverse Work ForceДокумент6 страницManaging Diverse Work Forcethakur_neha20_903303Оценок пока нет

- Nature and Functions of HRMДокумент16 страницNature and Functions of HRMthakur_neha20_903303100% (1)

- Anchoring ScriptДокумент2 страницыAnchoring Scriptthakur_neha20_903303Оценок пока нет

- Fringebenefits PPT For StudentsДокумент40 страницFringebenefits PPT For Studentsthakur_neha20_903303Оценок пока нет

- Retailing in IndiaДокумент25 страницRetailing in Indiathakur_neha20_903303Оценок пока нет

- Quality ManagementДокумент56 страницQuality Managementthakur_neha20_903303Оценок пока нет

- of Incentives PlansДокумент20 страницof Incentives Plansbaby0310Оценок пока нет

- Class 14 Slides Spring 2005Документ34 страницыClass 14 Slides Spring 2005thakur_neha20_903303Оценок пока нет

- ExecutivecompensationДокумент16 страницExecutivecompensationSana XanaОценок пока нет

- HRD Functions and Roles of HRD ProfessionalsДокумент18 страницHRD Functions and Roles of HRD Professionalsshanmugamhr57% (7)

- HRD Manager: Roles and CompetenciesДокумент19 страницHRD Manager: Roles and Competenciesthakur_neha20_903303Оценок пока нет

- LeadershipДокумент15 страницLeadershipthakur_neha20_903303Оценок пока нет

- QMPДокумент12 страницQMPkbl27Оценок пока нет

- Human Resource Development PPT For StudentsДокумент71 страницаHuman Resource Development PPT For Studentsthakur_neha20_903303Оценок пока нет

- Retailing in IndiaДокумент25 страницRetailing in Indiathakur_neha20_903303Оценок пока нет

- Tools of Financial Analysis & PlanningДокумент68 страницTools of Financial Analysis & Planninganon_672065362100% (1)

- Multiple ChoiceДокумент18 страницMultiple ChoiceJonnel Samaniego100% (1)

- Comparative Statement of Profit and LossДокумент6 страницComparative Statement of Profit and LossHimanshi ChopraОценок пока нет

- Venture Capital in India 2017 ProjectДокумент80 страницVenture Capital in India 2017 Projectakki_655150% (2)

- Economics of Indian Premier League FinalДокумент19 страницEconomics of Indian Premier League Finalshona1412100% (1)

- FIORI Apps in Simple FinanceДокумент13 страницFIORI Apps in Simple FinancesaavbОценок пока нет

- Agreement To SellДокумент6 страницAgreement To Sellsmrithi s. UnnithanОценок пока нет

- C4 PDFДокумент373 страницыC4 PDFIssa Adiema100% (4)

- Abra Valley College Vs AquinoДокумент1 страницаAbra Valley College Vs AquinoJoshua Cu SoonОценок пока нет

- BP040 Current Process ModelДокумент1 страницаBP040 Current Process Modelsastrylanka1980Оценок пока нет

- IndramaniДокумент1 страницаIndramaniBalraj BawaОценок пока нет

- Sample Profit and LossДокумент3 страницыSample Profit and Losssharoneyezs6791100% (1)

- PDFДокумент189 страницPDFPrakashОценок пока нет

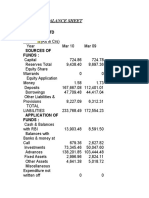

- Balance Sheet: JK Cement LTDДокумент3 страницыBalance Sheet: JK Cement LTDHimanshu SharmaОценок пока нет

- DemeДокумент12 страницDemeKevin ParkerОценок пока нет

- ANZN Annual Results 291009Документ2 страницыANZN Annual Results 291009bernardchickeyОценок пока нет

- Social Investment Manual PDFДокумент56 страницSocial Investment Manual PDFCrăciunОценок пока нет

- (COSBUS2) (BUS-CA2) Cost and Management Accounting 2 (Nov2013) v5Документ8 страниц(COSBUS2) (BUS-CA2) Cost and Management Accounting 2 (Nov2013) v5FarrukhsgОценок пока нет

- Rule: Multi Year Increase in Fees and Charges For Egg, Poultry, and Rabbit Grading and Audit ServicesДокумент3 страницыRule: Multi Year Increase in Fees and Charges For Egg, Poultry, and Rabbit Grading and Audit ServicesJustia.comОценок пока нет

- Dew Right CompanyДокумент11 страницDew Right CompanyGaurav KumarОценок пока нет

- Paper 4 Taxation Nov 14 PDFДокумент16 страницPaper 4 Taxation Nov 14 PDFghsjgjОценок пока нет

- Pre-Feasibility Study: Tea CompanyДокумент20 страницPre-Feasibility Study: Tea CompanyIPro PkОценок пока нет

- Interloop LimitedДокумент4 страницыInterloop LimitedEmadОценок пока нет

- RJR Case StudyДокумент5 страницRJR Case StudyFelipe Kasai MarcosОценок пока нет

- Mjunction Services Limited: Final Settlement PayslipДокумент1 страницаMjunction Services Limited: Final Settlement PayslipNur IslamОценок пока нет

- CIR V COFA - VAT ExemptionДокумент2 страницыCIR V COFA - VAT ExemptionJose MasarateОценок пока нет

- Renewable Energy Act of 2008 SummaryДокумент8 страницRenewable Energy Act of 2008 SummaryArcie SercadoОценок пока нет

- HW - AFM - E7-25, E7-28, P7-42 - Kelompok 8Документ7 страницHW - AFM - E7-25, E7-28, P7-42 - Kelompok 8swear to the skyОценок пока нет