Вам также может понравиться

- ACCA BT-FBT-AB-F1 Business and Technology NotesДокумент65 страницACCA BT-FBT-AB-F1 Business and Technology NotesAlex Zhang100% (1)

- NSS Econ 5 CH 5 Change in AD and As Consolidation WorksheetsДокумент25 страницNSS Econ 5 CH 5 Change in AD and As Consolidation WorksheetskamanОценок пока нет

- Inflation-Conscious Investments: Avoid the most common investment pitfallsОт EverandInflation-Conscious Investments: Avoid the most common investment pitfallsОценок пока нет

- Great Dep - Keynes and MonetarismДокумент10 страницGreat Dep - Keynes and MonetarismAdan MirzaОценок пока нет

- Cost Push InflationДокумент3 страницыCost Push InflationObaidullah Al Mahmud RefatОценок пока нет

- Topic F STD VerДокумент38 страницTopic F STD Verwgg5774Оценок пока нет

- Keynesian vs. Classical Income ModelДокумент70 страницKeynesian vs. Classical Income ModelNitish KhatanaОценок пока нет

- Fourth Edition CH 33 Agregate Demand and SupplyДокумент62 страницыFourth Edition CH 33 Agregate Demand and SupplyLukas PrawiraОценок пока нет

- Chapter 1Документ23 страницыChapter 1Dania QistinaОценок пока нет

- Aggregate Demand and Aggregate Supply (AD and AS)Документ46 страницAggregate Demand and Aggregate Supply (AD and AS)Abdullah ShahОценок пока нет

- Great Depression and KeynesДокумент7 страницGreat Depression and KeynesOwaish AhamedОценок пока нет

- BBF1201 - Chapter 2Документ14 страницBBF1201 - Chapter 2Keeme NaoОценок пока нет

- Lecture10-1.AS-AD Model-1..2023Документ53 страницыLecture10-1.AS-AD Model-1..2023Melike ÇetinkayaОценок пока нет

- Economics Today The Macro 17th Edition Roger LeRoy Miller Solutions Manual DownloadДокумент9 страницEconomics Today The Macro 17th Edition Roger LeRoy Miller Solutions Manual DownloadJeremy Jackson100% (21)

- Classical and Keynesian Macro AnalysisДокумент29 страницClassical and Keynesian Macro Analysispriyasunil2008Оценок пока нет

- Macro Economics: Assignment 04Документ11 страницMacro Economics: Assignment 04Areesha NafeesОценок пока нет

- Principles of Economics Chapter 22Документ30 страницPrinciples of Economics Chapter 22Lu CheОценок пока нет

- Economic Assignment 2Документ7 страницEconomic Assignment 2Prateek_Ghai_303Оценок пока нет

- Aggregate Demand.: Lecture 4 Macroeconomic EquilibriumДокумент18 страницAggregate Demand.: Lecture 4 Macroeconomic EquilibriumLisa RżeczyckayaОценок пока нет

- S3M. Keynesian TheoryДокумент51 страницаS3M. Keynesian TheorysdОценок пока нет

- Macro Chapter 3Документ25 страницMacro Chapter 3Ramadan DestaОценок пока нет

- Economics Today 17th Edition Roger Leroy Miller Solutions ManualДокумент9 страницEconomics Today 17th Edition Roger Leroy Miller Solutions ManualKimCoffeyjndf100% (45)

- Aggregate Demand and Aggregate SupplyДокумент51 страницаAggregate Demand and Aggregate SupplyNhược NhượcОценок пока нет

- S6 Product Market EqulibriumДокумент49 страницS6 Product Market EqulibriumthreexlmusketeersОценок пока нет

- Short-Run Economic Fluctuations: Economic Activity Fluctuates From Year To YearДокумент49 страницShort-Run Economic Fluctuations: Economic Activity Fluctuates From Year To YearDinda Cici AuliaОценок пока нет

- In This Chapter, There Are Four Objectives We Want To LearnДокумент11 страницIn This Chapter, There Are Four Objectives We Want To LearnelvienОценок пока нет

- Money Growth and Inflation: David Chow Mar 2020Документ23 страницыMoney Growth and Inflation: David Chow Mar 2020Johnny SinsОценок пока нет

- 6 - Aggregate Demand and SupplyДокумент62 страницы6 - Aggregate Demand and SupplyMạnh Nguyễn VănОценок пока нет

- Low .BДокумент13 страницLow .Bsteven msusaОценок пока нет

- S6 Product Market EqulibriumДокумент40 страницS6 Product Market EqulibriumShrija Majumder BJ22152Оценок пока нет

- 33 Princ-ch33-Tổng Cung Và Tổng CầuДокумент81 страница33 Princ-ch33-Tổng Cung Và Tổng CầuThành Đạt Lại (Steve)Оценок пока нет

- 3 Aggregate Demand and SupplyДокумент34 страницы3 Aggregate Demand and SupplySaiPraneethОценок пока нет

- Ad-AsДокумент52 страницыAd-AsNavneet ChauhanОценок пока нет

- Session 5 - Goods Market Equilibrium (AS & AD Model)Документ9 страницSession 5 - Goods Market Equilibrium (AS & AD Model)Nikhil kumarОценок пока нет

- MACRO - as-AD Keynsian-Classic ModelДокумент30 страницMACRO - as-AD Keynsian-Classic ModelUrBaN-xGaMeRx TriicKShOtZОценок пока нет

- Chapter - 33 ECO121Документ55 страницChapter - 33 ECO121Le Pham Khanh Ha (K17 HCM)Оценок пока нет

- Macro Chpter 1Документ15 страницMacro Chpter 1Taha SabirОценок пока нет

- Ensuring Price StabilityДокумент36 страницEnsuring Price StabilityAdeel SabirОценок пока нет

- The Consumptionist/keynesian Side of The Unemployment Controversy Will Be Dealt With in Depth in Week 12. Those Interested in An Immediate Account Can Consult Capitalism, Chapter 18Документ6 страницThe Consumptionist/keynesian Side of The Unemployment Controversy Will Be Dealt With in Depth in Week 12. Those Interested in An Immediate Account Can Consult Capitalism, Chapter 18Breno ArrudaОценок пока нет

- Introduction To Economic Fluctuations:: "Macroeconomics by Mankiw"Документ23 страницыIntroduction To Economic Fluctuations:: "Macroeconomics by Mankiw"rabia liaqatОценок пока нет

- Aggregate Demand and Aggregate SupplyДокумент52 страницыAggregate Demand and Aggregate SupplyTonny NguyenОценок пока нет

- MacroEconomics - ASSIGNMENT 1Документ11 страницMacroEconomics - ASSIGNMENT 1Amrinder SinghОценок пока нет

- Introduction To Economic Fluctuations: Instructor: Dmytro HryshkoДокумент32 страницыIntroduction To Economic Fluctuations: Instructor: Dmytro HryshkoNandini KashyapОценок пока нет

- Micro Vs Macro Economics Circular Flow of Income DepressionДокумент15 страницMicro Vs Macro Economics Circular Flow of Income DepressionSai harshaОценок пока нет

- Second MacroДокумент13 страницSecond Macrosteven msusaОценок пока нет

- Theme 2.4 NotesДокумент5 страницTheme 2.4 NoteslucОценок пока нет

- Aggregate Supply: Aggregate Supply Is The Aggregate of All TheДокумент3 страницыAggregate Supply: Aggregate Supply Is The Aggregate of All TheAnonymous AKdppszR5MОценок пока нет

- Macroeconomics A Contemporary Approach 10Th Edition Mceachern Solutions Manual Full Chapter PDFДокумент31 страницаMacroeconomics A Contemporary Approach 10Th Edition Mceachern Solutions Manual Full Chapter PDFjane.hardage449100% (12)

- Macroeconomics A Contemporary Approach 10th Edition McEachern Solutions Manual 1Документ36 страницMacroeconomics A Contemporary Approach 10th Edition McEachern Solutions Manual 1tinacunninghamadtcegyrxz100% (28)

- Macroeconomics A Contemporary Approach 10th Edition McEachern Solutions Manual 1Документ8 страницMacroeconomics A Contemporary Approach 10th Edition McEachern Solutions Manual 1paula100% (51)

- Economics McqsДокумент56 страницEconomics McqsAtif KhanОценок пока нет

- Asistensi 2 After UTS: Chapter 33 & 34 By: Khaira Abdillah Source: Cengage LearningДокумент111 страницAsistensi 2 After UTS: Chapter 33 & 34 By: Khaira Abdillah Source: Cengage LearningReza FahleviОценок пока нет

- Topic 6: Aggregate Demand & Aggregate Supply (PART 1) : Case & Fair (Ch. 26)Документ48 страницTopic 6: Aggregate Demand & Aggregate Supply (PART 1) : Case & Fair (Ch. 26)chan xianОценок пока нет

- 3iec Eco Revisionbook - 2.1Документ19 страниц3iec Eco Revisionbook - 2.1Nico KarpinskaОценок пока нет

- Aggregate Demand and SupplyДокумент63 страницыAggregate Demand and SupplyRashmeet AroraОценок пока нет

- Economic DebatesДокумент7 страницEconomic DebatesMphatso ManyambaОценок пока нет

- Week 6 Chapter 9 Slides AS AD - 08032021 092327am 1 01112021 081322am 05112023 111727am 26022024 023324pm 24032024 094701pmДокумент33 страницыWeek 6 Chapter 9 Slides AS AD - 08032021 092327am 1 01112021 081322am 05112023 111727am 26022024 023324pm 24032024 094701pmMosavi RecordsОценок пока нет

- Chapter 15: Aggregate Demand and Supply ReviewerДокумент5 страницChapter 15: Aggregate Demand and Supply Revieweradam_barrettoОценок пока нет

- Chapter 14 (Principle of Economic)Документ42 страницыChapter 14 (Principle of Economic)izatul akmal maisarahОценок пока нет

- Chapter 3Документ5 страницChapter 3ru40342Оценок пока нет

- TWO STAGFLATIONS - YOM-KIPPUR WAR, COVID19, UKRAINE WAR: Economic and Geopolitical EffectsОт EverandTWO STAGFLATIONS - YOM-KIPPUR WAR, COVID19, UKRAINE WAR: Economic and Geopolitical EffectsОценок пока нет

- Salida Salt Company State Rock Salt Contract Analysis Input Variables Basic Value DistributionДокумент2 страницыSalida Salt Company State Rock Salt Contract Analysis Input Variables Basic Value DistributionAkriti ShahОценок пока нет

- Contact Cost Response Cost Acquisition CostДокумент43 страницыContact Cost Response Cost Acquisition CostAkriti ShahОценок пока нет

- Macro Eco Session 8Документ42 страницыMacro Eco Session 8Akriti ShahОценок пока нет

- AkritiShah 46 BATAДокумент19 страницAkritiShah 46 BATAAkriti ShahОценок пока нет

- FindingsДокумент18 страницFindingsAkriti ShahОценок пока нет

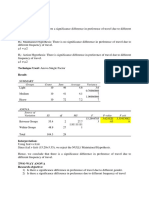

- One Way Anova Research Objective: Is There A Significance Difference in Preference of Travel Due To DifferentДокумент7 страницOne Way Anova Research Objective: Is There A Significance Difference in Preference of Travel Due To DifferentAkriti ShahОценок пока нет

- Q1 Short Note On Information System: RelevanceДокумент13 страницQ1 Short Note On Information System: RelevanceAkriti ShahОценок пока нет

- 19 Ratio Analysis TheoryДокумент22 страницы19 Ratio Analysis TheoryAkriti ShahОценок пока нет

- Find A Logo and Add Here I Am Getting All Ones With White Apply Good Theme and Font and Format Also. If Anything Is Missing Let Me KnowДокумент32 страницыFind A Logo and Add Here I Am Getting All Ones With White Apply Good Theme and Font and Format Also. If Anything Is Missing Let Me KnowAkriti ShahОценок пока нет

- AP Macroeconomics 2010 Free-Response Questions: The College BoardДокумент8 страницAP Macroeconomics 2010 Free-Response Questions: The College BoardNarsing MadhurОценок пока нет

- 250 MCQ For Ugc-Net Commerce and Economics Download PDF For FreeДокумент56 страниц250 MCQ For Ugc-Net Commerce and Economics Download PDF For FreeDiwakar Entertainment Dose67% (3)

- Multiple Choiice 2nd SemДокумент119 страницMultiple Choiice 2nd SemMudit RokzzОценок пока нет

- Simple Keynesian Model of Income DeterminationДокумент22 страницыSimple Keynesian Model of Income DeterminationBhagyashree Chauhan100% (1)

- Assignment On Intermediate Macro Economic (ECN 303) - USEDДокумент6 страницAssignment On Intermediate Macro Economic (ECN 303) - USEDBernardokpeОценок пока нет

- Structural StagnationДокумент27 страницStructural StagnationRandall Curtis100% (1)

- Home Economics Mcqs PaperДокумент27 страницHome Economics Mcqs Paperlog manОценок пока нет

- Case Study The Great Depression and The Global Financial CrisisДокумент9 страницCase Study The Great Depression and The Global Financial CrisisBurak NaldökenОценок пока нет

- Aggregate Demand Aggregate Supply 2.2 2.3 Mark SchemeДокумент53 страницыAggregate Demand Aggregate Supply 2.2 2.3 Mark Schemeayra kamalОценок пока нет

- Central Superior Services (CSS) Examination, Pakistan - Causes of InflationДокумент5 страницCentral Superior Services (CSS) Examination, Pakistan - Causes of InflationAmeer KhanОценок пока нет

- 2.1 Monetary PolicyДокумент48 страниц2.1 Monetary PolicyAnu AndrewsОценок пока нет

- BUSINESS CYCLE MaCROECONOMICSДокумент20 страницBUSINESS CYCLE MaCROECONOMICSJesierine GarciaОценок пока нет

- Original PDF Economics Today 19th by Roger Leroy Miller PDFДокумент41 страницаOriginal PDF Economics Today 19th by Roger Leroy Miller PDFwendy.ramos733100% (38)

- AQA MCQ Macroeconomics Book 3 PDFДокумент22 страницыAQA MCQ Macroeconomics Book 3 PDFkumarraghav581Оценок пока нет

- The Shortrun Tradeoff Between Inflation and UnemploymentДокумент42 страницыThe Shortrun Tradeoff Between Inflation and UnemploymentJeremy SilaenОценок пока нет

- Keynes Theory of EmploymentДокумент5 страницKeynes Theory of EmploymentShalini Singh IPSAОценок пока нет

- Chapter 21 The Monetary Policy and Aggregate Demand CurvesДокумент7 страницChapter 21 The Monetary Policy and Aggregate Demand CurvesserbannerОценок пока нет

- Aggregate Demand and SupplyДокумент41 страницаAggregate Demand and SupplySonali JainОценок пока нет

- Ringkasan Materi Bahasa Inggris NiagaДокумент31 страницаRingkasan Materi Bahasa Inggris NiagaNira IndrianiОценок пока нет

- Components of Ad Dp2Документ7 страницComponents of Ad Dp2sunshineОценок пока нет

- The Simple Algebra of The IS-LM Model and The Aggregate Demand CurveДокумент5 страницThe Simple Algebra of The IS-LM Model and The Aggregate Demand CurvechalachewkОценок пока нет

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaДокумент32 страницыDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaKaushik NanduriОценок пока нет

- A Linear Model of Cyclical GrowthДокумент14 страницA Linear Model of Cyclical GrowthErick ManchaОценок пока нет

- The Effect of Unemployment On Economic Development in NigeriaДокумент56 страницThe Effect of Unemployment On Economic Development in Nigeriajamessabraham2Оценок пока нет

- CHP 10 Income and SpendingДокумент13 страницCHP 10 Income and SpendingTeesha AggrawalОценок пока нет

- Aggregate - DemandДокумент111 страницAggregate - DemandLaiba IshaqОценок пока нет

- Debate of Deindustrialisation 1860-1880Документ8 страницDebate of Deindustrialisation 1860-1880Ankit100% (1)

- Macro Bcom New FinalДокумент37 страницMacro Bcom New FinalUsman GhaniОценок пока нет