Вам также может понравиться

- Cash and Bank AccountsДокумент15 страницCash and Bank AccountsFalola Feyisola Richard100% (1)

- Moonshots 10X Is Easier Than 10 PercentДокумент4 страницыMoonshots 10X Is Easier Than 10 PercentOmer Siddiqui100% (1)

- ACCCOB1 Module 3Документ19 страницACCCOB1 Module 3Ayanna CameroОценок пока нет

- Bank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoДокумент3 страницыBank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoKyle PanlaquiОценок пока нет

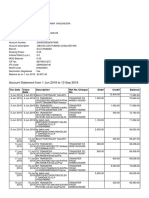

- NBS Bank Statement Dec 2022Документ2 страницыNBS Bank Statement Dec 2022Eric CartmanОценок пока нет

- s5 PDFДокумент5 страницs5 PDFKeshav KumarОценок пока нет

- Investment BankingДокумент85 страницInvestment BankingJoshuva DanielОценок пока нет

- Diploma in Accountancy June 2021 QaДокумент236 страницDiploma in Accountancy June 2021 QaMusonda Mwape100% (1)

- Main Project of Investment BankingДокумент44 страницыMain Project of Investment Bankingsupriyashewale87% (45)

- Investment BankingДокумент56 страницInvestment BankingKomal MansukhaniОценок пока нет

- A Study On Credit AppraisalДокумент83 страницыA Study On Credit AppraisalMallik ArjunОценок пока нет

- Design Thinking WorkshopДокумент14 страницDesign Thinking WorkshopOmer SiddiquiОценок пока нет

- Cost Accounting and Control OutputДокумент21 страницаCost Accounting and Control OutputApril Joy Obedoza100% (5)

- Quezon City University: Bachelor of Science in AccountancyДокумент13 страницQuezon City University: Bachelor of Science in AccountancyRiza Mae Alce50% (2)

- Financial Institutions (Coleen) : Term Funds For The Economy. These Institutions Provide A Variety of FinancialДокумент4 страницыFinancial Institutions (Coleen) : Term Funds For The Economy. These Institutions Provide A Variety of Financialsheinamae quelnatОценок пока нет

- TWO FACES: DEMYSTIFYING THE MORTGAGE ELECTRONIC REGISTRATION SYSTEM'S LAND TITLE THEORY (MERS) SSRN-id1684729Документ39 страницTWO FACES: DEMYSTIFYING THE MORTGAGE ELECTRONIC REGISTRATION SYSTEM'S LAND TITLE THEORY (MERS) SSRN-id1684729CarrieonicОценок пока нет

- Credit Appraisal ReportДокумент125 страницCredit Appraisal ReportSadaf IqbalОценок пока нет

- Management of Financial Institutions - BNK604 Power Point Slides Lecture 02Документ35 страницManagement of Financial Institutions - BNK604 Power Point Slides Lecture 02suma100% (4)

- MBA Project Report On Kotak Life InsuranceДокумент61 страницаMBA Project Report On Kotak Life InsuranceCyberfunОценок пока нет

- FI - Fall 2020 - PPT Slides - IntroductionДокумент27 страницFI - Fall 2020 - PPT Slides - IntroductionBabar MairajОценок пока нет

- Banking and Finance PDFДокумент43 страницыBanking and Finance PDFInFiNiTy100% (1)

- FMI Class - Chap 2Документ29 страницFMI Class - Chap 2ruman mahmoodОценок пока нет

- New Microsoft PowerPoint PresentationДокумент32 страницыNew Microsoft PowerPoint PresentationSaad MajeedОценок пока нет

- Financial and Regulatory Institutions: Assignment No. 2Документ12 страницFinancial and Regulatory Institutions: Assignment No. 2Saad MajeedОценок пока нет

- Presentation 1Документ13 страницPresentation 1ashwin6950Оценок пока нет

- NBFI'sДокумент31 страницаNBFI'sMuhammad Shabahat AhmadОценок пока нет

- Bank Meaning and FunctionsДокумент8 страницBank Meaning and FunctionsNeeta SharmaОценок пока нет

- Management of Financial Institutions - BNK604 Power Point Slides Lecture 02Документ31 страницаManagement of Financial Institutions - BNK604 Power Point Slides Lecture 02aimanbatool24Оценок пока нет

- Banking: Praveen Asokan 13382053 Mba-IbДокумент33 страницыBanking: Praveen Asokan 13382053 Mba-IbAnubhav JhaОценок пока нет

- CHAPTER Two Money and BankingДокумент8 страницCHAPTER Two Money and Bankingananya tesfayeОценок пока нет

- Structure of Indian Financial SystemДокумент24 страницыStructure of Indian Financial SystemRaj SodhaОценок пока нет

- Financial InsitutionsДокумент14 страницFinancial Insitutionscatprep2023Оценок пока нет

- FMI - Chap 2Документ35 страницFMI - Chap 2alioОценок пока нет

- Investment BankingДокумент12 страницInvestment BankingrocksonОценок пока нет

- Investment Banking: Group No:-4Документ26 страницInvestment Banking: Group No:-4_DJ_rocksОценок пока нет

- Financial Services ProjectДокумент32 страницыFinancial Services Projecthimita desaiОценок пока нет

- Banking MicroeconДокумент18 страницBanking Microeconnabil saifОценок пока нет

- Chapter One Meaning and Definition of Banking Meaning of BankingДокумент6 страницChapter One Meaning and Definition of Banking Meaning of BankingMk FisihaОценок пока нет

- Executive SummaryДокумент42 страницыExecutive SummarybhaveshjadavОценок пока нет

- Meaning of Finance: Information Has Been Collected From The WebsiteДокумент93 страницыMeaning of Finance: Information Has Been Collected From The WebsiteShobhit GoswamiОценок пока нет

- BankingДокумент100 страницBankingJayakiran RaiОценок пока нет

- Commercial Banks, FI and NBIFДокумент17 страницCommercial Banks, FI and NBIFVikash kumarОценок пока нет

- Content (Kiran)Документ67 страницContent (Kiran)Omkar ChavanОценок пока нет

- Iqra AssignmentДокумент5 страницIqra AssignmentAymen ImtiazОценок пока нет

- Banking and Its TypeДокумент13 страницBanking and Its TypeJaidev KannanОценок пока нет

- The Project On Pragathi BankДокумент85 страницThe Project On Pragathi BankPrashanth PBОценок пока нет

- Analysis of Investment Banking in Real Estate in IndiaДокумент11 страницAnalysis of Investment Banking in Real Estate in IndiaVinayak PadwalОценок пока нет

- COMMERCIALДокумент15 страницCOMMERCIALBadbitchОценок пока нет

- MFS Module 1Документ89 страницMFS Module 1Navleen KaurОценок пока нет

- What Is A BankДокумент14 страницWhat Is A BankNandini JaganОценок пока нет

- Union Bank of IndiaДокумент58 страницUnion Bank of IndiaRakesh Prabhakar ShrivastavaОценок пока нет

- Group 4 PresentationДокумент6 страницGroup 4 PresentationeranyigiОценок пока нет

- Final Investment BankingДокумент65 страницFinal Investment Bankingasmita2794Оценок пока нет

- Executive SummaryДокумент54 страницыExecutive SummarybhaveshjadavОценок пока нет

- Industry - Fundamental AnalysisДокумент13 страницIndustry - Fundamental AnalysisJerin JoyОценок пока нет

- Investment BankДокумент5 страницInvestment BankPradeep KumarОценок пока нет

- Financial InstitutionsДокумент76 страницFinancial InstitutionsGaurav Rathaur100% (1)

- Meaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofДокумент32 страницыMeaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofPunya KrishnaОценок пока нет

- Unit 1 Introduction To BankingДокумент27 страницUnit 1 Introduction To BankingRandom HeroОценок пока нет

- PFM AnswersДокумент48 страницPFM Answershinowal388Оценок пока нет

- Shivam - Kumar - MFS AssignmentДокумент8 страницShivam - Kumar - MFS AssignmentShivam KumarОценок пока нет

- Financial EnvironmentДокумент7 страницFinancial Environmenthussainmeeran12Оценок пока нет

- Fin 642 Report UpdatedДокумент18 страницFin 642 Report UpdatedMahmudulHasanRakibОценок пока нет

- Financial Services IndustryДокумент18 страницFinancial Services Industryashish sunnyОценок пока нет

- Attachment Indian Financial System IДокумент43 страницыAttachment Indian Financial System IPratheesh BoseОценок пока нет

- Meaning of Banking: 1. Central BanksДокумент6 страницMeaning of Banking: 1. Central BanksMuskanОценок пока нет

- Investment BankingДокумент32 страницыInvestment BankingRavi SharmaОценок пока нет

- Financial Intermediaries and Players Philippines Financial Intermediaries and PlayersДокумент9 страницFinancial Intermediaries and Players Philippines Financial Intermediaries and PlayersLeo-Alyssa Gregorio-CorporalОценок пока нет

- Research Assignment For SuzanaДокумент7 страницResearch Assignment For SuzanaShariful IslamОценок пока нет

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksДокумент5 страницFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikОценок пока нет

- TOI Final Project UpdatedddДокумент9 страницTOI Final Project UpdatedddOmer SiddiquiОценок пока нет

- All PNP ProgramДокумент13 страницAll PNP ProgramOmer SiddiquiОценок пока нет

- Futur - Io - Canvas - Moonshot (Class Exercise)Документ1 страницаFutur - Io - Canvas - Moonshot (Class Exercise)Omer SiddiquiОценок пока нет

- TOI AssignmentДокумент8 страницTOI AssignmentOmer SiddiquiОценок пока нет

- COST BEHAVIOR (Solution)Документ4 страницыCOST BEHAVIOR (Solution)Omer SiddiquiОценок пока нет

- International Finance Chapter 7 Part 1Документ11 страницInternational Finance Chapter 7 Part 1Rohil ChitrakarОценок пока нет

- AS Part 1Документ105 страницAS Part 1hariinshrОценок пока нет

- Chapter 4 Branch AccountingДокумент17 страницChapter 4 Branch Accountingkefyalew TОценок пока нет

- FABM 2 QuizДокумент2 страницыFABM 2 QuizShann 2Оценок пока нет

- Quiz PAS - PAS 19 To 23Документ3 страницыQuiz PAS - PAS 19 To 23Zoey Alvin EstarejaОценок пока нет

- PT - Mbi 2020Документ65 страницPT - Mbi 2020caesar putraОценок пока нет

- Mutual Savings Banks: Are Very Similar To Saving and Loan AssociationsДокумент3 страницыMutual Savings Banks: Are Very Similar To Saving and Loan Associationssamuel debebeОценок пока нет

- Narasimhan Committee Upsc Notes 33Документ2 страницыNarasimhan Committee Upsc Notes 33Gauravpatel CHSОценок пока нет

- Chapter 04 Consolidation ofДокумент64 страницыChapter 04 Consolidation ofBetty Santiago100% (1)

- Simulasi PT Barito Putera Hino 6.4 Ps Dump 11032019Документ1 страницаSimulasi PT Barito Putera Hino 6.4 Ps Dump 11032019bintang_arifОценок пока нет

- Codes Banking MICR Codes RBI 15102010 67440Документ1 455 страницCodes Banking MICR Codes RBI 15102010 67440abhayarchivОценок пока нет

- UNIT 1 Introduction To Treasury ManagementДокумент7 страницUNIT 1 Introduction To Treasury ManagementCarl BautistaОценок пока нет

- Consumer Perception Plastic MoneyДокумент58 страницConsumer Perception Plastic MoneyVasu ThakurОценок пока нет

- AUD02 - 05 Audit of Cash and Cash EquivalentsДокумент3 страницыAUD02 - 05 Audit of Cash and Cash EquivalentsMark BajacanОценок пока нет

- Chapter 13Документ3 страницыChapter 13magnatecyОценок пока нет

- 06 - Governance and Risk Management Wk. 2Документ11 страниц06 - Governance and Risk Management Wk. 2Camilo ToroОценок пока нет

- The Collapse of Lehman Brothers (2008) : A Case StudyДокумент14 страницThe Collapse of Lehman Brothers (2008) : A Case StudyKimberly Joy DimaanoОценок пока нет

- Handouts DiscussionДокумент7 страницHandouts DiscussionAvox EverdeenОценок пока нет

- Tutorial Test 5: 1. Three Types of ActivitiesДокумент4 страницыTutorial Test 5: 1. Three Types of ActivitiesVan Nguyen Thi HoangОценок пока нет

- Popularity of Credit Cards Issued by Different BanksДокумент25 страницPopularity of Credit Cards Issued by Different BanksNaveed Karim Baksh75% (8)