Вам также может понравиться

- Tourism and Climate Change: Evaluating The Extent of Policy IntegrationДокумент23 страницыTourism and Climate Change: Evaluating The Extent of Policy Integrationaparajita promaОценок пока нет

- Tourism and Climate Change: Evaluating The Extent of Policy IntegrationДокумент23 страницыTourism and Climate Change: Evaluating The Extent of Policy Integrationaparajita promaОценок пока нет

- Security Valuation Principles - Ch11Документ68 страницSecurity Valuation Principles - Ch11aparajita promaОценок пока нет

- Expenditures:: Gross Domestic Product Consumption + Investments + Government Spending + (Exports-Imports)Документ14 страницExpenditures:: Gross Domestic Product Consumption + Investments + Government Spending + (Exports-Imports)aparajita promaОценок пока нет

- Full Year: Visitor Arrivals ReportДокумент33 страницыFull Year: Visitor Arrivals Reportaparajita promaОценок пока нет

- Human Resource ManagementДокумент35 страницHuman Resource Managementaparajita promaОценок пока нет

- Commercial Bank Management PDFДокумент42 страницыCommercial Bank Management PDFaparajita promaОценок пока нет

- Methodology On Hotspot Investigation, Information Assortment and Data Handling ConceptsДокумент21 страницаMethodology On Hotspot Investigation, Information Assortment and Data Handling Conceptsaparajita promaОценок пока нет

- Inventory Costing Method of Manufacturing BusinessДокумент29 страницInventory Costing Method of Manufacturing Businessaparajita promaОценок пока нет

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareДокумент41 страницаInvestment Analysis and Portfolio Management: Lecture Presentation Softwareaparajita promaОценок пока нет

- OUR Company: MGT 351 Presentation On Human Resource PlanДокумент16 страницOUR Company: MGT 351 Presentation On Human Resource Planaparajita promaОценок пока нет

- Meaning of Inflation-1Документ7 страницMeaning of Inflation-1aparajita promaОценок пока нет

- Measurement, Reliability, and ValidityДокумент29 страницMeasurement, Reliability, and Validityaparajita promaОценок пока нет

- The Research Process: Coming To TermsДокумент19 страницThe Research Process: Coming To Termsaparajita promaОценок пока нет

- Presentation Final 2 - 2Документ29 страницPresentation Final 2 - 2aparajita promaОценок пока нет

- Questionnaire Vegetable-Vendors 1Документ3 страницыQuestionnaire Vegetable-Vendors 1aparajita promaОценок пока нет

- Deshi Dosh, Swot AnalysisДокумент5 страницDeshi Dosh, Swot Analysisaparajita promaОценок пока нет

- Chapter-10 Return & RiskДокумент19 страницChapter-10 Return & Riskaparajita promaОценок пока нет

- Bankruptcy ActДокумент15 страницBankruptcy Actaparajita promaОценок пока нет

- Law PresentationДокумент8 страницLaw Presentationaparajita promaОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Accounting CoreДокумент10 страницAccounting CoreGioОценок пока нет

- Shareholders VsДокумент2 страницыShareholders VsNidheesh TpОценок пока нет

- Kcse 2010 Business Studies p1Документ5 страницKcse 2010 Business Studies p1Urex ZОценок пока нет

- Chap 013 Financial Accounting (Statement of Cash Flow)Документ39 страницChap 013 Financial Accounting (Statement of Cash Flow)salman saeed100% (2)

- CH Capital Morgan Stanley Rate Sheet - 1.21Документ1 страницаCH Capital Morgan Stanley Rate Sheet - 1.21sokcordell69Оценок пока нет

- Primary Capital Markets: Presented By: Ankit Kumar Farid Farotan Parth Shubham DhimanДокумент53 страницыPrimary Capital Markets: Presented By: Ankit Kumar Farid Farotan Parth Shubham Dhimanankitkmr25Оценок пока нет

- Swet Ganga Hydropower and Construction LTD PDFДокумент58 страницSwet Ganga Hydropower and Construction LTD PDFAnil KhanalОценок пока нет

- Intermediate Microeconomics: Exercises Chapters 9-11Документ32 страницыIntermediate Microeconomics: Exercises Chapters 9-11A01720895 KurodaОценок пока нет

- Course 2 Sample Exam Questions: y Units of BroccoliДокумент47 страницCourse 2 Sample Exam Questions: y Units of BroccoliEden ZapicoОценок пока нет

- 26-06-2020 Financial Management Suggested AnswersДокумент3 страницы26-06-2020 Financial Management Suggested AnswersJEANОценок пока нет

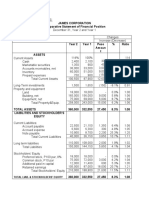

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionДокумент7 страницHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananОценок пока нет

- Corporate Finance (FIN722) Syllabus For Mid Term Exams: Recommended BooksДокумент3 страницыCorporate Finance (FIN722) Syllabus For Mid Term Exams: Recommended BooksShrgeel HussainОценок пока нет

- 3 Departmental AccountsДокумент13 страниц3 Departmental AccountsJayesh VyasОценок пока нет

- Forbes On BuffettДокумент32 страницыForbes On BuffettSharanya Palani100% (2)

- 42 CTP PAAS Result Sheet 2016Документ2 страницы42 CTP PAAS Result Sheet 2016Syed Aziz Hussain0% (1)

- Charlie MungerДокумент43 страницыCharlie Mungerbrijesh007Оценок пока нет

- Combined Valuing Yahoo! in 2013Документ15 страницCombined Valuing Yahoo! in 2013George Ng100% (1)

- Investment AccountДокумент2 страницыInvestment AccountQuestionscastle Friend67% (3)

- Advanced Financial Accounting 11th Edition Christensen Solutions Manual Full Chapter PDFДокумент64 страницыAdvanced Financial Accounting 11th Edition Christensen Solutions Manual Full Chapter PDFSandraMurraykean100% (13)

- Dell Working CapitalДокумент5 страницDell Working CapitalAshna ChowdhryОценок пока нет

- Valuation of Goodwill: (1) Few Years' Purchase of Average Profits Method: Under ThisДокумент5 страницValuation of Goodwill: (1) Few Years' Purchase of Average Profits Method: Under Thisabhi_cool7864757Оценок пока нет

- FM Mbaquiz1Документ4 страницыFM Mbaquiz1Pritee SinghОценок пока нет

- Full Download Book Fundamentals of Corporate Finance 5Th Global Edition PDFДокумент41 страницаFull Download Book Fundamentals of Corporate Finance 5Th Global Edition PDFshirley.sur179100% (23)

- Executive Summary CompleteДокумент4 страницыExecutive Summary CompleteJepkemei MeliОценок пока нет

- Assignment POSTING TO THE LEDGERДокумент7 страницAssignment POSTING TO THE LEDGERJie SapornaОценок пока нет

- Finance ManagementДокумент182 страницыFinance Managementuma3shineОценок пока нет

- GM Foreign Exchange HedgeДокумент4 страницыGM Foreign Exchange HedgeRima Chakravarty Sonde100% (1)

- Law On CorporationsДокумент80 страницLaw On CorporationsSir Jason DulceОценок пока нет

- Relevance and Irrelevance Theories of DividendДокумент4 страницыRelevance and Irrelevance Theories of Dividendptselvakumar0% (1)

- ROD of Keya CosmeticsДокумент71 страницаROD of Keya Cosmeticsrash_sblОценок пока нет