Вам также может понравиться

- Banking India: Accepting Deposits for the Purpose of LendingОт EverandBanking India: Accepting Deposits for the Purpose of LendingОценок пока нет

- A Presentation ON Regional Rural Bank: Hina Khan Mba Iii SemДокумент13 страницA Presentation ON Regional Rural Bank: Hina Khan Mba Iii SemAmitОценок пока нет

- Project Report On Regional Rural Banks (RRBS)Документ14 страницProject Report On Regional Rural Banks (RRBS)Dhairya JainОценок пока нет

- Ppt. Regional Rural BanksДокумент13 страницPpt. Regional Rural BanksRuchi Arora Arora73% (11)

- 12 Chapter 2Документ36 страниц12 Chapter 2Divyanshi JainОценок пока нет

- Regional Rural BanksДокумент18 страницRegional Rural BanksMuzaffar HussainОценок пока нет

- Rural Banking in IndiaДокумент13 страницRural Banking in IndiaStanley JonesОценок пока нет

- Rural BankingДокумент10 страницRural Bankinglaxmi sambre100% (1)

- Regional Rural Banks - Indian Banking LawДокумент28 страницRegional Rural Banks - Indian Banking LawNeed NotknowОценок пока нет

- Rural Banking: Presented By: Hema SinghДокумент34 страницыRural Banking: Presented By: Hema SinghRitika HiiОценок пока нет

- Name - Deepak Bharti CLASS - MBA 4th SEM. ROLL NO. - 57-MBA-07 SESSION - 2007-09Документ8 страницName - Deepak Bharti CLASS - MBA 4th SEM. ROLL NO. - 57-MBA-07 SESSION - 2007-09munish thakur100% (2)

- Regional Rural BanksДокумент2 страницыRegional Rural BanksDev KashyapОценок пока нет

- Regional Rural BanksДокумент6 страницRegional Rural Banksdranita@yahoo.comОценок пока нет

- This Paper Entitled 'RURAL FINANCING' Throws Light On The Following AspectsДокумент6 страницThis Paper Entitled 'RURAL FINANCING' Throws Light On The Following AspectshazursaranОценок пока нет

- Regional Rural BankДокумент4 страницыRegional Rural BankRekha Raghavan NandakumarОценок пока нет

- Rural Banking (Commercial Banking) Prepared by Rajkumar SharmaДокумент12 страницRural Banking (Commercial Banking) Prepared by Rajkumar SharmaSomnath KhandagaleОценок пока нет

- Theory of BankingДокумент48 страницTheory of BankingYashitha CaverammaОценок пока нет

- T 02. Functions of RBI and NABARDДокумент16 страницT 02. Functions of RBI and NABARDDineshОценок пока нет

- National Bank For Agriculture and Rural Development (Nabard)Документ21 страницаNational Bank For Agriculture and Rural Development (Nabard)HASHMI SUTARIYA100% (1)

- " History and Nationalisation of Banks in India ": PresentationДокумент21 страница" History and Nationalisation of Banks in India ": PresentationMayankJainОценок пока нет

- Proect Rural Banking in IndiaДокумент108 страницProect Rural Banking in IndiaRohitRana100% (5)

- Final PPT of Concept of RRBsДокумент27 страницFinal PPT of Concept of RRBsManali ShahОценок пока нет

- Structure of Banking System in IndiaДокумент8 страницStructure of Banking System in IndiaBadal DashОценок пока нет

- Reserve Bank of India (RBI) : Prof. Mishu Tripathi Assistant Professor-FinanceДокумент47 страницReserve Bank of India (RBI) : Prof. Mishu Tripathi Assistant Professor-Financeatanu7590Оценок пока нет

- Rural Banking: (In India)Документ35 страницRural Banking: (In India)nuro smartОценок пока нет

- A Presentation ON Regional Rural Bank: Presented By: Presented ToДокумент20 страницA Presentation ON Regional Rural Bank: Presented By: Presented ToVîçký BårdêОценок пока нет

- Project SynopsisДокумент8 страницProject SynopsisKaushik AdhikariОценок пока нет

- 18.04 - COMMERCIAL BANKS, NBFCS, COOPERATIVE BANKSДокумент12 страниц18.04 - COMMERCIAL BANKS, NBFCS, COOPERATIVE BANKSramixudinОценок пока нет

- Banking in IndiaДокумент13 страницBanking in IndiaMurahari NAОценок пока нет

- Rural BankingДокумент11 страницRural Bankingreach_to_rahulОценок пока нет

- Rural BankingДокумент25 страницRural BankingAamit KumarОценок пока нет

- Banking Sector in IndiaДокумент29 страницBanking Sector in Indiahahire0% (1)

- Capital BudgetingДокумент41 страницаCapital BudgetingLeela KrishnaОценок пока нет

- Objectives of Regional Rural Banks 1Документ8 страницObjectives of Regional Rural Banks 1Sandeep Sandy100% (1)

- Specialized BanksДокумент29 страницSpecialized BankskhusbuОценок пока нет

- Commercial Bank ManagemntДокумент37 страницCommercial Bank ManagemntPriya KalaОценок пока нет

- PRESENTATION in Rural BankingДокумент18 страницPRESENTATION in Rural BankingglorydharmarajОценок пока нет

- Functions of RBIДокумент7 страницFunctions of RBIPriyam PrakashОценок пока нет

- Indian Banking SystemДокумент25 страницIndian Banking SystemTajinder JassalОценок пока нет

- Regional Rural Banks RRBsДокумент11 страницRegional Rural Banks RRBsChintan PandyaОценок пока нет

- Money and Banking System MBAДокумент29 страницMoney and Banking System MBABabasab Patil (Karrisatte)100% (1)

- Commercial Banking in India: Submitted By: Shaikh Azhar S. Roll No.28Документ37 страницCommercial Banking in India: Submitted By: Shaikh Azhar S. Roll No.28Ojas LeoОценок пока нет

- RBI Finance PDF 1 - Regulators and Financial InstitutionsДокумент29 страницRBI Finance PDF 1 - Regulators and Financial InstitutionsbiswashswayambhuОценок пока нет

- NABARDДокумент19 страницNABARDNiravThakkarОценок пока нет

- Regional Rural BankДокумент26 страницRegional Rural BankVijayeta Nerurkar100% (1)

- Development and ApprochДокумент25 страницDevelopment and ApprochVyshnavОценок пока нет

- Miscellaneous Important Points-1Документ21 страницаMiscellaneous Important Points-1bhavishyat kumawatОценок пока нет

- Regional Rural BanksДокумент4 страницыRegional Rural BanksSiddhartha BindalОценок пока нет

- Vsit Rohit ProjectДокумент10 страницVsit Rohit ProjectNaresh KhutikarОценок пока нет

- An Overview of Banking in IndiaДокумент41 страницаAn Overview of Banking in IndiaVinay SudaniОценок пока нет

- NABARDДокумент37 страницNABARDsanjayyadav007100% (1)

- Functions: Commercial BankДокумент12 страницFunctions: Commercial BanksupriyakharadeОценок пока нет

- Regional Rural BankДокумент3 страницыRegional Rural BankSagar A. Barot100% (1)

- Regulators and Financial Institutions PDFДокумент25 страницRegulators and Financial Institutions PDFDexereusОценок пока нет

- Regulators and Financial Institutions PDFДокумент26 страницRegulators and Financial Institutions PDFTarun singhОценок пока нет

- Finance Rbi AffairsmindДокумент326 страницFinance Rbi Affairsmindanshuman kumarОценок пока нет

- Ibs F y B.com (H) Unit 1Документ18 страницIbs F y B.com (H) Unit 1Nikunj PatelОценок пока нет

- Higher Financing InstitutionsДокумент10 страницHigher Financing InstitutionsApeksha GuruwadeyarОценок пока нет

- Chapter 02Документ24 страницыChapter 02JuManHaqZzОценок пока нет

- Banking Law ProjectДокумент2 страницыBanking Law ProjectALKA LAKRAОценок пока нет

- IFSC Code Available in NACH For Banks Live in ACH Credit Ason Mar132015Документ7 883 страницыIFSC Code Available in NACH For Banks Live in ACH Credit Ason Mar132015Samuel GeorgeОценок пока нет

- ClssДокумент10 страницClssRajendra Kumar MeghwalОценок пока нет

- Cooperative Bank Internship ProjectДокумент64 страницыCooperative Bank Internship ProjectPrashanth Gowda82% (57)

- Finance Team 2020-2021Документ465 страницFinance Team 2020-2021DIVYANSHU SHEKHARОценок пока нет

- List of BanksДокумент8 страницList of BanksAditi GuptaОценок пока нет

- Types of BankingДокумент10 страницTypes of BankingJinu SajiОценок пока нет

- Project On Rural Banking in India 15-01-2023Документ74 страницыProject On Rural Banking in India 15-01-2023Praveen ChaudharyОценок пока нет

- Thesis On Regional Rural Banks in IndiaДокумент8 страницThesis On Regional Rural Banks in Indiafj9dbfw4100% (2)

- Rural Banking in IndiaДокумент70 страницRural Banking in IndiaPrashant Shinde67% (3)

- S.N. Bank Name Ifsc MicrДокумент6 страницS.N. Bank Name Ifsc Micrsivakrishna777777Оценок пока нет

- Abhilasha DubeyДокумент8 страницAbhilasha Dubeyanon_292119648Оценок пока нет

- A Study On Rural Banking in India: 1) SummaryДокумент72 страницыA Study On Rural Banking in India: 1) SummarySagar A. BarotОценок пока нет

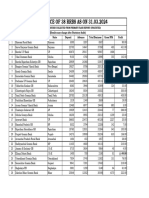

- ATCH To Cir. No. 89 - PERFORMANCE OF 39 RRBS AS ON 31.03.2024Документ2 страницыATCH To Cir. No. 89 - PERFORMANCE OF 39 RRBS AS ON 31.03.2024pateldixit.dx3Оценок пока нет

- Kyb 2023Документ10 страницKyb 2023RudraОценок пока нет

- Customer Satisfaction J&K BankДокумент42 страницыCustomer Satisfaction J&K BankSwyam DuggalОценок пока нет

- Study On The Banking Services Provided by Uttarakhand Gramin BankДокумент12 страницStudy On The Banking Services Provided by Uttarakhand Gramin BankDivyansh KaushikОценок пока нет

- Banking Sector Reforms in IndiaДокумент76 страницBanking Sector Reforms in Indialaxmi sambreОценок пока нет

- Types of Banks in IndiaДокумент3 страницыTypes of Banks in IndiaKumar NaveenОценок пока нет

- Role of Banking in India Economic For Devlopment With Reference To Icici BankДокумент116 страницRole of Banking in India Economic For Devlopment With Reference To Icici BankMayankJainОценок пока нет

- Efficacy of Regional Rural Banks (RRBS) in India: A Conventional AnalysisДокумент16 страницEfficacy of Regional Rural Banks (RRBS) in India: A Conventional AnalysisharshОценок пока нет

- Origin and Performance of Regional Rural Bank of IndiaДокумент13 страницOrigin and Performance of Regional Rural Bank of IndiaHetvi TankОценок пока нет

- Sl. No. Institution Code Institution Name: Public Sector BanksДокумент21 страницаSl. No. Institution Code Institution Name: Public Sector BanksRaja BeastmasterОценок пока нет

- Project On Rural Banking in IndiaДокумент57 страницProject On Rural Banking in IndiaMunawara 2481Оценок пока нет

- Banking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial BanksДокумент30 страницBanking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial Banksmicky=Оценок пока нет

- Impact of Karnataka Vikas Grameena Bank On Agriculture Development of Beneficiary FarmersДокумент98 страницImpact of Karnataka Vikas Grameena Bank On Agriculture Development of Beneficiary FarmersSomaling MirjeОценок пока нет

- List of Banks in India - Wikipedia, The Free EncyclopediaДокумент13 страницList of Banks in India - Wikipedia, The Free EncyclopediaAjesh Kumar MuraleedharanОценок пока нет

- Banking CompaniesДокумент2 страницыBanking CompaniesShantanu AnandОценок пока нет

- Unit - 1: Introduction To Indian Banking SystemДокумент109 страницUnit - 1: Introduction To Indian Banking SystemDr. S. Nellima KPRCAS-CommerceОценок пока нет

- Important Banking Indicators - Regional Rural Banks - OutstandingДокумент8 страницImportant Banking Indicators - Regional Rural Banks - OutstandingAkshay Yadav Student, Jaipuria LucknowОценок пока нет

- A Comparative Study of Regional Rural Banks in Chhattisgarh StateДокумент9 страницA Comparative Study of Regional Rural Banks in Chhattisgarh StateMohmmedKhayyumОценок пока нет