Вам также может понравиться

- Living TrustДокумент3 страницыLiving TrustJan Rhoneil Santillana100% (1)

- INS 21 Chapters 2-Insurers and How They Are RegulatedДокумент22 страницыINS 21 Chapters 2-Insurers and How They Are Regulatedvenki_hinfotechОценок пока нет

- Final PPT Motor TP Insurance & ClaimsДокумент57 страницFinal PPT Motor TP Insurance & ClaimsPRAKASH100% (1)

- A Cat Bond Premium Puzzle?: Financial Institutions CenterДокумент36 страницA Cat Bond Premium Puzzle?: Financial Institutions CenterchanduОценок пока нет

- Module 3 Yr. 2017Документ89 страницModule 3 Yr. 2017Xaky ODОценок пока нет

- INSURANCE & RISK MANAGEMENT - Sem3 MBA IRM-Module 2Документ41 страницаINSURANCE & RISK MANAGEMENT - Sem3 MBA IRM-Module 2Jinuachan Vadakkemulanjanal GenuachanОценок пока нет

- Reinsurance Principle and Practice CPCUДокумент9 страницReinsurance Principle and Practice CPCUNguyen Quoc HuyОценок пока нет

- HDFC LifeДокумент66 страницHDFC LifeChetan PahwaОценок пока нет

- Module 5 Yr. 2017Документ85 страницModule 5 Yr. 2017Xaky ODОценок пока нет

- Insurance and Risk ManagementДокумент140 страницInsurance and Risk Managementgg100% (1)

- INS 21 Chapter7-Risk ManagementДокумент19 страницINS 21 Chapter7-Risk Managementvenki_hinfotechОценок пока нет

- Basic of Reinsurance 03 June 21 Munch ReДокумент24 страницыBasic of Reinsurance 03 June 21 Munch ReFernand DagoudoОценок пока нет

- Claim Settlement of GICДокумент51 страницаClaim Settlement of GICSusilPandaОценок пока нет

- Fixing of Sum Insured Under Fire Insurance PoliciesДокумент17 страницFixing of Sum Insured Under Fire Insurance PoliciesShayak Kumar GhoshОценок пока нет

- Tata Aig Marine BrochureДокумент8 страницTata Aig Marine Brochurechaitanyabarge100% (2)

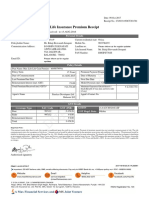

- Premium ReceiptsДокумент1 страницаPremium ReceiptsAmit KumarОценок пока нет

- Closer Script LiДокумент4 страницыCloser Script LiShiva Narayana Reddy100% (1)

- Boiler & MachineryДокумент35 страницBoiler & Machineryjoseph320@yahooОценок пока нет

- It's English That Kills YouДокумент63 страницыIt's English That Kills YouSujeet DongarjalОценок пока нет

- BABATUNDE MATTHEW OGUNLEYE Done StatementДокумент8 страницBABATUNDE MATTHEW OGUNLEYE Done StatementAleesha AleeshaОценок пока нет

- Pub Standstill Covers enДокумент22 страницыPub Standstill Covers enXitish MohantyОценок пока нет

- Postpaid Bill 7448440999 838926388Документ3 страницыPostpaid Bill 7448440999 838926388Kanth KodaliОценок пока нет

- Facultative Reinsurance PDFДокумент2 страницыFacultative Reinsurance PDFLindsay0% (1)

- Risks and Rewards For The Insurance Sector: The Big Issues, and How To Tackle ThemДокумент26 страницRisks and Rewards For The Insurance Sector: The Big Issues, and How To Tackle ThemPie DiverОценок пока нет

- Miscellaneous Manual 1Документ507 страницMiscellaneous Manual 1shrey12467% (3)

- HDFC Home LoanДокумент60 страницHDFC Home LoanSatnam SinghОценок пока нет

- Reinsurance Guidelines - Ir Guid 14 10 0017Документ11 страницReinsurance Guidelines - Ir Guid 14 10 0017Steven DreckettОценок пока нет

- Reinsurance Glossary 3Документ68 страницReinsurance Glossary 3أبو أنس - اليمنОценок пока нет

- What Is ReinsuranceДокумент7 страницWhat Is ReinsuranceDinesh RaiОценок пока нет

- Report On Non Performing Assets of BankДокумент53 страницыReport On Non Performing Assets of Bankhemali chovatiya75% (4)

- MarineДокумент48 страницMarineoxynetОценок пока нет

- Reinsurance ProjectДокумент114 страницReinsurance ProjectDattu Boga75% (12)

- Legal Framework in InsuranceДокумент36 страницLegal Framework in InsuranceHarshit Srivastava 18MBA0050Оценок пока нет

- Classification of InsuranceДокумент5 страницClassification of InsuranceRajendranath BeheraОценок пока нет

- Marine Insurance FinalДокумент21 страницаMarine Insurance FinalPratik RambhiaОценок пока нет

- Fire & Consequential Loss Insurance 57Документ15 страницFire & Consequential Loss Insurance 57surjith rОценок пока нет

- Fire Study Material - NWДокумент29 страницFire Study Material - NWDILEEP KAULОценок пока нет

- Fire ClausesДокумент62 страницыFire ClauseschriscalarionОценок пока нет

- Rate Making: How Insurance Premiums Are SetДокумент4 страницыRate Making: How Insurance Premiums Are SetSai Teja NadellaОценок пока нет

- Proportional Treaty SlipДокумент3 страницыProportional Treaty SlipAman Divya100% (1)

- Broker Tenders Guide 2015 WEBДокумент32 страницыBroker Tenders Guide 2015 WEBLestijono LastОценок пока нет

- CLAIM NOTES pdf-1 PDFДокумент9 страницCLAIM NOTES pdf-1 PDFJackson Mkwasa100% (1)

- Re InsuranceДокумент24 страницыRe InsuranceNavali Madugula100% (1)

- Fire InsuranceДокумент34 страницыFire InsuranceSaurav PandeyОценок пока нет

- Role of Actuaries & Exclusion of PerilsДокумент19 страницRole of Actuaries & Exclusion of PerilsKunal KalraОценок пока нет

- Marine and Hull InsuranceДокумент12 страницMarine and Hull InsuranceHarish NageshwaranОценок пока нет

- Aviation Fuelling Liability PdsДокумент3 страницыAviation Fuelling Liability PdsNoraini Mohd Shariff100% (1)

- ReinsuranceДокумент14 страницReinsuranceKrishnanunni VijayakumarОценок пока нет

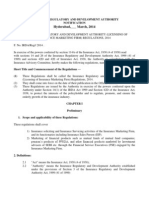

- Draft Regulations IMF Ver 2 25.3.14Документ29 страницDraft Regulations IMF Ver 2 25.3.14divyeshmodyОценок пока нет

- Vehicle InsuranceДокумент11 страницVehicle InsuranceAbhyank KumarОценок пока нет

- Aviation INSURANCE FinalДокумент53 страницыAviation INSURANCE FinalHarish AgarwalОценок пока нет

- Table No 133Документ2 страницыTable No 133ssfinservОценок пока нет

- Marine Insurance and Fire InsuranceДокумент33 страницыMarine Insurance and Fire InsuranceSuzanne Pagaduan CruzОценок пока нет

- Syllabus - Ic 88 Marketing and Public RelationsДокумент1 страницаSyllabus - Ic 88 Marketing and Public RelationsvinaykogОценок пока нет

- Machine Breakdown Insuranc Etariff RateДокумент60 страницMachine Breakdown Insuranc Etariff Rateben8_cheenathОценок пока нет

- Introduction To Re InsuranceДокумент20 страницIntroduction To Re InsurancekodavatiОценок пока нет

- Quotation - Slip - All Risk Central MedicareДокумент4 страницыQuotation - Slip - All Risk Central MedicareDtj246810Оценок пока нет

- Health Underwriting Klaus Palmen HerbertДокумент22 страницыHealth Underwriting Klaus Palmen HerberthashimОценок пока нет

- Motor OD Manual - Underwriting & Calims PDFДокумент201 страницаMotor OD Manual - Underwriting & Calims PDFMani Rathinam100% (1)

- 01 - LLMIT CH 1 Feb 08Документ18 страниц01 - LLMIT CH 1 Feb 08Pradyut TiwariОценок пока нет

- Motor Insurance Study Material FinalДокумент67 страницMotor Insurance Study Material FinalsekkilarjiОценок пока нет

- Project InsuranceДокумент13 страницProject InsuranceRohan Raj MishraОценок пока нет

- All India Fire TariffДокумент92 страницыAll India Fire Tariffkrmchandru0% (1)

- Underwriting and Ratemaking: Why Underwriting? What Is Its Purpose?Документ27 страницUnderwriting and Ratemaking: Why Underwriting? What Is Its Purpose?vijaijohn100% (1)

- Insurance ManagementДокумент76 страницInsurance ManagementDurga Prasad DashОценок пока нет

- Notes For RiДокумент25 страницNotes For Rikk kkОценок пока нет

- ReinsuranceДокумент40 страницReinsuranceAbid ParkarОценок пока нет

- ECO Data RecoveryДокумент3 страницыECO Data RecoveryDerek W SmithОценок пока нет

- Briefing Guide July Week2&3 Metrobank EMVCardsДокумент3 страницыBriefing Guide July Week2&3 Metrobank EMVCardsRafael-Cheryl Tupas-LimboОценок пока нет

- Difference Pledge MortgageДокумент6 страницDifference Pledge MortgageJeffrey Constantino Patacsil100% (1)

- Assessing Mandated Credit Programs: Case Study of The Magna Carta in The PhilippinesДокумент52 страницыAssessing Mandated Credit Programs: Case Study of The Magna Carta in The PhilippinesFlorence PanlilioОценок пока нет

- Financial Inclusion Bank of Baroda: Summer Training Project ReportДокумент102 страницыFinancial Inclusion Bank of Baroda: Summer Training Project ReportHashmi SutariyaОценок пока нет

- Chapter 6 BS 2 2PUCДокумент20 страницChapter 6 BS 2 2PUCVipin Mandyam KadubiОценок пока нет

- Rajesh Maske 2Документ3 страницыRajesh Maske 2Ashok MantreОценок пока нет

- Textile Policy Govt of Maharashtra 2011-2017Документ31 страницаTextile Policy Govt of Maharashtra 2011-2017Pradeep AhireОценок пока нет

- Chapter:-1: Vision of The CompanyДокумент64 страницыChapter:-1: Vision of The CompanyRavi ShettyОценок пока нет

- Lecture 10 Audit FinalisationДокумент21 страницаLecture 10 Audit FinalisationShibin Jayaprasad100% (1)

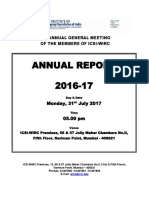

- Annual Report 2016-17: 41 Annual General Meeting of The Members of Icsi-WircДокумент42 страницыAnnual Report 2016-17: 41 Annual General Meeting of The Members of Icsi-WircParth prajapatiОценок пока нет

- E-Commerce: Slide 1-1Документ12 страницE-Commerce: Slide 1-1haleemОценок пока нет

- HDFC Bank Demat Services Offers You A Safe, Online and Seamless Platform To Keep Track of Your InvestmentsДокумент1 страницаHDFC Bank Demat Services Offers You A Safe, Online and Seamless Platform To Keep Track of Your InvestmentsBhanuprakashReddyDandavoluОценок пока нет

- Fannie Updates To Foreclosure Time FramesДокумент3 страницыFannie Updates To Foreclosure Time FramesForeclosure FraudОценок пока нет

- (In Case of Joint Accounts, Part-I (CIF) To Be Taken For Each Customer)Документ20 страниц(In Case of Joint Accounts, Part-I (CIF) To Be Taken For Each Customer)Jignesh V. KhimsuriyaОценок пока нет

- Principles and Practices of BankingДокумент57 страницPrinciples and Practices of BankingYogesh Devmore100% (1)

- Basic Banking TermsДокумент5 страницBasic Banking Termsjain_lalita89Оценок пока нет

- chp04 CevapДокумент3 страницыchp04 CevapdbjnОценок пока нет

- Insurance Capsule For NICL AOДокумент19 страницInsurance Capsule For NICL AOmanishОценок пока нет

- BOB Merger With Dena and Vijaya Bank PDFДокумент8 страницBOB Merger With Dena and Vijaya Bank PDFVijit SachdevaОценок пока нет

- Letter To Bank For Interest Certi Cate of Fixed Deposit (FD) SampleДокумент6 страницLetter To Bank For Interest Certi Cate of Fixed Deposit (FD) SampleHackerzillaОценок пока нет

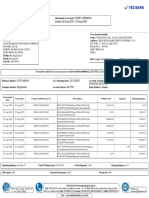

- Account Statement 22 Aug 2023-22 Aug 2023Документ2 страницыAccount Statement 22 Aug 2023-22 Aug 2023PRONAB MAJHIОценок пока нет

- Damage Claim Form R2Документ4 страницыDamage Claim Form R2hazwan jalaniОценок пока нет