Вам также может понравиться

- CH 13Документ25 страницCH 13Mariam MalallahОценок пока нет

- Investment Centers and Transfer PricingДокумент53 страницыInvestment Centers and Transfer PricingArlene DacpanoОценок пока нет

- Investment Centers and Transfer PricingДокумент23 страницыInvestment Centers and Transfer PricingWailОценок пока нет

- Chap 009Документ41 страницаChap 009jeraldtomas12Оценок пока нет

- EVA Investment Center Hilton Chapter 13Документ62 страницыEVA Investment Center Hilton Chapter 13Riedy RiandaniОценок пока нет

- Performance Measurement in Decentralized OrganizationsДокумент56 страницPerformance Measurement in Decentralized OrganizationsEman AhmedОценок пока нет

- Garrison Lecture Chapter 11Документ57 страницGarrison Lecture Chapter 11sofikhdyОценок пока нет

- Investment Centers and Transfer PricingДокумент61 страницаInvestment Centers and Transfer PricingIman NessaОценок пока нет

- Unit - 6 محاسبه اداريهДокумент47 страницUnit - 6 محاسبه اداريهsuperstreem.9Оценок пока нет

- Chapter 11Документ61 страницаChapter 11Samaaraa NorОценок пока нет

- Week 10 ImaДокумент49 страницWeek 10 ImaWai Ying LaiОценок пока нет

- Chapter 11 PDFДокумент65 страницChapter 11 PDFAftarur Rahaman AnikОценок пока нет

- 4e NBG CH12 SMДокумент72 страницы4e NBG CH12 SM胡振猷Оценок пока нет

- CH09Документ62 страницыCH09Lê Chấn PhongОценок пока нет

- MINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDДокумент22 страницыMINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDamoyyОценок пока нет

- Chap013 TNx2Документ69 страницChap013 TNx2Ashesh DasОценок пока нет

- Measuring and Controlling Assets EmployedДокумент30 страницMeasuring and Controlling Assets EmployedRhaymond MonterdeОценок пока нет

- Cap 8 Performance CH09 SM 1Документ61 страницаCap 8 Performance CH09 SM 1Lê Chấn PhongОценок пока нет

- Performance Evaluation in The Decentralized FirmДокумент38 страницPerformance Evaluation in The Decentralized FirmNana LeeОценок пока нет

- Introduction To Managerial Accounting 6th Edition Brewer Solutions ManualДокумент63 страницыIntroduction To Managerial Accounting 6th Edition Brewer Solutions Manualgiaocleopatra192y100% (35)

- Ch11accessible 200101213935 PDFДокумент61 страницаCh11accessible 200101213935 PDFسامر الخطيبОценок пока нет

- Performance Evaluation in The Decentralized FirmДокумент38 страницPerformance Evaluation in The Decentralized FirmMuhammad Rusydi AzizОценок пока нет

- Introduction To Managerial Accounting 7th Edition Brewer Solutions ManualДокумент63 страницыIntroduction To Managerial Accounting 7th Edition Brewer Solutions Manualgiaocleopatra192y100% (27)

- Performance Evaluation in The Decentralized FirmДокумент55 страницPerformance Evaluation in The Decentralized FirmIstiq OmahОценок пока нет

- Investment Centers and Transfer Pricing: Answers To Review QuestionsДокумент45 страницInvestment Centers and Transfer Pricing: Answers To Review QuestionsShey INFTОценок пока нет

- Division Performance MeasurementДокумент31 страницаDivision Performance MeasurementKetan DedhaОценок пока нет

- Investment Centers and Transfer Pricing: Answers To Review QuestionsДокумент43 страницыInvestment Centers and Transfer Pricing: Answers To Review QuestionsYong RenОценок пока нет

- CMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Документ39 страницCMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Henok FikaduОценок пока нет

- Accounting & Control: Cost ManagementДокумент40 страницAccounting & Control: Cost ManagementMeriskaОценок пока нет

- Accounting & Control: Cost ManagementДокумент40 страницAccounting & Control: Cost ManagementBusiness MatterОценок пока нет

- Pusat Prtanggung Jawaban Dan Transfer PricingДокумент40 страницPusat Prtanggung Jawaban Dan Transfer PricingmayaОценок пока нет

- Thirteen: Investment Centers and Transfer PricingДокумент63 страницыThirteen: Investment Centers and Transfer PricingDenОценок пока нет

- Control: The Management Control EnvironmentДокумент49 страницControl: The Management Control EnvironmentvinnaОценок пока нет

- ch13 Akuntansi ManajemenДокумент38 страницch13 Akuntansi ManajemenNabila NurmalitasariОценок пока нет

- Hilton MA 12e Chap013Документ43 страницыHilton MA 12e Chap013cmxzerostartОценок пока нет

- Decentralization: Mcgraw-Hill /irwinДокумент53 страницыDecentralization: Mcgraw-Hill /irwinYHОценок пока нет

- Performance Evaluation ROI-RI-EVAДокумент42 страницыPerformance Evaluation ROI-RI-EVAraghavendra_20835414Оценок пока нет

- Roi, RiДокумент17 страницRoi, RiGalan PagehgiriОценок пока нет

- Chapter 11 PDFДокумент66 страницChapter 11 PDFSyed Atiq TurabiОценок пока нет

- Divisional Performance Measures and Transfer Pricing NotesДокумент83 страницыDivisional Performance Measures and Transfer Pricing NotesShreya PatelОценок пока нет

- ROI Pak DhaniДокумент26 страницROI Pak DhaniCahya PerdanaОценок пока нет

- Performance Evaluation in Decentralized FirmsДокумент27 страницPerformance Evaluation in Decentralized FirmsXinjie MaОценок пока нет

- L 6 Performance MeasurementДокумент14 страницL 6 Performance MeasurementMist FactorОценок пока нет

- CH 10Документ37 страницCH 10billybuttonОценок пока нет

- Operating and Financial LeverageДокумент31 страницаOperating and Financial LeveragebharatОценок пока нет

- Topic 6 (PMS 1)Документ41 страницаTopic 6 (PMS 1)Nero ShaОценок пока нет

- Performance Mesurement of OrganizationДокумент10 страницPerformance Mesurement of OrganizationbbasОценок пока нет

- 2008 Acct 212 Chapter 10 Resp Accg NotesДокумент6 страниц2008 Acct 212 Chapter 10 Resp Accg NotesBrandon HookerОценок пока нет

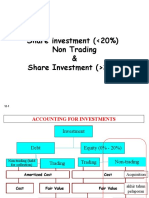

- 12.2 Share Investment Non Trading & Share Invesment Lebih 20%Документ18 страниц12.2 Share Investment Non Trading & Share Invesment Lebih 20%TIFFANNY SHELIAОценок пока нет

- Topic 6 (PMS 1)Документ40 страницTopic 6 (PMS 1)Thiba 2772Оценок пока нет

- Accounts PresentationДокумент16 страницAccounts PresentationsansarwalОценок пока нет

- ACT2121 Lecture 19 Responsibility AccountingДокумент49 страницACT2121 Lecture 19 Responsibility Accountingalangoo200Оценок пока нет

- Chap 013Документ49 страницChap 013palak32100% (1)

- Investment Centers and Transfer Pricing: Mcgraw-Hill/IrwinДокумент59 страницInvestment Centers and Transfer Pricing: Mcgraw-Hill/IrwinEljo PleqiОценок пока нет

- Responsibility AccountingДокумент32 страницыResponsibility AccountingSyed WaqasОценок пока нет

- Responsibility AccountingДокумент20 страницResponsibility AccountingaddityarajОценок пока нет

- Segment Reporting, Decentralization and The Balanced ScorecardДокумент20 страницSegment Reporting, Decentralization and The Balanced ScorecardSneha SureshОценок пока нет

- ACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilityДокумент5 страницACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilitySayadi AdiihОценок пока нет

- 5responsibility AccountingДокумент43 страницы5responsibility AccountingSayadi AdiihОценок пока нет

- Chapter 07S SlidesДокумент25 страницChapter 07S SlidesSayadi AdiihОценок пока нет

- Segment Reporting and Decentralization: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeДокумент69 страницSegment Reporting and Decentralization: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeSayadi AdiihОценок пока нет

- Garrison Lecture Chapter 11Документ57 страницGarrison Lecture Chapter 11sofikhdyОценок пока нет

- Tha Balanced ScorecardДокумент32 страницыTha Balanced ScorecardSayadi Adiih100% (1)

- Garrison Lecture Chapter 11Документ57 страницGarrison Lecture Chapter 11sofikhdyОценок пока нет

- Multi-Product Break-Even Point Formula: Margin and Weighted Average Contribution Margin Ratio Are UsedДокумент2 страницыMulti-Product Break-Even Point Formula: Margin and Weighted Average Contribution Margin Ratio Are UsedSayadi AdiihОценок пока нет

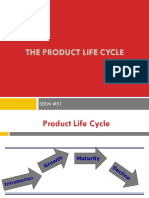

- The Product Life CycleДокумент10 страницThe Product Life CycleSayadi AdiihОценок пока нет

- Account Statement: MCB Bank LimitedДокумент1 страницаAccount Statement: MCB Bank LimitedAdmob Hunter 1250% (2)

- Computer Literacy Test 3Документ9 страницComputer Literacy Test 3Xavier MundattilОценок пока нет

- Prelim ExamДокумент13 страницPrelim ExamNah HamzaОценок пока нет

- Am113 Module 1-PrelimДокумент22 страницыAm113 Module 1-PrelimMaryjel SumambotОценок пока нет

- FINS1613 File 04 - All 3 Topics Practice Questions PDFДокумент16 страницFINS1613 File 04 - All 3 Topics Practice Questions PDFisy campbellОценок пока нет

- Budget 2024 HighlightsДокумент14 страницBudget 2024 HighlightsSunnyОценок пока нет

- Futures ContractsДокумент14 страницFutures ContractsSantosh More0% (1)

- STCM 04 Ge CVPДокумент2 страницыSTCM 04 Ge CVPdin matanguihanОценок пока нет

- Shil Gift Tax Chapter End SolutionДокумент3 страницыShil Gift Tax Chapter End SolutionMD. MUSTARIKUL ISLAM RAJUОценок пока нет

- A Cat Bond Premium Puzzle?: Financial Institutions CenterДокумент36 страницA Cat Bond Premium Puzzle?: Financial Institutions CenterchanduОценок пока нет

- Rein Hardware StoreДокумент2 страницыRein Hardware StoreMariñas, Romalyn D.Оценок пока нет

- Ratio Analysis of Shree Cement and Ambuja Cement Project Report 2Документ7 страницRatio Analysis of Shree Cement and Ambuja Cement Project Report 2Dale 08Оценок пока нет

- Excel Drill - CAPM & WACCДокумент8 страницExcel Drill - CAPM & WACCgjlastimozaОценок пока нет

- A Study On Financial Statement Analysis of Tata Steel Odisha Project, Kalinga NagarДокумент12 страницA Study On Financial Statement Analysis of Tata Steel Odisha Project, Kalinga Nagargmb117Оценок пока нет

- Unifi Capital PresentationДокумент40 страницUnifi Capital PresentationAnkurОценок пока нет

- Fundamental Analysis - Definition, Types, Benefits, and How To DoДокумент5 страницFundamental Analysis - Definition, Types, Benefits, and How To Dohavo lavoОценок пока нет

- List of Countries by GDP (Nominal)Документ13 страницList of Countries by GDP (Nominal)hoogggleeeОценок пока нет

- Business PlanДокумент5 страницBusiness PlanColegiul de Constructii din HincestiОценок пока нет

- Funds Flow AnalysisДокумент105 страницFunds Flow AnalysisAmjad Khan100% (2)

- Bad Debts - CE and DSE - AnswerДокумент3 страницыBad Debts - CE and DSE - AnswerKwan Yin HoОценок пока нет

- ISA 315 & ISA 240 (Fraud and Risk)Документ54 страницыISA 315 & ISA 240 (Fraud and Risk)Joe SmithОценок пока нет

- Chapter 7Документ46 страницChapter 7Awrangzeb AwrangОценок пока нет

- MAA716 - T2 - 2012 v2Документ11 страницMAA716 - T2 - 2012 v2ssusasi4769Оценок пока нет

- Walt Disney Financial StatementДокумент8 страницWalt Disney Financial StatementShaReyОценок пока нет

- IFR AsiaДокумент44 страницыIFR AsiaFernando LopezОценок пока нет

- Cooperative ManualДокумент35 страницCooperative ManualPratik MogheОценок пока нет

- USDA USFS Nursery Manual For Native Plants - A Guide For Tribal Nurseries - Nursery Management Nursery Manual For Native Plants by United States Department of Agriculture - U.S. Forest Service PDFДокумент309 страницUSDA USFS Nursery Manual For Native Plants - A Guide For Tribal Nurseries - Nursery Management Nursery Manual For Native Plants by United States Department of Agriculture - U.S. Forest Service PDFGreg John Peterson100% (2)

- Wachemo University School of Computing and Informatics Department of Computer Science Entrepreneurship Business PlanДокумент9 страницWachemo University School of Computing and Informatics Department of Computer Science Entrepreneurship Business PlanAbe BerhieОценок пока нет

- Microsoft Assignment FRA Group 7Документ5 страницMicrosoft Assignment FRA Group 7Payal AgrawalОценок пока нет

- PassportДокумент1 страницаPassportzjf4t2rkyrОценок пока нет