Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Introduction To Operations and Supply Chain ManagementДокумент42 страницыIntroduction To Operations and Supply Chain Managementdiyaalkhazraji1290% (1)

- Mexican Food: BBC Learning English London LifeДокумент3 страницыMexican Food: BBC Learning English London LifedoinalisneacОценок пока нет

- SWOT Analysis: StrengthsДокумент4 страницыSWOT Analysis: Strengthsassign hub100% (1)

- LSCMДокумент9 страницLSCMVishnu Sri Harsha MulakalaОценок пока нет

- Handicap Clothing ConversionДокумент5 страницHandicap Clothing Conversionaccessaudio100% (4)

- Q3 Dressmaking 9 W 5Документ7 страницQ3 Dressmaking 9 W 5jac cabonilasОценок пока нет

- Consumer and Organizational MarketsДокумент26 страницConsumer and Organizational MarketsMaryjoy Valerio0% (1)

- Gap Analysis Report For Keya - Group (MM & WM)Документ12 страницGap Analysis Report For Keya - Group (MM & WM)shetupucОценок пока нет

- F02-003i4 Loose Tube Cable Mid-Span Access LS 2Документ4 страницыF02-003i4 Loose Tube Cable Mid-Span Access LS 2amir11601Оценок пока нет

- NearPhysical VolumeIIДокумент495 страницNearPhysical VolumeIImasterborОценок пока нет

- Demand For Goods and Services UpdateДокумент8 страницDemand For Goods and Services UpdateKhai VeChainОценок пока нет

- Factors Affecting Mayur Suitings SalesДокумент88 страницFactors Affecting Mayur Suitings SalesSwapnil KadamОценок пока нет

- Global Toy Safety Standards Manual (TUV) PDFДокумент15 страницGlobal Toy Safety Standards Manual (TUV) PDFEugene PaiОценок пока нет

- Tattoo AirbrushДокумент9 страницTattoo AirbrushSimona WingОценок пока нет

- Saravana Bhavan KuwaitДокумент7 страницSaravana Bhavan KuwaitkkpaliathОценок пока нет

- A Project Report On Leisure WearДокумент20 страницA Project Report On Leisure WearBratesh PradhanОценок пока нет

- Lit en DPP Catalogue 2Документ76 страницLit en DPP Catalogue 2Karina ChristiОценок пока нет

- Iso 20471-2013-04Документ34 страницыIso 20471-2013-04Mahmoud MoussaОценок пока нет

- A Study On The Effects of High Heels On Women: Purti Wakankar LDVДокумент12 страницA Study On The Effects of High Heels On Women: Purti Wakankar LDVShivani SharmaОценок пока нет

- Master SMV Sheet Machinist OperationsДокумент9 страницMaster SMV Sheet Machinist OperationsMD JAWED AKHTARОценок пока нет

- Panasonic NA 107VC4Документ40 страницPanasonic NA 107VC4killerhAPPyОценок пока нет

- Sarah Browne, A Model Society, Patterns & Thoughts, 2008Документ52 страницыSarah Browne, A Model Society, Patterns & Thoughts, 2008Sarah BrowneОценок пока нет

- Group Project on E-Commerce in IndiaДокумент53 страницыGroup Project on E-Commerce in IndiaAmit Singh100% (2)

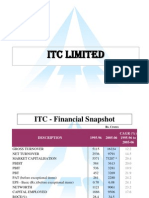

- ITCДокумент47 страницITCHarshit KatwalaОценок пока нет

- Encore 300 - Fuel Dispenser & PumpsДокумент6 страницEncore 300 - Fuel Dispenser & Pumpsgilbarcomarketing123Оценок пока нет

- Portwest Hats PS53Документ2 страницыPortwest Hats PS53Arun RavindranОценок пока нет

- Informe Milka Case StudyДокумент5 страницInforme Milka Case StudyCesar D. VillanuevaОценок пока нет

- Brand EquityДокумент4 страницыBrand EquityKumar MaheshОценок пока нет

- MIGMax 140 WelderДокумент32 страницыMIGMax 140 WelderVooDooJake100% (1)

- Asias Temples of LuxuryДокумент7 страницAsias Temples of Luxuryjasonvulog3626Оценок пока нет