Вам также может понравиться

- Chirag Jogi's Private Tuitions 9594222309Документ10 страницChirag Jogi's Private Tuitions 9594222309Chirag JogiОценок пока нет

- Session 7 Ledgers 4 - Inventory (Stock)Документ5 страницSession 7 Ledgers 4 - Inventory (Stock)ol.iv.e.a.gui.l.ar412Оценок пока нет

- Double Entry BookДокумент4 страницыDouble Entry BookDamith Piumal PereraОценок пока нет

- Ch-6 (Expenses, Sales, Drawing)Документ16 страницCh-6 (Expenses, Sales, Drawing)Kie RubyjaneОценок пока нет

- Returns Inwards and Returns Outwards JournalДокумент15 страницReturns Inwards and Returns Outwards Journaldrishti.singh0609Оценок пока нет

- Accounting For Merchandising CompaniesДокумент40 страницAccounting For Merchandising CompaniesAnonymous mnAAXLkYQCОценок пока нет

- Accounting For Merchandising CompaniesДокумент40 страницAccounting For Merchandising CompaniesAnonymous mnAAXLkYQC100% (1)

- Accounting For Merchandising Operations: HOSP 1210 (Financial Acct) Learning CentreДокумент4 страницыAccounting For Merchandising Operations: HOSP 1210 (Financial Acct) Learning CentreHuening KaiОценок пока нет

- Topic 3 Recording of Data - Double Entry SystemДокумент57 страницTopic 3 Recording of Data - Double Entry SystemJonisОценок пока нет

- Chapter-5: Accounting For Merchandising OperationsДокумент36 страницChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamОценок пока нет

- Periodic Methods of AccountingДокумент40 страницPeriodic Methods of AccountingKiasatina Amalia MustafaОценок пока нет

- Account Receivable ClassДокумент30 страницAccount Receivable ClassBeast aОценок пока нет

- Account Receivable ClassДокумент30 страницAccount Receivable ClassBeast aОценок пока нет

- Accounting For ReceivablesДокумент49 страницAccounting For Receivablesdwi studyОценок пока нет

- CH 5 Returns, Discounts and Sales Tax N5Документ16 страницCH 5 Returns, Discounts and Sales Tax N5Soputivong NhemОценок пока нет

- Chapter 3Документ37 страницChapter 3ENG ZI QINGОценок пока нет

- Accounting Treatment of Bill of Exchange:: Explanation With An ExampleДокумент2 страницыAccounting Treatment of Bill of Exchange:: Explanation With An ExampleSmith F. JohnОценок пока нет

- Tally NotesДокумент32 страницыTally NotesenuОценок пока нет

- Worksheet - Unit 3 - Double Entry Accounting - Part 2Документ3 страницыWorksheet - Unit 3 - Double Entry Accounting - Part 2LearnJa Online SchoolОценок пока нет

- Chirag Jogi's Private Tuitions 9594222309Документ8 страницChirag Jogi's Private Tuitions 9594222309Chirag JogiОценок пока нет

- Lesson 3Документ9 страницLesson 3Yin YinОценок пока нет

- 4-Accounting Problems-Journal and LedgerДокумент40 страниц4-Accounting Problems-Journal and LedgerPriya RanjanОценок пока нет

- Purchases and Purchases JournalДокумент38 страницPurchases and Purchases Journaljannat farooqiОценок пока нет

- Chapter 5 AccountingДокумент23 страницыChapter 5 AccountingShania PersaudОценок пока нет

- Accounting For Receivables: Weygandt - Kieso - KimmelДокумент49 страницAccounting For Receivables: Weygandt - Kieso - KimmelHaftom YitbarekОценок пока нет

- Ud. Surya Prabhu (Titipan 2) Desy TrianaДокумент38 страницUd. Surya Prabhu (Titipan 2) Desy TrianaDESY TRIANAОценок пока нет

- Chapter 6 Accounting Equations: Short Answer QuestionДокумент16 страницChapter 6 Accounting Equations: Short Answer QuestionSaransh BattaОценок пока нет

- Worksheet - Unit 3 - Double Entry Accounting - Part 2Документ3 страницыWorksheet - Unit 3 - Double Entry Accounting - Part 2LearnJa Online SchoolОценок пока нет

- Adeup CoДокумент5 страницAdeup CoPavan RaiОценок пока нет

- Tutorial Test 06: RequirementsДокумент2 страницыTutorial Test 06: RequirementsLan Hương NguyễnОценок пока нет

- Unit 1: Assessment ExercisesДокумент2 страницыUnit 1: Assessment ExercisesJaved MushtaqОценок пока нет

- Chapter 3Документ31 страницаChapter 3EricKHLeawОценок пока нет

- Assessment Accounting - Exercise-U1Документ5 страницAssessment Accounting - Exercise-U1Anam KhanОценок пока нет

- Ud PrabhuДокумент27 страницUd PrabhunidaОценок пока нет

- Accounting For MerchandisingДокумент2 страницыAccounting For MerchandisingEvelyn MaligayaОценок пока нет

- CH 5 - Returns, Discounts and Sales Tax - UpdatedДокумент31 страницаCH 5 - Returns, Discounts and Sales Tax - Updatedgolooz43Оценок пока нет

- Accounting PrinciplesДокумент36 страницAccounting PrinciplesEshetieОценок пока нет

- (Problems) - Audit of InventoriesДокумент22 страницы(Problems) - Audit of Inventoriesapatos40% (5)

- Accounting Double EntryДокумент6 страницAccounting Double EntryAyaz NujuraullyОценок пока нет

- Accounting Principles: Second Canadian EditionДокумент36 страницAccounting Principles: Second Canadian EditionKerby Gail RulonaОценок пока нет

- Chapter 4 - Recording and Summarizing TransactionsДокумент56 страницChapter 4 - Recording and Summarizing Transactionsshemida60% (5)

- Module 1 - Credit Bad DebtsДокумент21 страницаModule 1 - Credit Bad Debtsiacpa.aialmeОценок пока нет

- Accounting For Merchandising OperationsДокумент5 страницAccounting For Merchandising OperationsatoydequitОценок пока нет

- Financial Accounting (Lecture 10)Документ31 страницаFinancial Accounting (Lecture 10)Khaleeq AhmedОценок пока нет

- Chapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentДокумент3 страницыChapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentAshlene CruzОценок пока нет

- 9 ACCOUNTS FINAL REVISION Semester 1Документ5 страниц9 ACCOUNTS FINAL REVISION Semester 1bimbel.3hОценок пока нет

- Financial&managerial Accounting - 15e Williamshakabettner Chap 6Документ15 страницFinancial&managerial Accounting - 15e Williamshakabettner Chap 6mzqace100% (1)

- Credit Notes, Refunds, and DiscountsДокумент30 страницCredit Notes, Refunds, and Discountsdivya kalyaniОценок пока нет

- Accounting EquationДокумент12 страницAccounting EquationriaОценок пока нет

- Chapter3 Auditing 2Документ10 страницChapter3 Auditing 2lilis100% (4)

- Ch05 Accounting For Merchandising Business2Документ30 страницCh05 Accounting For Merchandising Business2Kader AbdiОценок пока нет

- Accounting EquationДокумент38 страницAccounting EquationAdelyn DizonОценок пока нет

- Chapter 2-1: Using T Accounts / Analyzing The Accounting EquationДокумент23 страницыChapter 2-1: Using T Accounts / Analyzing The Accounting EquationGarrett JohnsonОценок пока нет

- Handouts Session 4Документ5 страницHandouts Session 4Allaisa Mae JacobОценок пока нет

- Introduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtДокумент38 страницIntroduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtMuhammad FaisalОценок пока нет

- Chapter 4 - Accounting For Merchandising (Slide Notes)Документ27 страницChapter 4 - Accounting For Merchandising (Slide Notes)NUR BALQIS BINTI MOHD TAJUDDIN BGОценок пока нет

- Chap 4 Books of Prime EntryДокумент29 страницChap 4 Books of Prime EntrynabkillОценок пока нет

- Lecture 2 Second Year Financial Accounting: Merchandising Operation 1Документ40 страницLecture 2 Second Year Financial Accounting: Merchandising Operation 1sara100% (1)

- Cambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersОт EverandCambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersРейтинг: 2 из 5 звезд2/5 (4)

- Ca$h is Fact: Implementing a Credit and Collections Policy From Application to Payment and BeyondОт EverandCa$h is Fact: Implementing a Credit and Collections Policy From Application to Payment and BeyondОценок пока нет

- Accounting Presentation - TurrabДокумент20 страницAccounting Presentation - Turrabits2koolОценок пока нет

- 7707 Scheme of Work (For Examination From 2020)Документ34 страницы7707 Scheme of Work (For Examination From 2020)its2koolОценок пока нет

- PSArips.com.txtДокумент1 страницаPSArips.com.txtits2koolОценок пока нет

- WorksheetДокумент3 страницыWorksheetits2koolОценок пока нет

- X-Ray Chest PA ViewДокумент1 страницаX-Ray Chest PA Viewits2koolОценок пока нет

- Accounting For Inventory - Momin WaliДокумент12 страницAccounting For Inventory - Momin Waliits2koolОценок пока нет

- Activity Based LearningДокумент28 страницActivity Based Learningits2koolОценок пока нет

- Admission Application FormДокумент14 страницAdmission Application Formits2koolОценок пока нет

- 9 TH - Extra PaperДокумент9 страниц9 TH - Extra Paperits2koolОценок пока нет

- 1300 Math Formulas - Alex SvirinДокумент338 страниц1300 Math Formulas - Alex SvirinMirnesОценок пока нет

- IG 4 - Pre SessionalДокумент2 страницыIG 4 - Pre Sessionalits2koolОценок пока нет

- Extracted Pages From Frank Wood S Business Accounting 1Документ1 страницаExtracted Pages From Frank Wood S Business Accounting 1its2koolОценок пока нет

- 00-T Accounts Btech PDFДокумент1 страница00-T Accounts Btech PDFits2koolОценок пока нет

- Queen ElizabethДокумент1 страницаQueen Elizabethits2koolОценок пока нет

- IG3, O3 - Doubtdul DebtsДокумент2 страницыIG3, O3 - Doubtdul Debtsits2koolОценок пока нет

- Sample AssignmentДокумент31 страницаSample Assignmentits2kool50% (2)

- What Is AccountingДокумент13 страницWhat Is Accountingits2koolОценок пока нет

- Assignment For Managing Financial Resources and Decisions.22490Документ9 страницAssignment For Managing Financial Resources and Decisions.22490vanvitloveОценок пока нет

- Sources of Finance - MFRDДокумент23 страницыSources of Finance - MFRDits2kool100% (1)

- Mango's Risk Register: How To Use This RegisterДокумент3 страницыMango's Risk Register: How To Use This Registerits2koolОценок пока нет

- Assignment For Managing Financial Resources and Decisions.22490Документ9 страницAssignment For Managing Financial Resources and Decisions.22490vanvitloveОценок пока нет

- Run For Your Life Group Task - FinalДокумент4 страницыRun For Your Life Group Task - Finalits2koolОценок пока нет

- O Level Accounts Notes - All PagesДокумент59 страницO Level Accounts Notes - All Pagesits2kool92% (224)

- Tafseer Ibn-e-Kaseer - Fehrist PageДокумент34 страницыTafseer Ibn-e-Kaseer - Fehrist PagePakistan Digital LibraryОценок пока нет

- Payroll DocumentationДокумент2 страницыPayroll Documentationits2kool100% (1)

- Head of Education Uk PakistanДокумент4 страницыHead of Education Uk Pakistanits2koolОценок пока нет

- Business Growth BasicsДокумент6 страницBusiness Growth Basicsits2koolОценок пока нет

- Higher Algebra - Hall & KnightДокумент593 страницыHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Basic Reconciliation StatementДокумент13 страницBasic Reconciliation StatementEaster Adina-LumangОценок пока нет

- 49 Agro Conglomerate Vs CAДокумент5 страниц49 Agro Conglomerate Vs CACharm Divina LascotaОценок пока нет

- 0204 Part A DCHB Kullu PDFДокумент362 страницы0204 Part A DCHB Kullu PDFsoumi mitraОценок пока нет

- GA Tax GuideДокумент46 страницGA Tax Guidedamilano1Оценок пока нет

- G.R. No. 187769 (Digest)Документ6 страницG.R. No. 187769 (Digest)Davy Pats100% (1)

- Cabuhat v. CAДокумент2 страницыCabuhat v. CALiana AcubaОценок пока нет

- Finance Interview QuestionsДокумент5 страницFinance Interview QuestionsdrjoestanОценок пока нет

- ONE IBC LIMITED - Bank Wire Payment Instructions USD + EUR Updated 26 Dec 2018Документ4 страницыONE IBC LIMITED - Bank Wire Payment Instructions USD + EUR Updated 26 Dec 2018dothanhtungОценок пока нет

- Obli Con CasesДокумент38 страницObli Con CasesIyahОценок пока нет

- Customer Management and Organizational Performance of Banking Sector - A Case Study of Commercial Bank of Ethiopia Haramaya Branch and Harar BranchesДокумент10 страницCustomer Management and Organizational Performance of Banking Sector - A Case Study of Commercial Bank of Ethiopia Haramaya Branch and Harar BranchesAlexander DeckerОценок пока нет

- BA5011 - Merchant Banking and Financial Services Assignment-1Документ6 страницBA5011 - Merchant Banking and Financial Services Assignment-1PREETHA SHERI GОценок пока нет

- Tender Schedule For The Work Of: Cauvery Neeravari Nigama LimitedДокумент309 страницTender Schedule For The Work Of: Cauvery Neeravari Nigama LimitednischalОценок пока нет

- LockBox Doc For TrainingДокумент15 страницLockBox Doc For Trainingankish77100% (1)

- Accounts NotesДокумент482 страницыAccounts NotesVishnuReddyОценок пока нет

- Контракт в ВордеДокумент16 страницКонтракт в ВордеDavid Lee100% (10)

- Assignment of Islamic FinanceДокумент20 страницAssignment of Islamic FinanceHeena Ch100% (1)

- Jones Finac Ce ch02 PDFДокумент32 страницыJones Finac Ce ch02 PDFAnonymous HumanОценок пока нет

- Internship ReportДокумент13 страницInternship ReportSuraksha Koirala50% (6)

- Name Family Members & Friends Phone NombersДокумент36 страницName Family Members & Friends Phone NombersNagaraj HalabhaviОценок пока нет

- Mobile Banking Application FormДокумент1 страницаMobile Banking Application FormMohd QuddusОценок пока нет

- Business Plan IT (Oman)Документ13 страницBusiness Plan IT (Oman)Zohair KhanОценок пока нет

- Nri Banking 11Документ45 страницNri Banking 11dalvishweta100% (1)

- Bangko Sentral NG PilipinasДокумент59 страницBangko Sentral NG PilipinasAnn balledosОценок пока нет

- PNB vs. Reyes - Annulment of REMДокумент2 страницыPNB vs. Reyes - Annulment of REMTheodore0176100% (1)

- Economic SlowdownДокумент10 страницEconomic SlowdownPrapti JainОценок пока нет

- Ncnda BDG DiamondДокумент6 страницNcnda BDG DiamondPenny100% (1)

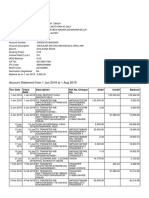

- Account Statement From 1 Jan 2019 To 1 Aug 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыAccount Statement From 1 Jan 2019 To 1 Aug 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSaurabh SinghОценок пока нет

- Pay Men Tech Response MessagesДокумент16 страницPay Men Tech Response MessagesMahesh Nakhate100% (1)

- Test Bank For Investments 12th Edition Zvi Bodie Alex Kane Alan MarcusДокумент39 страницTest Bank For Investments 12th Edition Zvi Bodie Alex Kane Alan MarcusAddison Rogers100% (35)