Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- RMC No. 14-2021Документ1 страницаRMC No. 14-2021nathalie velasquezОценок пока нет

- Minimum Alternate Tax Section 115JbДокумент17 страницMinimum Alternate Tax Section 115JbEmeline SoroОценок пока нет

- Goods and Service Tax Act, 2017Документ4 страницыGoods and Service Tax Act, 2017shivani yadavОценок пока нет

- Mulch Sale FlyerДокумент2 страницыMulch Sale Flyerbsatroop776100% (2)

- 2015 Taxation Law - Atty Noel Ortega PDFДокумент28 страниц2015 Taxation Law - Atty Noel Ortega PDFViner VillariñaОценок пока нет

- The Transfer Pricing Law Review - Edition 3 - 24 July 2019Документ327 страницThe Transfer Pricing Law Review - Edition 3 - 24 July 2019Sandi Zanz0% (1)

- Public Debt FlowchartДокумент1 страницаPublic Debt FlowchartRbОценок пока нет

- Getting Paid Math ScoglandДокумент3 страницыGetting Paid Math Scoglandapi-26781533414% (7)

- Annual Report 15Документ196 страницAnnual Report 15Mani SinghОценок пока нет

- POS301.R - Topic7Worksheet-8-29-16 CompleteДокумент3 страницыPOS301.R - Topic7Worksheet-8-29-16 Completetama00018Оценок пока нет

- Secure Act 2 - 0 2023 SIEДокумент4 страницыSecure Act 2 - 0 2023 SIEHenry Jose Codallo SisoОценок пока нет

- Tax 301 Module 1Документ39 страницTax 301 Module 1LENLYN FALAMIGОценок пока нет

- P U P College of Accountancy and FinanceДокумент2 страницыP U P College of Accountancy and FinanceFaithful Word Baptist ChurchОценок пока нет

- IncomeДокумент4 страницыIncomeapi-3839889Оценок пока нет

- Pressco Case SolutionДокумент6 страницPressco Case SolutionAashna MehtaОценок пока нет

- Jawaban 2Документ43 страницыJawaban 2pitoyo sssОценок пока нет

- Something For Nothing Understanding TIFДокумент8 страницSomething For Nothing Understanding TIFSandra FlorezОценок пока нет

- ISE 2040 Excel HWДокумент20 страницISE 2040 Excel HWPatch HavanasОценок пока нет

- Singapore Tax GuideДокумент20 страницSingapore Tax GuideTaccad ReydennОценок пока нет

- CTA CasesДокумент177 страницCTA CasesJade Palace TribezОценок пока нет

- LD AccountДокумент5 страницLD AccountYandisa Ngaleka0% (1)

- Actividad 1Документ2 страницыActividad 1Diana Marcela MONCADA SUAREZОценок пока нет

- Alorica - Angelo May 13Документ1 страницаAlorica - Angelo May 13bktsuna0201Оценок пока нет

- Cash To Be Collected: EkartДокумент1 страницаCash To Be Collected: EkartE-World PlazaОценок пока нет

- Revised January 1992 Daily Wage PayrollДокумент4 страницыRevised January 1992 Daily Wage PayrollJhem Martinez100% (1)

- SMART Notes ACCA F6 (40 Pages) FA18 Upto March 2020Документ42 страницыSMART Notes ACCA F6 (40 Pages) FA18 Upto March 2020Jasna Rose Roses100% (1)

- Republic V Dela RamaДокумент2 страницыRepublic V Dela RamaKarenliambrycejego Ragragio100% (2)

- Principles of Taxation LawДокумент11 страницPrinciples of Taxation LawPrashikshan UlakОценок пока нет

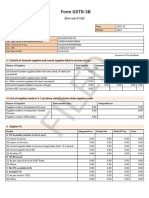

- GSTR3B 03alnpk4728k1zv 042021Документ2 страницыGSTR3B 03alnpk4728k1zv 042021Harish VermaОценок пока нет

- Income Taxation Quiz 1Документ2 страницыIncome Taxation Quiz 1Yi Zara100% (1)