Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- HIPPA TrainingДокумент29 страницHIPPA Trainingaadi100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- SOX With ISO 27001 & 27002 Mapping AuditsДокумент18 страницSOX With ISO 27001 & 27002 Mapping Auditshumdil0% (1)

- IT General ControlsДокумент18 страницIT General ControlsAtulOsaveОценок пока нет

- Worksheet For Bank Reconciliation - 8 PDFДокумент2 страницыWorksheet For Bank Reconciliation - 8 PDFsanele dlaminiОценок пока нет

- Isms Internal AuditДокумент10 страницIsms Internal AuditGayathri RachakondaОценок пока нет

- General Journal SampleДокумент2 страницыGeneral Journal SampleBusinessTips.Ph89% (19)

- Nigerian Financial System OverviewДокумент9 страницNigerian Financial System OverviewHayatu A. NuhuОценок пока нет

- ISMS Statement of Applicability For ISMS Course Participant ExerciseДокумент12 страницISMS Statement of Applicability For ISMS Course Participant ExerciseCyber Guru100% (1)

- EFM Three Statement ModelДокумент5 страницEFM Three Statement ModelAmr El-BelihyОценок пока нет

- Absorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualДокумент20 страницAbsorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualPatrick LanceОценок пока нет

- Essential Legal Issues for E-Commerce BusinessesДокумент35 страницEssential Legal Issues for E-Commerce BusinessesSyed Ahmed AliОценок пока нет

- Anten Theor BasicsДокумент99 страницAnten Theor BasicsaadiОценок пока нет

- Network SecurityДокумент76 страницNetwork SecurityaadiОценок пока нет

- Science - Technology Part 2 PDFДокумент67 страницScience - Technology Part 2 PDFaadiОценок пока нет

- A Survey of Image Steganography TechniquesДокумент12 страницA Survey of Image Steganography TechniquesDrMadhuravani PeddiОценок пока нет

- Parliament BillsДокумент6 страницParliament BillsaadiОценок пока нет

- Trick GK File 3Документ6 страницTrick GK File 3aadiОценок пока нет

- Basic - Science - Questions - 99Документ22 страницыBasic - Science - Questions - 99aadiОценок пока нет

- Trick GK File 5 - (Geography Special) PDFДокумент6 страницTrick GK File 5 - (Geography Special) PDFaadiОценок пока нет

- Current Affairs July PDF Capsule 2015 by AffairsCloudДокумент137 страницCurrent Affairs July PDF Capsule 2015 by AffairsCloudgauravkakkar28Оценок пока нет

- Risk Assessment ProcessДокумент39 страницRisk Assessment ProcessaadiОценок пока нет

- Iso 27001Документ65 страницIso 27001aadiОценок пока нет

- A Study of The Business Value of It General Controls in ChinaДокумент15 страницA Study of The Business Value of It General Controls in ChinaPuguh JayadiningratОценок пока нет

- Get Vehicle Loans at Low RatesДокумент5 страницGet Vehicle Loans at Low RatesAkshay ZutshiОценок пока нет

- Richard W Ellson ResumeДокумент2 страницыRichard W Ellson Resumenrhuron13Оценок пока нет

- 4 Completing The Accounting Cycle PartДокумент1 страница4 Completing The Accounting Cycle PartTalionОценок пока нет

- All AcДокумент32 страницыAll AcVinod KumarОценок пока нет

- GST Payment Challan Form NEFT DetailsДокумент2 страницыGST Payment Challan Form NEFT DetailsSunil KalraОценок пока нет

- Ym0654 Tax - PNL 2019 04 01 2020 03 31Документ52 страницыYm0654 Tax - PNL 2019 04 01 2020 03 31Jayachandra JcОценок пока нет

- HDFCДокумент36 страницHDFCdarshan.babu.mclarenОценок пока нет

- APP ScenariosДокумент18 страницAPP Scenariosanand chawanОценок пока нет

- Paul Renner C6 - KYCmap - Preventing Financial Instrument FraudДокумент6 страницPaul Renner C6 - KYCmap - Preventing Financial Instrument FraudPaul RennerОценок пока нет

- Stakeholder Relationship ManagementДокумент7 страницStakeholder Relationship Managementchrisdi08Оценок пока нет

- CCR S.A. - August 12, 2021 Financial StatementsДокумент27 страницCCR S.A. - August 12, 2021 Financial StatementsTheodore H. CallisterОценок пока нет

- Finmar Quiz MidtermДокумент1 страницаFinmar Quiz MidtermNune SabanalОценок пока нет

- Syailendra Fixed Income FundДокумент1 страницаSyailendra Fixed Income FundJan KristantoОценок пока нет

- Final INTERNSHIP Report BCB FALL 2019 PDFДокумент52 страницыFinal INTERNSHIP Report BCB FALL 2019 PDFMuhammad TamimОценок пока нет

- N DivyaS RanjithKumarДокумент14 страницN DivyaS RanjithKumarPrithviОценок пока нет

- Standby Letter of CreditДокумент14 страницStandby Letter of CreditSudershan ThaibaОценок пока нет

- Bahan Kuis Prak Kompak Senin SiangДокумент3 страницыBahan Kuis Prak Kompak Senin SiangAkbaer EkoОценок пока нет

- Bank Reconmciliation ProcessДокумент13 страницBank Reconmciliation ProcessRachelleОценок пока нет

- MUTUAL FUNDS STUDYДокумент30 страницMUTUAL FUNDS STUDYBhavesh PopatОценок пока нет

- How interest rates impact bond pricesДокумент2 страницыHow interest rates impact bond pricestawhid anamОценок пока нет

- Revisi Group 11 - Completing The AuditДокумент22 страницыRevisi Group 11 - Completing The AuditEsti SetianingsihОценок пока нет

- UFRS CH-21-25 ProblemSetДокумент30 страницUFRS CH-21-25 ProblemSetGioОценок пока нет

- Assignment Module 3 LedgerДокумент3 страницыAssignment Module 3 LedgerPRINCE100% (1)

- Jo Jita Wahi SikanderДокумент31 страницаJo Jita Wahi SikanderRupali GuptaОценок пока нет

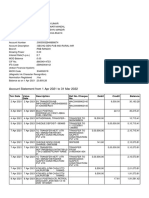

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент14 страницAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandОценок пока нет