Вам также может понравиться

- Research Methodology Full NotesДокумент87 страницResearch Methodology Full Notesu2b1151785% (253)

- Example Accounting ProblemsДокумент17 страницExample Accounting ProblemsMarryRose Dela Torre FerrancoОценок пока нет

- BF Activity-sheet-Q2 Week 3 and 4 Risk-Return-Trade-OffДокумент12 страницBF Activity-sheet-Q2 Week 3 and 4 Risk-Return-Trade-OffSamantha Beatriz B Chua100% (1)

- 1 Accounting For Merchandising BusinessДокумент23 страницы1 Accounting For Merchandising BusinessKhay2 ManaliliDelaCruz100% (1)

- Reflective Essay On Art AppreciationДокумент4 страницыReflective Essay On Art AppreciationKyeien50% (2)

- 201 1ST Ass With AnswersДокумент19 страниц201 1ST Ass With AnswersLyn AbudaОценок пока нет

- Module - 1: What Do You Already Know?Документ23 страницыModule - 1: What Do You Already Know?Lene Corpuz100% (1)

- Lesson 3 Statement of Changes in Equity (SCE)Документ11 страницLesson 3 Statement of Changes in Equity (SCE)Hazel Joy DalanonОценок пока нет

- SCALP Handout 044Документ10 страницSCALP Handout 044Angelica PatagОценок пока нет

- Chapter 5: Analysis Financial Statements: Financial Mix RatioДокумент22 страницыChapter 5: Analysis Financial Statements: Financial Mix RatioBOSS I4N TVОценок пока нет

- Research Project 0.1Документ23 страницыResearch Project 0.1Prince SanjiОценок пока нет

- Las-Business-Finance-Q1 Week 1Документ16 страницLas-Business-Finance-Q1 Week 1Kinn Jay100% (1)

- Case Study 2Документ6 страницCase Study 2Joshua Eric Velasco DandalОценок пока нет

- Sari-Tech: Mobile Based Inventory and Management SystemДокумент4 страницыSari-Tech: Mobile Based Inventory and Management SystemMendoza, Adrian M.Оценок пока нет

- Journal Entries TradingДокумент79 страницJournal Entries TradingAvox EverdeenОценок пока нет

- AccountantsДокумент15 страницAccountantsJenny EvangelistaОценок пока нет

- Salary WagesДокумент4 страницыSalary WagesAthena Panal DangelОценок пока нет

- Resuento - Ulob ActivitiesДокумент16 страницResuento - Ulob Activitiesemem resuentoОценок пока нет

- Forefront II Trading CorporationДокумент6 страницForefront II Trading CorporationJasmine LimОценок пока нет

- 4.3. Obligations of Borrowers: Questions To PonderДокумент6 страниц4.3. Obligations of Borrowers: Questions To PonderTin CabosОценок пока нет

- Introduction To Applied Economics 3Документ12 страницIntroduction To Applied Economics 3Rex Michael100% (1)

- Module II - Analyzing Business TransactionsДокумент4 страницыModule II - Analyzing Business TransactionsIj IlardeОценок пока нет

- Exercise 3-15Документ3 страницыExercise 3-15Roy Bonitez100% (2)

- Tiga Laba Laundry Shop General Journal For The Month of January 2020 Date Particulars P R Debit Credi TДокумент5 страницTiga Laba Laundry Shop General Journal For The Month of January 2020 Date Particulars P R Debit Credi TMaureen FloresОценок пока нет

- Chapter 2 and 3 Lopez BookДокумент4 страницыChapter 2 and 3 Lopez BookSam CorsigaОценок пока нет

- Module 8.2Документ28 страницModule 8.2Yen AllejeОценок пока нет

- Accounting Act 2Документ2 страницыAccounting Act 2Vanessa Bianca Glace Viray BanagОценок пока нет

- Foa p1 Module For Bsa & Bsais StudentsДокумент41 страницаFoa p1 Module For Bsa & Bsais StudentsMiquel VillamarinОценок пока нет

- Title: Marketing Practices of Street Food Vendors in Roxas Avenue, Davao CityДокумент25 страницTitle: Marketing Practices of Street Food Vendors in Roxas Avenue, Davao CityJhayann Ramirez100% (1)

- Strategic Management of Stakeholder RelationshipsДокумент18 страницStrategic Management of Stakeholder RelationshipsAlyssa Hallasgo-Lopez Atabelo100% (1)

- Guidelines On Basic Accounting Principles and ConceptsДокумент15 страницGuidelines On Basic Accounting Principles and ConceptsCrisMedionaОценок пока нет

- ApliedEconomics Q3 M5 Activity 2Документ1 страницаApliedEconomics Q3 M5 Activity 2Gine Bert Fariñas PalabricaОценок пока нет

- Module 1 - Lesson 1Документ6 страницModule 1 - Lesson 1Mai RuizОценок пока нет

- Business Finance: Basic Long-Term Financial ConceptsДокумент37 страницBusiness Finance: Basic Long-Term Financial ConceptsLala BubОценок пока нет

- Rovelyn E. Forcadas ABM-11 Activity #9-BДокумент2 страницыRovelyn E. Forcadas ABM-11 Activity #9-BRovelyn E. ForcadasОценок пока нет

- Fundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeДокумент9 страницFundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeBea allyssa CanapiОценок пока нет

- Fabm2 Q3 M2-3Документ10 страницFabm2 Q3 M2-3Jessamine Romano AplodОценок пока нет

- Business Ethics - Module 9Документ4 страницыBusiness Ethics - Module 9jhongmhai GamingОценок пока нет

- Financial AnalysisДокумент3 страницыFinancial AnalysisJasmine ActaОценок пока нет

- FAR Chapter4 FinalДокумент43 страницыFAR Chapter4 FinalPATRICIA COLINAОценок пока нет

- Quantitative Techniques ReviewerДокумент3 страницыQuantitative Techniques ReviewerAstronomy SpacefieldОценок пока нет

- Module 1 Introduction To Applied EconomicsДокумент6 страницModule 1 Introduction To Applied EconomicsLa salette roxasОценок пока нет

- Activity Module 1,2,3,4,5,6,7,8, and 9 FinalДокумент13 страницActivity Module 1,2,3,4,5,6,7,8, and 9 FinalQuenie De la CruzОценок пока нет

- Financial Statements Analyses and Their Implications To ManagementДокумент9 страницFinancial Statements Analyses and Their Implications To ManagementMarie Frances SaysonОценок пока нет

- Chapter 2 4Документ16 страницChapter 2 4Jasmine TalagtagОценок пока нет

- 01 Activity 1-WPS OfficeДокумент2 страницы01 Activity 1-WPS OfficeDaphne RoblesОценок пока нет

- PT .1 in AccountingДокумент8 страницPT .1 in AccountingMerdwindelle Allagones100% (1)

- Business Ethics and Social Responsibilities - Module 1Документ11 страницBusiness Ethics and Social Responsibilities - Module 1Ayessa mae CaagoyОценок пока нет

- Fabm1 Completing The Accounting CycleДокумент16 страницFabm1 Completing The Accounting CycleVenice100% (1)

- Fundamental of Accounting, Business, and Management 2 PDFДокумент15 страницFundamental of Accounting, Business, and Management 2 PDFElijah AramburoОценок пока нет

- FABM Case StudyДокумент11 страницFABM Case StudyAlyssa FarnazoОценок пока нет

- Filipino Values System in BusinessДокумент19 страницFilipino Values System in BusinessCristine FerrerОценок пока нет

- Final ModuleДокумент3 страницыFinal ModuleAnnabelle MancoОценок пока нет

- Position PaperДокумент2 страницыPosition PaperGeojanni Pangibitan100% (1)

- Financial Statement ExamДокумент2 страницыFinancial Statement ExamTam TamОценок пока нет

- Production Schedule For Output X With Variable Labor Input Quantity of Labor Input Total Product Marginal Product Average ProductДокумент2 страницыProduction Schedule For Output X With Variable Labor Input Quantity of Labor Input Total Product Marginal Product Average ProductPrincess GallionОценок пока нет

- CHAPTER 2 (2) PaynalДокумент11 страницCHAPTER 2 (2) PaynalKristine Joy LarderaОценок пока нет

- Business Mathematics - Module 14 - Overtime PayДокумент6 страницBusiness Mathematics - Module 14 - Overtime PayLovely Joy Hatamosa Verdon-DielОценок пока нет

- Pamantasan NG Lungsod NG Pasig: Test I - IdentificationДокумент2 страницыPamantasan NG Lungsod NG Pasig: Test I - IdentificationKyree VladeОценок пока нет

- Q-1. What Is The Difference Between Management Accounting and Financial Accounting?Документ12 страницQ-1. What Is The Difference Between Management Accounting and Financial Accounting?poojaОценок пока нет

- SomethingДокумент6 страницSomethingGanya BishnoiОценок пока нет

- Abm 1 Lesson Week 6Документ17 страницAbm 1 Lesson Week 6Teacher Roschelle mariñasОценок пока нет

- Objective of The StudyДокумент3 страницыObjective of The StudyKyeienОценок пока нет

- Parental Consent FormДокумент1 страницаParental Consent FormKyeienОценок пока нет

- Philippine Culture: What Makes The Filipinos Different From The Rest of The WorldДокумент10 страницPhilippine Culture: What Makes The Filipinos Different From The Rest of The WorldKyeienОценок пока нет

- Solicitation LetterДокумент3 страницыSolicitation LetterKyeienОценок пока нет

- ArtsДокумент1 страницаArtsKyeienОценок пока нет

- Ratio Analysis-WPS OfficeДокумент4 страницыRatio Analysis-WPS OfficeKyeienОценок пока нет

- Chapter 3 Key Points On Process CostingДокумент4 страницыChapter 3 Key Points On Process CostingKyeienОценок пока нет

- Stories With Values For KidsДокумент19 страницStories With Values For KidsKyeienОценок пока нет

- Art Is An Objec-WPS OfficeДокумент3 страницыArt Is An Objec-WPS OfficeKyeienОценок пока нет

- Process FIFO CostingДокумент6 страницProcess FIFO CostingKyeienОценок пока нет

- Key Points On Slam PoetryДокумент1 страницаKey Points On Slam PoetryKyeienОценок пока нет

- The Proud Rose, Some StoriesДокумент3 страницыThe Proud Rose, Some StoriesKyeienОценок пока нет

- The 10 Best Short Stories EverДокумент6 страницThe 10 Best Short Stories EverKyeienОценок пока нет

- Chapter V-Ix CooperativeДокумент17 страницChapter V-Ix CooperativeKyeienОценок пока нет

- What Does A Billionaire Mind EntailsДокумент2 страницыWhat Does A Billionaire Mind EntailsAyesha ButtОценок пока нет

- BP For Sap S4hana Otc PDFДокумент39 страницBP For Sap S4hana Otc PDFUzair AslamОценок пока нет

- Lecture - 11 Brand Equity - Models and TheoriesДокумент13 страницLecture - 11 Brand Equity - Models and TheoriesAbdullah JavedОценок пока нет

- I. POS System of StarbucksДокумент8 страницI. POS System of StarbucksKyra Mae Asis TreceñeОценок пока нет

- List of Top UAE CompaniesДокумент8 страницList of Top UAE CompaniesTauheedalHasan58% (19)

- Technopreneurship Module 5: Customer Segment Activity 5: Frianeza, Zarah Joy C. BCSE-3-2Документ2 страницыTechnopreneurship Module 5: Customer Segment Activity 5: Frianeza, Zarah Joy C. BCSE-3-2Joy Frianeza75% (4)

- Curriculum - Vitae - Format Juliette PDFДокумент3 страницыCurriculum - Vitae - Format Juliette PDFJuli JulioОценок пока нет

- Chapter 10 PPT - Holthausen & Zmijewski 2019Документ121 страницаChapter 10 PPT - Holthausen & Zmijewski 2019royОценок пока нет

- BAN120 Journal ReviewДокумент1 страницаBAN120 Journal ReviewEdwin CastilloОценок пока нет

- Chapter 1Документ27 страницChapter 1Haqim HazramieОценок пока нет

- Sample of Article Review PDFДокумент9 страницSample of Article Review PDFEleanor50% (2)

- Bingcang & Tamon (CVP, Module 5)Документ67 страницBingcang & Tamon (CVP, Module 5)FayehAmantilloBingcangОценок пока нет

- Pert.5 Activity-Based Costing and ManagementДокумент44 страницыPert.5 Activity-Based Costing and ManagementHanis AryОценок пока нет

- Caed102: Financial MarketsДокумент2 страницыCaed102: Financial MarketsXytusОценок пока нет

- Chapter 17 Limits To The Use of DebtДокумент25 страницChapter 17 Limits To The Use of DebtFahmi Ahmad FarizanОценок пока нет

- Ninjacart - Indian Company - Company ProfileДокумент23 страницыNinjacart - Indian Company - Company ProfileebeОценок пока нет

- Lecture-03 Organization of Maintenance ForceДокумент34 страницыLecture-03 Organization of Maintenance ForceMohammad ShafiОценок пока нет

- Cross-Functional CompetenciesДокумент2 страницыCross-Functional Competenciesasdkhn khnОценок пока нет

- Tutorial Sheet 2Документ2 страницыTutorial Sheet 2siamesamuel229Оценок пока нет

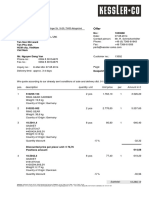

- Angebot 1033668 PDFДокумент2 страницыAngebot 1033668 PDFhoiОценок пока нет

- 070 Blessy JosephДокумент28 страниц070 Blessy JosephClaira BanikОценок пока нет

- إعادة هيكلة الشركاتДокумент15 страницإعادة هيكلة الشركات111bfdfdОценок пока нет

- ACW 367 WK 5 Conceptual Framework ModifiedДокумент18 страницACW 367 WK 5 Conceptual Framework ModifiedKameleswary GanesanОценок пока нет

- ECON 1000 Exam Review Q62-75Документ3 страницыECON 1000 Exam Review Q62-75Slock TruОценок пока нет

- Order #37677567: Item Info Order SummaryДокумент1 страницаOrder #37677567: Item Info Order Summaryagrace burgosОценок пока нет

- Entrepreneur Ship Development: Deepa Kumari Deepa - Kumari@sharda - Ac.inДокумент25 страницEntrepreneur Ship Development: Deepa Kumari Deepa - Kumari@sharda - Ac.inREHANRAJОценок пока нет

- Yustika Adiningsih-f0319141-Spm A-Mindmap CH 4 Dan 5Документ2 страницыYustika Adiningsih-f0319141-Spm A-Mindmap CH 4 Dan 5yes iОценок пока нет

- Freight Calculation - FCL - SolutionДокумент4 страницыFreight Calculation - FCL - SolutionTanisha AgarwalОценок пока нет