Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Updates in PFRS Answer SheetsДокумент11 страницUpdates in PFRS Answer SheetsVrix Ace MangilitОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Strategic Cost Management - Answer SheetsДокумент12 страницStrategic Cost Management - Answer SheetsVrix Ace MangilitОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- FAR Answer SheetsДокумент10 страницFAR Answer SheetsVrix Ace MangilitОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- 1906 January 2018 ENCS FinalДокумент2 страницы1906 January 2018 ENCS FinalJewelyn C. Espares-Ciocon100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Cost Behavior AnaysisДокумент19 страницCost Behavior AnaysisVrix Ace MangilitОценок пока нет

- Application for Authority to Print Receipts and InvoicesДокумент1 страницаApplication for Authority to Print Receipts and InvoicesVrix Ace MangilitОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Cash and ReceivablesДокумент30 страницCash and ReceivablesVrix Ace MangilitОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Afar Answer SheetДокумент7 страницAfar Answer SheetVrix Ace MangilitОценок пока нет

- Cost Behavior and Segregation: TopicДокумент4 страницыCost Behavior and Segregation: TopicVrix Ace MangilitОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- Test Bank With Answers Intermediate Accounting 12e by Kieso Chapter 17Документ47 страницTest Bank With Answers Intermediate Accounting 12e by Kieso Chapter 17Cleofe Jane PatnubayОценок пока нет

- Working Capital & Cash Management: Collecting Center Concentration BankingДокумент3 страницыWorking Capital & Cash Management: Collecting Center Concentration BankingVrix Ace MangilitОценок пока нет

- Humanbe Case Study 1Документ1 страницаHumanbe Case Study 1Vrix Ace MangilitОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Application for Authority to Print Receipts and InvoicesДокумент1 страницаApplication for Authority to Print Receipts and InvoicesVrix Ace MangilitОценок пока нет

- Application For Business Permit: Amendment: AmendmentДокумент2 страницыApplication For Business Permit: Amendment: AmendmentVrix Ace MangilitОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- CLASSIQUE Furniture Co.: Quantity Unit Article Unit PriceДокумент2 страницыCLASSIQUE Furniture Co.: Quantity Unit Article Unit PriceVrix Ace MangilitОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- In Settlement of The Following: Amount: Total Sales Less: SC/PWD Discount Total Due Less: Withholding Tax Payment DueДокумент2 страницыIn Settlement of The Following: Amount: Total Sales Less: SC/PWD Discount Total Due Less: Withholding Tax Payment DueVrix Ace MangilitОценок пока нет

- Account Titles and Descriptions for Financial StatementsДокумент13 страницAccount Titles and Descriptions for Financial StatementsVrix Ace MangilitОценок пока нет

- BUSINESS-PERMIT-FORM (Dragged)Документ1 страницаBUSINESS-PERMIT-FORM (Dragged)Vrix Ace MangilitОценок пока нет

- Application For Business Permit: Amendment: AmendmentДокумент2 страницыApplication For Business Permit: Amendment: AmendmentVrix Ace MangilitОценок пока нет

- Statement of CI and OEДокумент5 страницStatement of CI and OEVrix Ace MangilitОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Type Type of Books To Be Registered Quantity From ToДокумент1 страницаType Type of Books To Be Registered Quantity From ToVrix Ace MangilitОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- CLASSIQUE Furniture Co. Trial Balance 2019Документ1 страницаCLASSIQUE Furniture Co. Trial Balance 2019Vrix Ace MangilitОценок пока нет

- Managerial and SupervisoryДокумент2 страницыManagerial and SupervisoryVrix Ace MangilitОценок пока нет

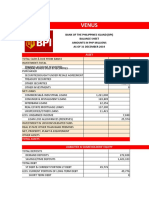

- Statement of Financial Position As of March 31, 2020Документ5 страницStatement of Financial Position As of March 31, 2020Vrix Ace MangilitОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- BIR Registration FormДокумент4 страницыBIR Registration FormVrix Ace MangilitОценок пока нет

- Finmar ReqsДокумент2 страницыFinmar ReqsVrix Ace MangilitОценок пока нет

- Statement of Financial Position As of December 31, 2020Документ4 страницыStatement of Financial Position As of December 31, 2020Vrix Ace MangilitОценок пока нет

- FINMARKДокумент4 страницыFINMARKVrix Ace MangilitОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Book 1Документ1 страницаBook 1Vrix Ace MangilitОценок пока нет

- FOREXДокумент2 страницыFOREXVrix Ace MangilitОценок пока нет

- Auditing bank reconciliation proceduresДокумент2 страницыAuditing bank reconciliation procedureshsjhsОценок пока нет

- Rotisserie Affair Deli Marketing PlanДокумент41 страницаRotisserie Affair Deli Marketing PlanAri EngberОценок пока нет

- Concord Final Edition For GBSДокумент35 страницConcord Final Edition For GBSMahamud Zaman ShumitОценок пока нет

- Adrian MittermayrДокумент2 страницыAdrian Mittermayrapi-258981850Оценок пока нет

- Group 6 - Mid-Term - PNJ PosterДокумент1 страницаGroup 6 - Mid-Term - PNJ PosterMai SươngОценок пока нет

- Microeconomics Principles and Policy 13Th Edition Baumol Test Bank Full Chapter PDFДокумент67 страницMicroeconomics Principles and Policy 13Th Edition Baumol Test Bank Full Chapter PDFVeronicaKellykcqb100% (8)

- Travel Procedure Module #3Документ9 страницTravel Procedure Module #3Salvatore VieiraОценок пока нет

- CRM AssignmentДокумент3 страницыCRM AssignmentDiksha VashishthОценок пока нет

- Malaysia's Petrochemical Zones For Location PDFДокумент41 страницаMalaysia's Petrochemical Zones For Location PDFWan Faiz50% (2)

- Integration and Responsiveness MatrixДокумент9 страницIntegration and Responsiveness MatrixVishalОценок пока нет

- The Product Manager and The ProductДокумент24 страницыThe Product Manager and The ProductRohitkumariluОценок пока нет

- DTC Agreement Between Cyprus and United StatesДокумент30 страницDTC Agreement Between Cyprus and United StatesOECD: Organisation for Economic Co-operation and DevelopmentОценок пока нет

- LA Chief Procurement OfficerДокумент3 страницыLA Chief Procurement OfficerJason ShuehОценок пока нет

- Savings BondsДокумент2 страницыSavings BondsffsdfsfdftrertОценок пока нет

- SM MCQДокумент30 страницSM MCQWoroud Quraan100% (3)

- Chap 001Документ6 страницChap 001Vicky CamiОценок пока нет

- All about Shezan's marketing strategyДокумент2 страницыAll about Shezan's marketing strategySam HeartsОценок пока нет

- Astro and CosmoДокумент5 страницAstro and CosmoGerson SchafferОценок пока нет

- Consumer Satisfaction of Aircel NetworkДокумент5 страницConsumer Satisfaction of Aircel NetworkSaurabh KumarОценок пока нет

- ARISE Spa Struggles to Keep Employees SatisfiedДокумент21 страницаARISE Spa Struggles to Keep Employees Satisfiedarjunparekh100% (6)

- Tiong, Gilbert Charles - Financial Planning and ManagementДокумент10 страницTiong, Gilbert Charles - Financial Planning and ManagementGilbert TiongОценок пока нет

- CH 11Документ6 страницCH 11Saleh RaoufОценок пока нет

- Chapter 5 Questions V1Документ6 страницChapter 5 Questions V1prashantgargindia_930% (1)

- Unincorporated Business TrustДокумент9 страницUnincorporated Business TrustSpencerRyanOneal98% (42)

- Coso ErmДокумент49 страницCoso ErmmullazakОценок пока нет

- Bukit Asam Anual ReportДокумент426 страницBukit Asam Anual Reportwandi_borneo8753Оценок пока нет

- Beams 12ge LN22Документ51 страницаBeams 12ge LN22emakОценок пока нет

- Finance Class 04 - New With TestДокумент23 страницыFinance Class 04 - New With TestMM Fakhrul IslamОценок пока нет

- Abdulghany Mohamed CVДокумент4 страницыAbdulghany Mohamed CVAbdulghany SulehriaОценок пока нет

- SBR Res QcaДокумент3 страницыSBR Res QcaAlejandro ZagalОценок пока нет