Вам также может понравиться

- Value Chain Management Capability A Complete Guide - 2020 EditionОт EverandValue Chain Management Capability A Complete Guide - 2020 EditionОценок пока нет

- Process DesignДокумент28 страницProcess DesignAnna DolotОценок пока нет

- Ps Module 4 Understanding Buyers Week 7-8Документ35 страницPs Module 4 Understanding Buyers Week 7-8Marian Rivera DiazОценок пока нет

- Management Accounting: Student EditionДокумент27 страницManagement Accounting: Student EditiondianaОценок пока нет

- Management Accounting: Product & Service CostingДокумент49 страницManagement Accounting: Product & Service CostingFarizal WahyuОценок пока нет

- SPG Sample BallotsДокумент5 страницSPG Sample BallotsVanessa Valerie RogadorОценок пока нет

- Ias 2Документ23 страницыIas 2Syed Salman Sajid100% (4)

- Advance Chapter 1Документ16 страницAdvance Chapter 1abel habtamuОценок пока нет

- Barringer 04Документ34 страницыBarringer 04ruth_erlynОценок пока нет

- PartnershipsДокумент27 страницPartnershipssamuel debebeОценок пока нет

- All Intermediate ChapterДокумент278 страницAll Intermediate ChapterNigus AyeleОценок пока нет

- Practice of Ratio Analysis Development of Financial StatementsДокумент8 страницPractice of Ratio Analysis Development of Financial StatementsZarish AzharОценок пока нет

- W4 Module 4 FINANCIAL RATIOS Part 2BДокумент12 страницW4 Module 4 FINANCIAL RATIOS Part 2BDanica VetuzОценок пока нет

- Week 1 Conceptual Framework For Financial ReportingДокумент17 страницWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARROОценок пока нет

- AFA2e Chapter03 PPTДокумент50 страницAFA2e Chapter03 PPTIzzy BОценок пока нет

- Financial ManagementДокумент96 страницFinancial ManagementAngelaMariePeñarandaОценок пока нет

- Statement of Cash Flows: Learning ObjectivesДокумент49 страницStatement of Cash Flows: Learning ObjectivesPrima Rosita AriniОценок пока нет

- CH 12 Intangible AssetsДокумент57 страницCH 12 Intangible AssetsSamiHadadОценок пока нет

- Chap 017 AccДокумент47 страницChap 017 Acckaren_park1Оценок пока нет

- M1 - Introduction To Valuation HandoutДокумент6 страницM1 - Introduction To Valuation HandoutPrince LeeОценок пока нет

- Brigham Powerpoint ch01Документ17 страницBrigham Powerpoint ch01AhsanОценок пока нет

- Capital Budget Planning PowerPointfinalДокумент31 страницаCapital Budget Planning PowerPointfinalNour FawazОценок пока нет

- Income and Changes in Retained Earnings: - Chapter 12Документ49 страницIncome and Changes in Retained Earnings: - Chapter 12Moqadus SeharОценок пока нет

- 2 Overview of Transaction Processing and ERP SystemДокумент25 страниц2 Overview of Transaction Processing and ERP SystemLisna SetiawatiОценок пока нет

- Corporation and Corporate GovernanceДокумент18 страницCorporation and Corporate GovernanceAlmiraОценок пока нет

- ch04.ppt - Income Statement and Related InformationДокумент68 страницch04.ppt - Income Statement and Related InformationAmir ContrerasОценок пока нет

- Chapter 7 Asset Investment Decisions and Capital RationingДокумент31 страницаChapter 7 Asset Investment Decisions and Capital RationingdperepolkinОценок пока нет

- Total Quality Management: Three Case Studies From Around The WorldДокумент5 страницTotal Quality Management: Three Case Studies From Around The WorldhariОценок пока нет

- Sallys Struthers - Answer KeyДокумент7 страницSallys Struthers - Answer KeyLlyod Francis LaylayОценок пока нет

- Chapter 2 (The Asset Allocation Decision)Документ28 страницChapter 2 (The Asset Allocation Decision)Abuzafar AbdullahОценок пока нет

- CH 14Документ63 страницыCH 14Sahar YehiaОценок пока нет

- Chapter 4 - Managing in A Global EnvironmentДокумент5 страницChapter 4 - Managing in A Global Environmentbiancag_91Оценок пока нет

- 3 Multinational EnterpriseДокумент33 страницы3 Multinational Enterprisemahbobullah rahmaniОценок пока нет

- Lecture 10 - Financial Statement AnalysisДокумент35 страницLecture 10 - Financial Statement AnalysisTabassum Sufia MazidОценок пока нет

- Amoud Universit Y: Facult of Economics and Pol ScienceДокумент5 страницAmoud Universit Y: Facult of Economics and Pol ScienceCabdirizaq McismaanОценок пока нет

- Hansen AISE IM Ch07Документ54 страницыHansen AISE IM Ch07AimanОценок пока нет

- Financial Accounting 4th Edition Chapter 2Документ67 страницFinancial Accounting 4th Edition Chapter 2Joey TrompОценок пока нет

- Chapter 5 The Production Process and CostsДокумент6 страницChapter 5 The Production Process and CostsChristlyn Joy BaralОценок пока нет

- Chapter 2Документ48 страницChapter 2Mohd AsyrafОценок пока нет

- Titman PPT CH18Документ79 страницTitman PPT CH18IKA RAHMAWATIОценок пока нет

- Hello PDFДокумент57 страницHello PDFMursalin HossainОценок пока нет

- Ethics, Fraud and Internal Control: Accounting Information Systems 9e James A. HallДокумент41 страницаEthics, Fraud and Internal Control: Accounting Information Systems 9e James A. HallAdilah AzamОценок пока нет

- Module 2Документ13 страницModule 2Mimi OlshopeОценок пока нет

- M Fin 202 CH 13 SolutionsДокумент9 страницM Fin 202 CH 13 SolutionsNguyenThiTuOanhОценок пока нет

- Chapter 1 AccountingДокумент64 страницыChapter 1 AccountingMasum HossainОценок пока нет

- 12 Channel Power, Conflict & Its ManagingДокумент38 страниц12 Channel Power, Conflict & Its ManagingSagar Bhardwaj100% (1)

- Portfolio ManagementДокумент28 страницPortfolio Managementagarwala4767% (3)

- Long-Term FinancingДокумент30 страницLong-Term Financingmarkwillbalbas100% (1)

- AFM Lecture 11Документ24 страницыAFM Lecture 11Alseraj TechnologyОценок пока нет

- Chapter 1 5e With AnswersДокумент16 страницChapter 1 5e With AnswersDiana Aeleen Mandujano Poblano100% (2)

- Gtu Theory QuestionsДокумент4 страницыGtu Theory QuestionsbhfunОценок пока нет

- Managerial Econimics AssignmentДокумент3 страницыManagerial Econimics AssignmentNikhilОценок пока нет

- Name: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateДокумент8 страницName: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateRegina PutriОценок пока нет

- Customer Satisfaction Level at Wal-MartДокумент17 страницCustomer Satisfaction Level at Wal-MartShagun NagpalОценок пока нет

- Capital Structure PlanningДокумент25 страницCapital Structure PlanningSumit MahajanОценок пока нет

- The Four Walls: Live Like the Wind, Free, Without HindrancesОт EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesРейтинг: 5 из 5 звезд5/5 (1)

- Management Accounting: Activity Cost BehaviorДокумент44 страницыManagement Accounting: Activity Cost BehaviorCharlet_DОценок пока нет

- Hansen Aise Im Ch03Документ44 страницыHansen Aise Im Ch03Milun RahmaОценок пока нет

- Graduate Thesis Topics in EconomicsДокумент6 страницGraduate Thesis Topics in Economicslizbundrenwestminster100% (2)

- Motor's Bearing DetailsДокумент9 страницMotor's Bearing DetailsValipireddy NagarjunОценок пока нет

- How To Acquit Your Funding FinalДокумент5 страницHow To Acquit Your Funding FinalIsmael SamsonОценок пока нет

- BPCL Indemnity BondДокумент2 страницыBPCL Indemnity Bondmilind kenjaleОценок пока нет

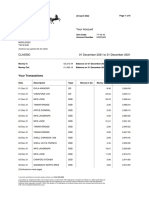

- Vessel 2023 09 07Документ3 страницыVessel 2023 09 07bill duanОценок пока нет

- Eco ProjectДокумент2 страницыEco ProjectOm ChandakОценок пока нет

- Me6004 UcmpДокумент93 страницыMe6004 UcmpRam100% (1)

- GO - Ms.No. 259Документ2 страницыGO - Ms.No. 259Anonymous 9Yv6n5qvSОценок пока нет

- Indian Oil Corporation Limited: Bhubaneswar Divisional OfficeДокумент3 страницыIndian Oil Corporation Limited: Bhubaneswar Divisional OfficeBinay Sahoo100% (1)

- General Ledger & Trial BalanceДокумент5 страницGeneral Ledger & Trial BalancecassaaaeyОценок пока нет

- Lesson 9: Benefit/Cost Analysis and Public Sector Economics: Prof - Jessica Maria Paz S. Casimiro, Ce, Enp, DisdsДокумент26 страницLesson 9: Benefit/Cost Analysis and Public Sector Economics: Prof - Jessica Maria Paz S. Casimiro, Ce, Enp, DisdsAziezah PalintaОценок пока нет

- Topic 8 AsphaltДокумент20 страницTopic 8 Asphaltvirkaalam02Оценок пока нет

- Homework Chap 25Документ2 страницыHomework Chap 25An leeОценок пока нет

- 2016 Preqin Global Private Equity & Venture Capital: Sample PagesДокумент15 страниц2016 Preqin Global Private Equity & Venture Capital: Sample PagesJZОценок пока нет

- LNGC Methane Princess - Imo 9253715 - Cargo-Operating-ManualДокумент245 страницLNGC Methane Princess - Imo 9253715 - Cargo-Operating-Manualseawolf50Оценок пока нет

- Your AccountДокумент6 страницYour AccountJean FurtadoОценок пока нет

- Pluger Pump 310 N Cat PumpsДокумент4 страницыPluger Pump 310 N Cat PumpsJorge EstebanОценок пока нет

- GR8 Ems Nov Test P1 2022Документ12 страницGR8 Ems Nov Test P1 2022melisizwenzimande32Оценок пока нет

- Total Qty - 4 Nos Material - UNS F33100 / ASTM A536 65-45-12Документ1 страницаTotal Qty - 4 Nos Material - UNS F33100 / ASTM A536 65-45-12sudipta dasОценок пока нет

- Brilliant Negotiations What Brilliant Negotiators Know, Do and SayДокумент153 страницыBrilliant Negotiations What Brilliant Negotiators Know, Do and SayThomas FederuikОценок пока нет

- QS Seamless Aluminum Ferrules Safe Use and Instructions V01Документ6 страницQS Seamless Aluminum Ferrules Safe Use and Instructions V01beshoyОценок пока нет

- Lot Plan-1Документ1 страницаLot Plan-1johnpaul mosuelaОценок пока нет

- FinmanДокумент9 страницFinmanCharles MateoОценок пока нет

- Channel FUSДокумент1 страницаChannel FUSArunKumar RajendranОценок пока нет

- Management Programme Term-End Examination 00 December, 2011 Ms-8: Quantitative Analysis ForДокумент4 страницыManagement Programme Term-End Examination 00 December, 2011 Ms-8: Quantitative Analysis Forvaaz205Оценок пока нет

- Elasticity of DemandДокумент64 страницыElasticity of DemandWadOod KhAn100% (1)

- Microeconomics 4Th Edition Krugman Test Bank Full Chapter PDFДокумент67 страницMicroeconomics 4Th Edition Krugman Test Bank Full Chapter PDFletitiajasminednyaa100% (10)

- Assorted Steel Bars and Metal Sheets: Deformed Reinforcing Steel BarДокумент2 страницыAssorted Steel Bars and Metal Sheets: Deformed Reinforcing Steel BarVon San JoseОценок пока нет

- MACD - Trading The MACD DivergenceДокумент7 страницMACD - Trading The MACD DivergenceAaron DrakeОценок пока нет

- Field Performance of BlueCoil Including Performance of Mechanically Damaged CTДокумент15 страницField Performance of BlueCoil Including Performance of Mechanically Damaged CTbehrooz rajabshehniОценок пока нет