Вам также может понравиться

- 1 SEM BCOM - Indian Financial System PDFДокумент35 страниц1 SEM BCOM - Indian Financial System PDFLohithashva Nanjesh Gowda100% (5)

- Finale StocksДокумент108 страницFinale StocksNavin Jethmalani100% (2)

- HeatRatesSparkSpreadTolling Dec2010Документ5 страницHeatRatesSparkSpreadTolling Dec2010Deepanshu Agarwal100% (1)

- CB Lecture 4Документ17 страницCB Lecture 4Tshepang MatebesiОценок пока нет

- Gds Briefs LD Mar Apr Cards 20180214135237Документ135 страницGds Briefs LD Mar Apr Cards 20180214135237Anonymous UserОценок пока нет

- Interest Rates 1: What Are Interest Rates?: SSRN Electronic Journal January 2014Документ26 страницInterest Rates 1: What Are Interest Rates?: SSRN Electronic Journal January 2014Aina AguirreОценок пока нет

- The Nature and Role of Financial SystemДокумент58 страницThe Nature and Role of Financial SystemMadhu BabuОценок пока нет

- Financial Markets: From Wikipedia, The Free EncyclopediaДокумент24 страницыFinancial Markets: From Wikipedia, The Free Encyclopediaraden chandrajaya listiandokoОценок пока нет

- Financial SystemДокумент16 страницFinancial Systemshivakumar N100% (2)

- Mutual FundДокумент43 страницыMutual FundSachi LunechiyaОценок пока нет

- Financial Tools: Your Company NameДокумент33 страницыFinancial Tools: Your Company NameMarwan AbuzayanОценок пока нет

- RSM230 Tutorial January28Документ13 страницRSM230 Tutorial January28Sophia VuОценок пока нет

- Securitisation Primer and Analysis of A Financial Technique: Andrea Durante November 2010Документ25 страницSecuritisation Primer and Analysis of A Financial Technique: Andrea Durante November 2010Emmanuele Orospies SpadaroОценок пока нет

- Money Creation-Reflections of An Ex-Central BankerДокумент31 страницаMoney Creation-Reflections of An Ex-Central BankerbiondimiОценок пока нет

- An Overview: Treasury Operations in BanksДокумент61 страницаAn Overview: Treasury Operations in BanksManipal SinghОценок пока нет

- Indian Financial System: UNIT-1Документ48 страницIndian Financial System: UNIT-1Use ThrowОценок пока нет

- Prudent Daily Return Reports (19th Nov 2019)Документ74 страницыPrudent Daily Return Reports (19th Nov 2019)parveen kumarОценок пока нет

- Asset Securitisation and Long Term Financing in The Power SectorДокумент63 страницыAsset Securitisation and Long Term Financing in The Power SectorState House NigeriaОценок пока нет

- Overview of Mutual FundsДокумент29 страницOverview of Mutual FundsAkansh NuwalОценок пока нет

- Bfs1 Indian Financial SystemДокумент35 страницBfs1 Indian Financial SystemRitesh RamanОценок пока нет

- Indian Financial System: PGDM 4 TrimesterДокумент15 страницIndian Financial System: PGDM 4 TrimesterAshok PaikraОценок пока нет

- SBI Life ULIP News Letter January 2022Документ39 страницSBI Life ULIP News Letter January 2022Srigandh's WealthОценок пока нет

- Indian Financial SystemДокумент41 страницаIndian Financial SystemKaneОценок пока нет

- Part-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesДокумент7 страницPart-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesThe JesterОценок пока нет

- Asset-Backed Securitization, Kennard, Alan LДокумент10 страницAsset-Backed Securitization, Kennard, Alan Lsalah hamoudaОценок пока нет

- Financial Systems Financial Regulators and InstrumentsДокумент12 страницFinancial Systems Financial Regulators and InstrumentsRaymond Pascual100% (1)

- 2019 Revision Notes 8 - Chapter 8 6Документ9 страниц2019 Revision Notes 8 - Chapter 8 6Sarah RetzОценок пока нет

- Task-1 Good Investment Decision Make Investor Earn More Profits Explain. Meaning of InvestmentДокумент12 страницTask-1 Good Investment Decision Make Investor Earn More Profits Explain. Meaning of InvestmentthakuranitaОценок пока нет

- IFC Structured Finance EngДокумент2 страницыIFC Structured Finance EngJoe GentileОценок пока нет

- SBI Life ULIP News Letter April 2023Документ34 страницыSBI Life ULIP News Letter April 2023Kritika ThakurОценок пока нет

- Types of Mutual FundsДокумент5 страницTypes of Mutual FundsRajdeep BanerjeeОценок пока нет

- Finance Is A Bridge Between The Present & The FutureДокумент10 страницFinance Is A Bridge Between The Present & The FutureanuradhaОценок пока нет

- LeveragedFinanceHandbook PDFДокумент140 страницLeveragedFinanceHandbook PDFDarioОценок пока нет

- Foreign Exchange, Treasury and Market Risk Mangement-1Документ163 страницыForeign Exchange, Treasury and Market Risk Mangement-1Sandeep KumarОценок пока нет

- KCV49 PJYC4 M0 DJ PJ 827Документ26 страницKCV49 PJYC4 M0 DJ PJ 827GybcОценок пока нет

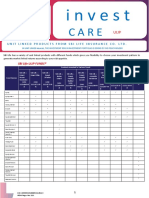

- Inves CareДокумент41 страницаInves CareSAM BОценок пока нет

- Financial System: Made by Akansha Richa SaxenaДокумент16 страницFinancial System: Made by Akansha Richa SaxenaAkansha SinghОценок пока нет

- Understanding The Risk of CDOsДокумент29 страницUnderstanding The Risk of CDOsngoodacre1Оценок пока нет

- FI02 Intro To Fixed Income Trading and Bonds 6523d55268da1Документ78 страницFI02 Intro To Fixed Income Trading and Bonds 6523d55268da1Kinzimbu Asset ManagementОценок пока нет

- The Sasub IДокумент24 страницыThe Sasub IHarsh KaushikОценок пока нет

- Accounting For Financial Instruments: AS-30, AS-31, AS-32Документ36 страницAccounting For Financial Instruments: AS-30, AS-31, AS-32ratikarumitОценок пока нет

- 1 SEM BCOM - Indian Financial System PDFДокумент35 страниц1 SEM BCOM - Indian Financial System PDFShambhavi JОценок пока нет

- 1 SEM BCOM - Indian Financial SystemДокумент35 страниц1 SEM BCOM - Indian Financial SystemShambhavi JОценок пока нет

- Securities Market: Dr. Rana Singh 9811828987Документ52 страницыSecurities Market: Dr. Rana Singh 9811828987Abebe AdmasuОценок пока нет

- Stock Investing Mastermind - Zebra Learn-86Документ2 страницыStock Investing Mastermind - Zebra Learn-86RGNitinDevaОценок пока нет

- ECO531 Chapter 2 Mind MapДокумент6 страницECO531 Chapter 2 Mind MapASMA HANANI BINTI ANUAR100% (1)

- Debt Securities Security Type Bonds, Notes and SecuritiesДокумент10 страницDebt Securities Security Type Bonds, Notes and Securitiessnehal kokareОценок пока нет

- Business Finance 1 NotesДокумент62 страницыBusiness Finance 1 Notessanu sayedОценок пока нет

- RE Capital Markets 6.9 330pДокумент82 страницыRE Capital Markets 6.9 330pAirollОценок пока нет

- IE - 2016 - Intro To Investment FundsДокумент30 страницIE - 2016 - Intro To Investment Fundsjhonatan velandia medinaОценок пока нет

- AC 3 - Intermediate Acctg' 1 (Ate Jan Ver)Документ119 страницAC 3 - Intermediate Acctg' 1 (Ate Jan Ver)John Renier Bernardo100% (1)

- Financial Education Workbook-IX - RemovedДокумент46 страницFinancial Education Workbook-IX - RemovedDaksh ChapadiyaОценок пока нет

- Indian Financial SystemДокумент35 страницIndian Financial SystemPrathviraj MajkureОценок пока нет

- CSB Bank Limited: 1.1 Brief History of The CompanyДокумент8 страницCSB Bank Limited: 1.1 Brief History of The CompanyNithin Mathew Jose MBA 2020Оценок пока нет

- Credit Agricole Covered BondsДокумент39 страницCredit Agricole Covered BondsBhulesh SinghОценок пока нет

- Capco Capital Mkt.v2Документ62 страницыCapco Capital Mkt.v2poonam cОценок пока нет

- Fixed Income Portfolio Management: Presented By: Group VДокумент29 страницFixed Income Portfolio Management: Presented By: Group VCarmela CastilloОценок пока нет

- Handout-Cb Session 10 & 11 28 & 29 Sep 2021Документ25 страницHandout-Cb Session 10 & 11 28 & 29 Sep 2021Aliasgar TamimОценок пока нет

- Excellent Present at On On Financial Management of Structured ProductsДокумент18 страницExcellent Present at On On Financial Management of Structured ProductsForeclosure Fraud100% (1)

- Manajemen Dana Bank: Source of Fund Use of FundДокумент19 страницManajemen Dana Bank: Source of Fund Use of FundmamalyaОценок пока нет

- Chapter Two The Financial System2 - Eco551Документ25 страницChapter Two The Financial System2 - Eco551Hafiz akbarОценок пока нет

- Introducción A Las FinanzasДокумент47 страницIntroducción A Las FinanzasLeslyОценок пока нет

- TakeoversДокумент22 страницыTakeoversRohit SharmaОценок пока нет

- How Does The Sample Size Affect GARCH Model?: H.S. NG and K.P. LamДокумент4 страницыHow Does The Sample Size Affect GARCH Model?: H.S. NG and K.P. LamSurendra Pal SinghОценок пока нет

- Final Traffic Assessment ReportДокумент4 страницыFinal Traffic Assessment ReportNavarun VashisthОценок пока нет

- Process of Procuring RTA Clearance by Motorela DriversДокумент2 страницыProcess of Procuring RTA Clearance by Motorela DriversJas Em BejОценок пока нет

- Invoice: Invoice From Invoice To Customer InformationДокумент1 страницаInvoice: Invoice From Invoice To Customer Informationnarsampet stcОценок пока нет

- P2 2aДокумент3 страницыP2 2aSakib Ul-abrarОценок пока нет

- f2 Acca Lesson6 (Labour)Документ10 страницf2 Acca Lesson6 (Labour)Mikhail Banhan100% (1)

- Acc501 Final Term Current Solved Paper 2011Документ6 страницAcc501 Final Term Current Solved Paper 2011Ab DulОценок пока нет

- The Great U.S. Fiat Currency FRAUDДокумент7 страницThe Great U.S. Fiat Currency FRAUDin1or100% (1)

- Onboarding Guidelines - Non-Funded Training Partner: A. Eligibility CriteriaДокумент3 страницыOnboarding Guidelines - Non-Funded Training Partner: A. Eligibility CriteriaSendhil KumaranОценок пока нет

- Nicholas Borst CLM Issue 75Документ21 страницаNicholas Borst CLM Issue 75Ghanashyam MuthukumarОценок пока нет

- Economics 2 XiiДокумент17 страницEconomics 2 Xiiapi-3703686Оценок пока нет

- 2584/2 Chotki Ghitti Hyd Rizwana: Acknowledgement Slip 114 (1) (Return of Income Filed Voluntarily For Complete Year)Документ4 страницы2584/2 Chotki Ghitti Hyd Rizwana: Acknowledgement Slip 114 (1) (Return of Income Filed Voluntarily For Complete Year)Mohsin Ali Shaikh vlogsОценок пока нет

- Housing Development Control and Licensing Amendment Act 2012 Amendment Regulations 2015Документ2 страницыHousing Development Control and Licensing Amendment Act 2012 Amendment Regulations 2015Kalaiyalagan KaruppiahОценок пока нет

- Competency Based QuestionsДокумент4 страницыCompetency Based QuestionsLeenaОценок пока нет

- Leather Goods Manufacturing Unit (Wallets) PDFДокумент18 страницLeather Goods Manufacturing Unit (Wallets) PDFSyed Zeeshan AliОценок пока нет

- Solution Manual For Principles of Corporate Finance 12th Edition by BrealeyДокумент3 страницыSolution Manual For Principles of Corporate Finance 12th Edition by BrealeyNgân HàОценок пока нет

- FOREX MARKETS Part 2Документ60 страницFOREX MARKETS Part 2Parvesh AghiОценок пока нет

- Transfer Vehicle Ownership ProcedureДокумент2 страницыTransfer Vehicle Ownership ProcedureAnonymous JmiKPByYwhОценок пока нет

- LCCI Level 3 Certificate in Accounting ASE20104 Resource Booklet Sep 2018Документ8 страницLCCI Level 3 Certificate in Accounting ASE20104 Resource Booklet Sep 2018Musthari KhanОценок пока нет

- Priyanka Arvind PathakДокумент11 страницPriyanka Arvind Pathakravi newaseОценок пока нет

- An Internship Report On Organizational Study at Voltas.Документ88 страницAn Internship Report On Organizational Study at Voltas.Sandeep Saraswat50% (4)

- ChargesДокумент57 страницChargesdeepika sawantОценок пока нет

- EVA Momentum The One Ratio That Tells The Whole StoryДокумент15 страницEVA Momentum The One Ratio That Tells The Whole StorySiYuan ZhangОценок пока нет

- How Is Inflation Calculated?Документ2 страницыHow Is Inflation Calculated?Omkar SheteОценок пока нет

- Multinational Business Finance 15th Edition Eiteman Test BankДокумент14 страницMultinational Business Finance 15th Edition Eiteman Test Bankmisavizebrigadeuieix100% (26)

- GAC+JD FinalsДокумент3 страницыGAC+JD FinalsAmod JadhavОценок пока нет