Вам также может понравиться

- Input Data Sheet For SHS E-Class Record: Learners' NamesДокумент10 страницInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesОценок пока нет

- Input Data Sheet For SHS E-Class Record: Learners' NamesДокумент10 страницInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesОценок пока нет

- Input Data Sheet For SHS E-Class Record: Learners' NamesДокумент11 страницInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesОценок пока нет

- Input Data Sheet For SHS E-Class Record: Learners' NamesДокумент11 страницInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesОценок пока нет

- Input Data Sheet For SHS E-Class Record: Learners' NamesДокумент11 страницInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesОценок пока нет

- PDPRДокумент1 страницаPDPRMariya BhavesОценок пока нет

- Grading Sheet For FINANCE 2Документ1 страницаGrading Sheet For FINANCE 2Mariya BhavesОценок пока нет

- SPss Project BeveragesДокумент6 страницSPss Project BeveragesMariya BhavesОценок пока нет

- Logistic ManagementДокумент1 страницаLogistic ManagementMariya BhavesОценок пока нет

- Strategic Activity 5Документ4 страницыStrategic Activity 5Mariya BhavesОценок пока нет

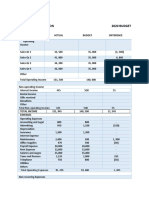

- Twinnies Corporation 2020 BudgetДокумент2 страницыTwinnies Corporation 2020 BudgetMariya BhavesОценок пока нет

- Chapter 6-7 Strategic ManagementДокумент5 страницChapter 6-7 Strategic ManagementMariya BhavesОценок пока нет

- Chapter 2-3 Strategic ManagementДокумент5 страницChapter 2-3 Strategic ManagementMariya BhavesОценок пока нет

- Chapter 3Документ3 страницыChapter 3Mariya BhavesОценок пока нет

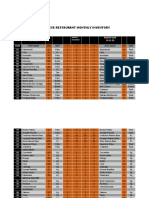

- Japanese Restaurant Monthly InventoryДокумент2 страницыJapanese Restaurant Monthly InventoryMariya BhavesОценок пока нет

- Chapter 3Документ5 страницChapter 3Mariya BhavesОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Cascade Configuration Tool: Installation and Operations ManualДокумент22 страницыCascade Configuration Tool: Installation and Operations ManualAndrés GarciaОценок пока нет

- Ageing World ReportДокумент4 страницыAgeing World Reporttheresia anggitaОценок пока нет

- Wapda CSR 2013 Zone 3Документ245 страницWapda CSR 2013 Zone 3Naveed Shaheen91% (11)

- 50 Interview Question Code Galatta - HandbookДокумент16 страниц50 Interview Question Code Galatta - HandbookSai DhanushОценок пока нет

- Science: BiologyДокумент22 страницыScience: BiologyMike RollideОценок пока нет

- 250 Conversation StartersДокумент28 страниц250 Conversation StartersmuleОценок пока нет

- Soal PTS Vii BigДокумент6 страницSoal PTS Vii Bigdimas awe100% (1)

- Bhagavatam English Chapter 10bДокумент22 страницыBhagavatam English Chapter 10bsrimatsimhasaneshwarОценок пока нет

- ASC 2020-21 Questionnaire PDFДокумент11 страницASC 2020-21 Questionnaire PDFShama PhotoОценок пока нет

- Ielts Reading Actual Tests With Suggested Answers Oct 2021 JДокумент508 страницIelts Reading Actual Tests With Suggested Answers Oct 2021 JHarpreet Singh JohalОценок пока нет

- Ibridge Product Spec SheetДокумент2 страницыIbridge Product Spec SheetanupamОценок пока нет

- Bachelors of Engineering: Action Research Project - 1Документ18 страницBachelors of Engineering: Action Research Project - 1manasi rathiОценок пока нет

- Automotive SensorsДокумент20 страницAutomotive SensorsahmedОценок пока нет

- The Journeyto Learning Throughthe Learning StylesДокумент93 страницыThe Journeyto Learning Throughthe Learning Stylesastria alosОценок пока нет

- Federal Public Service CommissionДокумент2 страницыFederal Public Service CommissionNasir LatifОценок пока нет

- Paper 1 Set 2 PDFДокумент531 страницаPaper 1 Set 2 PDFabdul rehman aОценок пока нет

- Tom Rockmore - Hegel's Circular EpistemologyДокумент213 страницTom Rockmore - Hegel's Circular Epistemologyluiz100% (1)

- 04 DosimetryДокумент104 страницы04 DosimetryEdmond ChiangОценок пока нет

- Manual Daily Calorie Log: MyfitnesspalДокумент4 страницыManual Daily Calorie Log: MyfitnesspalAzariah Burnside100% (2)

- Potassium Permanganate CARUSOL CarusCoДокумент9 страницPotassium Permanganate CARUSOL CarusColiebofreakОценок пока нет

- Math Habits of MindДокумент12 страницMath Habits of MindAzmi SallehОценок пока нет

- Pipetite: Pipetite Forms A Flexible, Sanitary Seal That Allows For Pipeline MovementДокумент4 страницыPipetite: Pipetite Forms A Flexible, Sanitary Seal That Allows For Pipeline MovementAngela SeyerОценок пока нет

- Lab 6 Data VisualizationДокумент8 страницLab 6 Data VisualizationRoaster GuruОценок пока нет

- CN Blue Love Rigt Lyrics (Romanized)Документ3 страницыCN Blue Love Rigt Lyrics (Romanized)Dhika Halet NinridarОценок пока нет

- Review of Ventura's "An Overview of Child Psychology in The Philippines"Документ2 страницыReview of Ventura's "An Overview of Child Psychology in The Philippines"Irene CayeОценок пока нет

- AA1 Adventure Anthology One r14Документ85 страницAA1 Adventure Anthology One r14dachda100% (1)

- Manual CAT 345C LДокумент20 страницManual CAT 345C LRicardo SotoОценок пока нет

- Lay Planning TypesДокумент1 страницаLay Planning TypesGaurav Shakya100% (1)

- Croda Smarter Polymers Guide Sep 2019Документ20 страницCroda Smarter Polymers Guide Sep 2019Keith Tamura100% (1)

- Zoology LAB Scheme of Work 2023 Hsslive HSSДокумент7 страницZoology LAB Scheme of Work 2023 Hsslive HSSspookyvibee666Оценок пока нет