Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Paradigm Shift of Waste ManagementДокумент10 страницParadigm Shift of Waste ManagementNaMeiNaОценок пока нет

- GDP For 1st QuarterДокумент5 страницGDP For 1st QuarterUmesh MatkarОценок пока нет

- Ethanol As Fuel Pros and Cons PDFДокумент2 страницыEthanol As Fuel Pros and Cons PDFRositaОценок пока нет

- True False and MCQ Demand and Supply.Документ2 страницыTrue False and MCQ Demand and Supply.Nikoleta TrudovОценок пока нет

- Test Bank For Entrepreneurship The Art Science and Process For Success 3rd Edition Charles Bamford Garry BrutonДокумент15 страницTest Bank For Entrepreneurship The Art Science and Process For Success 3rd Edition Charles Bamford Garry Brutonsaleburrock1srОценок пока нет

- "Comparative Study On Defects and Inspection System of Woven Fabrics in Different RMG Industry in Bangladesh" 1Документ17 страниц"Comparative Study On Defects and Inspection System of Woven Fabrics in Different RMG Industry in Bangladesh" 1S.m. MahasinОценок пока нет

- Bilo GraphyДокумент9 страницBilo Graphyvimalvijayan89Оценок пока нет

- Proforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017Документ1 страницаProforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017lê thu phươngОценок пока нет

- 1 Plastics Give A Helpful HandДокумент10 страниц1 Plastics Give A Helpful HandNIranjanaОценок пока нет

- Daniela Del Bene e Kesang ThakurДокумент23 страницыDaniela Del Bene e Kesang ThakurYara CerpaОценок пока нет

- How To Start A Travel and Tour BusinessДокумент3 страницыHow To Start A Travel and Tour BusinessGrace LeonardoОценок пока нет

- Why Poverty Has Declined - Inquirer OpinionДокумент6 страницWhy Poverty Has Declined - Inquirer OpinionRamon T. Conducto IIОценок пока нет

- Begging in Rural India and BangladeshДокумент3 страницыBegging in Rural India and BangladeshAkshay NarangОценок пока нет

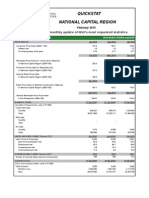

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsДокумент3 страницыQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiОценок пока нет

- Dodi SetyawanДокумент2 страницыDodi SetyawanEgao Mayukko Dina MizushimaОценок пока нет

- Account Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент8 страницAccount Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajwinder SandhuОценок пока нет

- Factors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Документ53 страницыFactors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Aditya KumarОценок пока нет

- Melinda Coopers Family Values Between Neoliberalism and The New Social ConservatismДокумент4 страницыMelinda Coopers Family Values Between Neoliberalism and The New Social ConservatismmarianfelizОценок пока нет

- Marketing Strategy An OverviewДокумент13 страницMarketing Strategy An OverviewRobin PalanОценок пока нет

- Luis Rodrigo Ubeda: Mission, Values and Culture of POTCДокумент6 страницLuis Rodrigo Ubeda: Mission, Values and Culture of POTCLuis Rodrigo ÚbedaОценок пока нет

- History of Tata SteelДокумент13 страницHistory of Tata Steelmanoj rakesh100% (4)

- TC2014 15 NirdДокумент124 страницыTC2014 15 Nirdssvs1234Оценок пока нет

- Everything To Know About Customer Lifetime Value - Ebook PDFДокумент28 страницEverything To Know About Customer Lifetime Value - Ebook PDFNishi GoyalОценок пока нет

- Basic Concept of International DevelopmentДокумент9 страницBasic Concept of International DevelopmentAbdullah AbdulrehmanОценок пока нет

- Before The Notary PublicДокумент4 страницыBefore The Notary PublicImdad KhanОценок пока нет

- Problems and Prospects of Organic Horticultural Farming in BangladeshДокумент10 страницProblems and Prospects of Organic Horticultural Farming in BangladeshMahamud Hasan PrinceОценок пока нет

- Certificate - BG. MARINE POWER 3028 - TB. KIETRANS 23Документ3 страницыCertificate - BG. MARINE POWER 3028 - TB. KIETRANS 23Habibie MikhailОценок пока нет

- Receipt ClerkДокумент1 страницаReceipt Clerksonabeta07Оценок пока нет

- The Business Model CanvasДокумент2 страницыThe Business Model CanvasJohn HowardОценок пока нет

- ECO 303 PQsДокумент21 страницаECO 303 PQsoyekanolalekan028284Оценок пока нет