Вам также может понравиться

- Commercial Banking in IndiaДокумент8 страницCommercial Banking in IndiaSachin SinghОценок пока нет

- Non-Banking Financial InstitutionsДокумент4 страницыNon-Banking Financial Institutionscool_vardahОценок пока нет

- Commercial Banking in IndiaДокумент12 страницCommercial Banking in IndiamahajandenikaОценок пока нет

- HDFC BankДокумент138 страницHDFC BankKrishna KanthОценок пока нет

- UntitledДокумент16 страницUntitledಲೋಕೇಶ್ ಎಂ ಗೌಡОценок пока нет

- Banking Final BibliographyДокумент93 страницыBanking Final BibliographyDipen AshwaniОценок пока нет

- 180 Sample-Chapter PDFДокумент15 страниц180 Sample-Chapter PDFhanumanthaiahgowdaОценок пока нет

- An Anlitical Study of Loan Scheames of Icici Bank in Nagpur CityДокумент52 страницыAn Anlitical Study of Loan Scheames of Icici Bank in Nagpur CityVipin KushwahaОценок пока нет

- 03 - IntroductionДокумент50 страниц03 - IntroductionVirendra JhaОценок пока нет

- Banking and Insurance OverviewДокумент27 страницBanking and Insurance OverviewRajeshwariОценок пока нет

- Banking Financial Services Management - Unit 1: Overview of Indian Banking SystemДокумент64 страницыBanking Financial Services Management - Unit 1: Overview of Indian Banking SystemtkashvinОценок пока нет

- NBFC Module 2 CompletedДокумент27 страницNBFC Module 2 CompletedAneesha AkhilОценок пока нет

- Shriram Finace Sip ReportДокумент64 страницыShriram Finace Sip Reportshiv khillari75% (4)

- Banking SystemДокумент10 страницBanking SystemVaishnavi JhaОценок пока нет

- PART A NewДокумент22 страницыPART A NewMadhav DavdaОценок пока нет

- Analysis of Loan Process and Competitors of Magma FincorpДокумент39 страницAnalysis of Loan Process and Competitors of Magma Fincorp983858nandini80% (5)

- 08 Chapter 01Документ44 страницы08 Chapter 01anwari risalathОценок пока нет

- Principles & Practices of Indian Banking: Financial System OverviewДокумент33 страницыPrinciples & Practices of Indian Banking: Financial System OverviewKunal AggarwalОценок пока нет

- NBFC Edelweise Retail FinanceДокумент14 страницNBFC Edelweise Retail FinancesunitaОценок пока нет

- Module IiiДокумент12 страницModule IiiKrishna GuptaОценок пока нет

- Banking N FinanceДокумент27 страницBanking N FinancetechworkpressОценок пока нет

- Sem V2019 PatternДокумент41 страницаSem V2019 PatternAayushi ViraniОценок пока нет

- Financial Services & Institutions - An IntroductionДокумент11 страницFinancial Services & Institutions - An IntroductionMayank KumarОценок пока нет

- Director AssignmentДокумент16 страницDirector AssignmentUma VermaОценок пока нет

- Report On Banking SectorДокумент8 страницReport On Banking SectorSaurabh Paharia100% (1)

- Financial Performance of BankДокумент14 страницFinancial Performance of BankManjunath ShettyОценок пока нет

- MB-4056 Bank Management and Other Financial ServicesДокумент28 страницMB-4056 Bank Management and Other Financial Servicesxiexie itsmeОценок пока нет

- Indian Financial System: Role of Commercial BanksДокумент11 страницIndian Financial System: Role of Commercial BanksRohit GoyalОценок пока нет

- JAIIB Principles of Banking MOD AДокумент32 страницыJAIIB Principles of Banking MOD AMisha Kapoor AroraОценок пока нет

- Banking Regulations and Capital RequirementsДокумент18 страницBanking Regulations and Capital RequirementsSunanda SharmaОценок пока нет

- Overview of IFSДокумент21 страницаOverview of IFSMaiyakabetaОценок пока нет

- Symbi Banking Lecture Notes 2012Документ29 страницSymbi Banking Lecture Notes 2012Abhijit DeshpandeОценок пока нет

- Symbi Banking Lecture Notes 2012Документ29 страницSymbi Banking Lecture Notes 2012Ankur ChauhanОценок пока нет

- A) Brief Relevance of The Topic and The Organization.: GrowthДокумент38 страницA) Brief Relevance of The Topic and The Organization.: GrowthShree CyberiaОценок пока нет

- Commercial Bank in India: Public Sector Private Sector Foreign SectorДокумент13 страницCommercial Bank in India: Public Sector Private Sector Foreign SectorAshish SharmaОценок пока нет

- Role of Financial InstitutesДокумент44 страницыRole of Financial InstitutesJitender KumarОценок пока нет

- Financial Intermediation BusinessДокумент96 страницFinancial Intermediation BusinessRoba AbeyuОценок пока нет

- Non Banking Financial CompanyДокумент39 страницNon Banking Financial Companymanoj phadtareОценок пока нет

- Vaibhav (Banking and Insurance) - 1Документ10 страницVaibhav (Banking and Insurance) - 1Vaibhav TiwariОценок пока нет

- Scope and Role of Key Financial Institutions in India's Money MarketДокумент5 страницScope and Role of Key Financial Institutions in India's Money MarketVishnu JadhavОценок пока нет

- FINANCIAL INSTITUTION REGULATORSДокумент31 страницаFINANCIAL INSTITUTION REGULATORSManish KumarОценок пока нет

- (1) Intro. to Financial Services (cir. 14.9.2023)Документ16 страниц(1) Intro. to Financial Services (cir. 14.9.2023)Sonali MoreОценок пока нет

- Conversion of DFI's Into Banks With Special Reference To ICICI and IDBI BanksДокумент63 страницыConversion of DFI's Into Banks With Special Reference To ICICI and IDBI Banksdarshan71219892205100% (1)

- Bank Lending EnvironmentДокумент7 страницBank Lending EnvironmentMoses OlabodeОценок пока нет

- WWW - Edutap.Co - in Hello@Edutap - Co.In: Query? / 8 1 4 6 2 0 7 2 4 1Документ37 страницWWW - Edutap.Co - in Hello@Edutap - Co.In: Query? / 8 1 4 6 2 0 7 2 4 1vikalpОценок пока нет

- MBFS Unit 1Документ48 страницMBFS Unit 1pearlksrОценок пока нет

- Comparative Analysis On Non Performing Assets of Private and Public Sector BanksДокумент50 страницComparative Analysis On Non Performing Assets of Private and Public Sector BanksAvinash AndyОценок пока нет

- Interview QuestionДокумент73 страницыInterview Questionaditya0004Оценок пока нет

- Introduction to Banking Industry and Credit AppraisalДокумент47 страницIntroduction to Banking Industry and Credit AppraisalJasmine KaurОценок пока нет

- Financial GlossaryДокумент63 страницыFinancial Glossarymikedelta28Оценок пока нет

- Trend Analysis FinanceДокумент17 страницTrend Analysis FinanceNarasimhaPrasadОценок пока нет

- Important Topics For Bank InterviewДокумент10 страницImportant Topics For Bank Interviewpooja kumariОценок пока нет

- BII Final NOTES UNIT1Документ26 страницBII Final NOTES UNIT1SOHAIL makandarОценок пока нет

- Valuation of Goodwill and Shares ProjectДокумент41 страницаValuation of Goodwill and Shares ProjectakshataОценок пока нет

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsОт EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsОценок пока нет

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)От EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Оценок пока нет

- Bank Fundamentals: An Introduction to the World of Finance and BankingОт EverandBank Fundamentals: An Introduction to the World of Finance and BankingРейтинг: 4.5 из 5 звезд4.5/5 (4)

- Regional Rural Banks of India: Evolution, Performance and ManagementОт EverandRegional Rural Banks of India: Evolution, Performance and ManagementОценок пока нет

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceОт EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceРейтинг: 4 из 5 звезд4/5 (9)

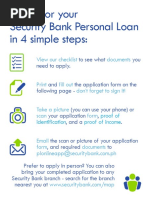

- Apply for a Personal Loan in 4 Easy StepsДокумент2 страницыApply for a Personal Loan in 4 Easy StepsRonald TemajoОценок пока нет

- Canara Bank Form 589-RSNДокумент13 страницCanara Bank Form 589-RSNshardaashish0075% (4)

- WillsДокумент863 страницыWillsAnonymous 5k7iGy0% (1)

- Indian Banking System Project ReportДокумент55 страницIndian Banking System Project ReportManish GoyalОценок пока нет

- Deed of Sale With Assumption of MortgageДокумент2 страницыDeed of Sale With Assumption of MortgageTYSON DONGLAОценок пока нет

- Oblicon and SalesДокумент12 страницOblicon and SalesHyman Jay Blanco100% (2)

- Doctrine of Indoor ManagementДокумент14 страницDoctrine of Indoor ManagementAshutosh KumarОценок пока нет

- Internship Report WWWДокумент68 страницInternship Report WWWWasim Imam100% (1)

- Financing - Vs - Forgiving A Debt OverhangДокумент16 страницFinancing - Vs - Forgiving A Debt OverhangDImiskoОценок пока нет

- FinalДокумент60 страницFinalSANKET BANDYOPADHYAYОценок пока нет

- Why Put Money in a BankДокумент11 страницWhy Put Money in a BankBlake AldridgeОценок пока нет

- Inflation Title: Price Stability Definition, Causes, EffectsДокумент20 страницInflation Title: Price Stability Definition, Causes, EffectsSadj GHorbyОценок пока нет

- SSS vs. CA 120 SCRA 707 1983Документ9 страницSSS vs. CA 120 SCRA 707 1983JP DCОценок пока нет

- Orchard Creek ApartmentsДокумент21 страницаOrchard Creek ApartmentsRyan SloanОценок пока нет

- Project On Punjab National BankДокумент86 страницProject On Punjab National BankPrakash Singh100% (1)

- Housing Rules and RegulationsДокумент8 страницHousing Rules and RegulationsJefferson ValerioОценок пока нет

- Sca - Beltran V.PHHCДокумент6 страницSca - Beltran V.PHHCClarkBarcelonОценок пока нет

- Managing Cash Flow: 2011 Pearson Education, Inc. Publishing As Prentice HallДокумент40 страницManaging Cash Flow: 2011 Pearson Education, Inc. Publishing As Prentice HallShristee ManandharОценок пока нет

- TABL2751 Wtabkk 6 General DeductionsДокумент45 страницTABL2751 Wtabkk 6 General DeductionsKarlLiОценок пока нет

- Rayo lacks standing to annul Metrobank foreclosureДокумент2 страницыRayo lacks standing to annul Metrobank foreclosureCzarDuranteОценок пока нет

- Bank of America Short Sale FormsДокумент7 страницBank of America Short Sale FormsPetra NorrisОценок пока нет

- Oc Reyes vs. Tupara CDДокумент1 страницаOc Reyes vs. Tupara CDbam112190Оценок пока нет

- Chapter 10: Key Liabilities for CorporationsДокумент28 страницChapter 10: Key Liabilities for CorporationsAbdul KabeerОценок пока нет

- Unit # 1 Introduction To Financial InstitutionsДокумент4 страницыUnit # 1 Introduction To Financial InstitutionsZaheer Ahmed SwatiОценок пока нет

- Mortel V KasscoДокумент1 страницаMortel V KasscoMichelle BernardoОценок пока нет

- Your Horoscope by Susan MillerДокумент6 страницYour Horoscope by Susan MillerAliОценок пока нет

- 21DJC Day 1 - What Would You DoIf You Have 1 Million DollarsДокумент14 страниц21DJC Day 1 - What Would You DoIf You Have 1 Million DollarsPrinsesaJuuОценок пока нет

- Speculating On Everyday Life: The Cultural Economy of The QuotidianДокумент16 страницSpeculating On Everyday Life: The Cultural Economy of The QuotidianlucianaeuОценок пока нет

- IS202 ER Modeling Lab Test 1Документ3 страницыIS202 ER Modeling Lab Test 1jaslynОценок пока нет

- US Internal Revenue Service: I1040aДокумент80 страницUS Internal Revenue Service: I1040aIRS100% (1)