Вам также может понравиться

- 10 Activity-And Strategic Based-Responsibility AccountingДокумент46 страниц10 Activity-And Strategic Based-Responsibility AccountingGito Novhandra100% (3)

- 07 Support Department Cost AllocationДокумент27 страниц07 Support Department Cost AllocationGito NovhandraОценок пока нет

- 09 Standard Costing A Managerial Control ToolДокумент27 страниц09 Standard Costing A Managerial Control ToolGito Novhandra50% (4)

- 05 Job-Order CostingДокумент28 страниц05 Job-Order CostingGito NovhandraОценок пока нет

- 4-b SambunganДокумент16 страниц4-b SambunganGito NovhandraОценок пока нет

- 08 Fungtional Activity-Based CostingДокумент44 страницы08 Fungtional Activity-Based CostingGito NovhandraОценок пока нет

- 06 Prosess CostingДокумент28 страниц06 Prosess CostingGito NovhandraОценок пока нет

- 04 Activity Based CostingДокумент32 страницы04 Activity Based CostingGito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH19Документ36 страницManagement Accounting - Hansen Mowen CH19Gito NovhandraОценок пока нет

- 02 Basic Management Accounting ConceptsДокумент26 страниц02 Basic Management Accounting ConceptsGito NovhandraОценок пока нет

- 4-b SambunganДокумент16 страниц4-b SambunganGito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH16Документ39 страницManagement Accounting - Hansen Mowen CH16Gito NovhandraОценок пока нет

- 01 Introduction The Role, History and Direction of Management AccountingДокумент27 страниц01 Introduction The Role, History and Direction of Management AccountingGito Novhandra100% (1)

- 03 Activiy Cost BehaviorДокумент34 страницы03 Activiy Cost BehaviorGito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH18Документ52 страницыManagement Accounting - Hansen Mowen CH18Gito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH11Документ45 страницManagement Accounting - Hansen Mowen CH11Gito Novhandra100% (3)

- Management Accounting - Hansen Mowen CH17Документ41 страницаManagement Accounting - Hansen Mowen CH17Gito Novhandra100% (1)

- Mastering Body LanguageДокумент4 страницыMastering Body LanguageGito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH07Документ43 страницыManagement Accounting - Hansen Mowen CH07Gito Novhandra100% (1)

- Management Accounting - Hansen Mowen CH14Документ35 страницManagement Accounting - Hansen Mowen CH14Gito Novhandra100% (1)

- CH13Документ38 страницCH13Gito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH09Документ43 страницыManagement Accounting - Hansen Mowen CH09Gito Novhandra100% (4)

- (Sex Seduction Dating) Thunder Cat - Art of ApproachingДокумент94 страницы(Sex Seduction Dating) Thunder Cat - Art of ApproachingDavid Herbert Lawrence100% (6)

- Management Accounting - Hansen Mowen CH12Документ38 страницManagement Accounting - Hansen Mowen CH12Gito Novhandra100% (3)

- Management Accounting - Hansen Mowen CH10Документ57 страницManagement Accounting - Hansen Mowen CH10Gito Novhandra100% (2)

- Management Accounting - Hansen Mowen CH15Документ23 страницыManagement Accounting - Hansen Mowen CH15Gito NovhandraОценок пока нет

- Management Accounting - Hansen Mowen CH08Документ50 страницManagement Accounting - Hansen Mowen CH08Gito Novhandra100% (2)

- Management Accounting - Hansen Mowen CH04Документ49 страницManagement Accounting - Hansen Mowen CH04Gito Novhandra100% (5)

- Management Accounting - Hansen Mowen CH06Документ50 страницManagement Accounting - Hansen Mowen CH06Gito Novhandra100% (3)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Arunar: Organization Structure Training AT MRF LTDДокумент47 страницArunar: Organization Structure Training AT MRF LTDsimranОценок пока нет

- Cebu AssessorДокумент3 страницыCebu AssessorVanny Gimotea BaluyutОценок пока нет

- Nagaland University Act, 1989Документ34 страницыNagaland University Act, 1989Latest Laws TeamОценок пока нет

- Announcement On IAI-SOA IFRI Certificate ProgramДокумент3 страницыAnnouncement On IAI-SOA IFRI Certificate ProgramDeepakIMTОценок пока нет

- Week 4 Professional StandardДокумент14 страницWeek 4 Professional StandardFITRI SAHIDAHОценок пока нет

- MAS 132 - Statistics IIДокумент6 страницMAS 132 - Statistics IIAmit Kumar AroraОценок пока нет

- Enterprise Risk Management Wiki GoodДокумент9 страницEnterprise Risk Management Wiki Goodsarvjeet_kaushalОценок пока нет

- Carm 01Документ3 страницыCarm 01Sivakumar KanchirajuОценок пока нет

- Banco RealДокумент17 страницBanco Realshahidsark100% (1)

- 5.0. Audit Findings/Observations: Summary of Audited FundsДокумент4 страницы5.0. Audit Findings/Observations: Summary of Audited FundsBryoohОценок пока нет

- IFRS Workshop Agenda PDFДокумент18 страницIFRS Workshop Agenda PDFSanath FernandoОценок пока нет

- EB - Romney - AIS13wm 405 440 1 5Документ5 страницEB - Romney - AIS13wm 405 440 1 5Mayang SariОценок пока нет

- 2016 Bsa Qualifying Examination PermitДокумент2 страницы2016 Bsa Qualifying Examination Permitapi-194241825Оценок пока нет

- Service Tax Rules 1994Документ92 страницыService Tax Rules 1994Rishi DebОценок пока нет

- Becg LongДокумент16 страницBecg LongBhaskaran BalamuraliОценок пока нет

- NSDL IAR New FormatДокумент20 страницNSDL IAR New FormatMansoor Ahmed Siddiqui0% (1)

- Donde R. Salazar, Cpa: Independent Auditors' Report The Board of Directors Seabutterfly IncДокумент2 страницыDonde R. Salazar, Cpa: Independent Auditors' Report The Board of Directors Seabutterfly IncJheza Mae PitogoОценок пока нет

- Aud Module 1-5Документ23 страницыAud Module 1-5yaanvinaОценок пока нет

- ch14 Audit ReportДокумент24 страницыch14 Audit ReportErik LegaspiОценок пока нет

- Auditor's Responsibilities Relating The Subsequent Event in An Audit of The Financial StatementsДокумент6 страницAuditor's Responsibilities Relating The Subsequent Event in An Audit of The Financial StatementsHarutraОценок пока нет

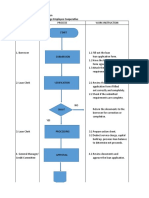

- Process Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeДокумент4 страницыProcess Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeJao FloresОценок пока нет

- Book Keeping AccountancyДокумент8 страницBook Keeping AccountancyNarra JanardhanОценок пока нет

- Comparing AEO, PIP, and C-TPAT international trade compliance programsДокумент2 страницыComparing AEO, PIP, and C-TPAT international trade compliance programsBrenda MartinezОценок пока нет

- HDBFS and CPCДокумент4 страницыHDBFS and CPCMulaneyОценок пока нет

- Islam Aur Jadeed Maeeshat o Tijarat by Mufti Taqi UsmaniДокумент171 страницаIslam Aur Jadeed Maeeshat o Tijarat by Mufti Taqi UsmaniShahood Ahmed100% (1)

- Understanding Auditing ConceptsДокумент27 страницUnderstanding Auditing ConceptsIndahОценок пока нет

- Cost of Goods Sold Assignment Q No. 03 To 09Документ7 страницCost of Goods Sold Assignment Q No. 03 To 09mukarram123100% (2)

- Tendernotice 1Документ82 страницыTendernotice 1viveknigamОценок пока нет

- Blank Taxi Receipt TemplateДокумент4 страницыBlank Taxi Receipt TemplatedigrajОценок пока нет

- CSWIP 3 1 Course ScheduleДокумент2 страницыCSWIP 3 1 Course ScheduleDeepakОценок пока нет