Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Fedex vs. UPS The Battle For Value CaseДокумент18 страницFedex vs. UPS The Battle For Value CaseJose Q. Hdz100% (1)

- Swift Code BankДокумент10 страницSwift Code BankQasseh ChintaОценок пока нет

- Foxchase Topo MapДокумент1 страницаFoxchase Topo MapJim DuncanОценок пока нет

- 2012 Year End Charlottesville Real Estate Nest ReportДокумент9 страниц2012 Year End Charlottesville Real Estate Nest ReportJonathan KauffmannОценок пока нет

- AYLI Press ReleaseДокумент1 страницаAYLI Press ReleaseJim DuncanОценок пока нет

- Crozet - Market Comparison StatisticsДокумент1 страницаCrozet - Market Comparison StatisticsJim DuncanОценок пока нет

- RAD Registration AnnouncementДокумент1 страницаRAD Registration AnnouncementJim DuncanОценок пока нет

- Unisted States Air Force Langley Winds Ensemble - 11 October 2012 in Crozet, VirginiaДокумент1 страницаUnisted States Air Force Langley Winds Ensemble - 11 October 2012 in Crozet, VirginiaJim DuncanОценок пока нет

- Nest Report: Charlottesville Area Real Estate Market Report Q3 2012Документ9 страницNest Report: Charlottesville Area Real Estate Market Report Q3 2012Jonathan KauffmannОценок пока нет

- International Folk Dance Class at Tabor Church in CrozetДокумент1 страницаInternational Folk Dance Class at Tabor Church in CrozetJim DuncanОценок пока нет

- Q2 2012 Charlottesville Nest ReportДокумент9 страницQ2 2012 Charlottesville Nest ReportJim DuncanОценок пока нет

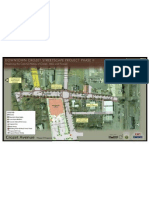

- Downtown Crozet Compiled Projects ImageДокумент1 страницаDowntown Crozet Compiled Projects ImageJim DuncanОценок пока нет

- CMP Streets Cape GoalsДокумент2 страницыCMP Streets Cape GoalsJim DuncanОценок пока нет

- Risky Ques On BANKINGДокумент64 страницыRisky Ques On BANKINGabhishek3012Оценок пока нет

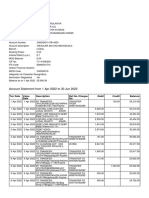

- Account Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницAccount Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceParveen SainiОценок пока нет

- IBPS PO Preliminary Practice Set 5Документ41 страницаIBPS PO Preliminary Practice Set 5Nive AdmiresОценок пока нет

- Front Office AccountingДокумент13 страницFront Office AccountingpranithОценок пока нет

- Environmnetal ServicesДокумент3 страницыEnvironmnetal ServicesRumaisa HamidОценок пока нет

- Project Report HR Bajaj KirtiДокумент65 страницProject Report HR Bajaj Kirtisandeeprandhawa12Оценок пока нет

- Canara BankДокумент7 страницCanara BankPriyankaKulkarni100% (1)

- Payment Process Request Status ReportДокумент1 страницаPayment Process Request Status ReportNishant RanaОценок пока нет

- Acc Project 2021 22Документ14 страницAcc Project 2021 22Piyush GoyalОценок пока нет

- Goldman Sachs Alumni: Currently Serving Name Current Title in Obama Administration Former Goldman Sachs TitleДокумент4 страницыGoldman Sachs Alumni: Currently Serving Name Current Title in Obama Administration Former Goldman Sachs TitleuighuigОценок пока нет

- Xtreme Dance January Newsletter 2012Документ1 страницаXtreme Dance January Newsletter 2012incontroltechОценок пока нет

- LIC Jeevan Saral - Best Insurance Plan FromДокумент18 страницLIC Jeevan Saral - Best Insurance Plan FromRohit JagtapОценок пока нет

- Functions - Duties of The RBI GovernorДокумент4 страницыFunctions - Duties of The RBI GovernorDeepanwita SarОценок пока нет

- Bajaj Allianz Fire InsuranceДокумент44 страницыBajaj Allianz Fire InsuranceDinesh RominaОценок пока нет

- Chapter-I Organization ProfileДокумент27 страницChapter-I Organization ProfileEklo Newar100% (1)

- Intellectual Property Rights As Security For LoansДокумент2 страницыIntellectual Property Rights As Security For LoansReshma Balagopal100% (1)

- Philippine Health Care Providers Vs CirДокумент4 страницыPhilippine Health Care Providers Vs CirArgel Joseph CosmeОценок пока нет

- UK Financial Regulation Ed23-5 PDFДокумент298 страницUK Financial Regulation Ed23-5 PDFVincenzo Somma100% (2)

- 10 - Chapter 2 - Background of Insurance IndustryДокумент29 страниц10 - Chapter 2 - Background of Insurance IndustryBounna PhoumalavongОценок пока нет

- Assessing Fund Performance:: Using Benchmarks in Venture CapitalДокумент13 страницAssessing Fund Performance:: Using Benchmarks in Venture CapitalNamek Zu'biОценок пока нет

- Lend LeaseДокумент4 страницыLend Leaseoakley0817Оценок пока нет

- Rupee Appreciation - Its Impact On Indian EconomyДокумент60 страницRupee Appreciation - Its Impact On Indian Economynikhil100% (1)

- Transformation of E-Payment & It's Impact On BanksДокумент36 страницTransformation of E-Payment & It's Impact On BanksPinky Gupta100% (3)

- Vikas July BillДокумент1 страницаVikas July Billvikas2354_268878339Оценок пока нет

- PDFДокумент374 страницыPDFSimbuОценок пока нет

- Mastercard Switch RulesДокумент80 страницMastercard Switch RulesBaluОценок пока нет

- Claim Form For Health Insurance Policies - Part A Name of Insurance Company: Client NameДокумент4 страницыClaim Form For Health Insurance Policies - Part A Name of Insurance Company: Client NameSatyadev KalraОценок пока нет

- A-EduAchieve 2 Brochure Final 07052019Документ14 страницA-EduAchieve 2 Brochure Final 07052019Navinkumar G.KunarathinamОценок пока нет