Вам также может понравиться

- Emerging Market Mania: Is It Different This Time?Документ3 страницыEmerging Market Mania: Is It Different This Time?api-3820619Оценок пока нет

- L28 29 Non Financial Measures of Performance EvaluationДокумент11 страницL28 29 Non Financial Measures of Performance Evaluationapi-3820619100% (1)

- Rewriting The Rules For India's BanksДокумент4 страницыRewriting The Rules For India's Banksapi-3820619Оценок пока нет

- TP Accounting For Decision Making ZimmermanДокумент1 страницаTP Accounting For Decision Making Zimmermanapi-3820619Оценок пока нет

- L30 The Balanced Scoreboard BLUEДокумент14 страницL30 The Balanced Scoreboard BLUEapi-3820619100% (1)

- L31 Total Cost ManagementДокумент13 страницL31 Total Cost Managementapi-3820619Оценок пока нет

- L32 Audit As Control ToolДокумент12 страницL32 Audit As Control Toolapi-3820619Оценок пока нет

- L27 MCS in Service IndДокумент13 страницL27 MCS in Service Indapi-3820619Оценок пока нет

- L21 Long Range PlanningДокумент7 страницL21 Long Range Planningapi-3820619Оценок пока нет

- L22 Scope of MCS SP OP MC TransparencyДокумент1 страницаL22 Scope of MCS SP OP MC Transparencyapi-3820619Оценок пока нет

- L23 BudgetingДокумент11 страницL23 Budgetingapi-3820619Оценок пока нет

- L24 Problems On Bud GettingДокумент7 страницL24 Problems On Bud Gettingapi-3820619Оценок пока нет

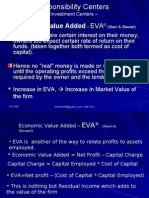

- L19 RC Problems On ROI and EVAДокумент8 страницL19 RC Problems On ROI and EVAapi-3820619100% (2)

- L20 Bench MarkingДокумент6 страницL20 Bench Markingapi-3820619Оценок пока нет

- L15 L16 Problems On TPДокумент15 страницL15 L16 Problems On TPapi-3820619Оценок пока нет

- L14 TP Cost Based MethodДокумент9 страницL14 TP Cost Based Methodapi-3820619Оценок пока нет

- L16 Problem On Transfer PricingДокумент20 страницL16 Problem On Transfer Pricingapi-382061990% (20)

- L18 RC Invest Centers EVAДокумент13 страницL18 RC Invest Centers EVAapi-3820619Оценок пока нет

- L17 RC Investment Center ROIДокумент13 страницL17 RC Investment Center ROIapi-3820619100% (1)

- L15 Other Methods of TPДокумент2 страницыL15 Other Methods of TPapi-3820619Оценок пока нет

- XL330 JIT RemovedДокумент2 страницыXL330 JIT Removedapi-3820619Оценок пока нет

- L13 TP MKT Based MethodДокумент8 страницL13 TP MKT Based Methodapi-3820619Оценок пока нет

- L12 Problem On Profitability Measures For Profit CenterДокумент8 страницL12 Problem On Profitability Measures For Profit Centerapi-3820619Оценок пока нет

- XL260 Ratio RemovedДокумент20 страницXL260 Ratio Removedapi-3820619Оценок пока нет

- L9 Input Output RelationshipДокумент6 страницL9 Input Output Relationshipapi-3820619Оценок пока нет

- XL260 Variance RemovedДокумент11 страницXL260 Variance Removedapi-3820619Оценок пока нет

- XL100 RC Disc Exp Added in L10Документ5 страницXL100 RC Disc Exp Added in L10api-3820619Оценок пока нет

- L8 MCS Formal ProcessДокумент3 страницыL8 MCS Formal Processapi-3820619100% (1)

- L7 Goal Congruence MCS Form ProcessДокумент10 страницL7 Goal Congruence MCS Form Processapi-3820619100% (7)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Johari WindowДокумент7 страницJohari WindowSarthak Priyank VermaОценок пока нет

- 12 Constructor and DistructorДокумент15 страниц12 Constructor and DistructorJatin BhasinОценок пока нет

- Practical Applications of Electrical ConductorsДокумент12 страницPractical Applications of Electrical ConductorsHans De Keulenaer100% (5)

- Cuentos CADEДокумент6 страницCuentos CADEMäuricio E. González VegaОценок пока нет

- CCTV Guidelines - Commission Letter Dated 27.08.2022Документ2 страницыCCTV Guidelines - Commission Letter Dated 27.08.2022Sumeet TripathiОценок пока нет

- 24 Inch MonitorДокумент10 страниц24 Inch MonitorMihir SaveОценок пока нет

- Pell (2017) - Trends in Real-Time Traffic SimulationДокумент8 страницPell (2017) - Trends in Real-Time Traffic SimulationJorge OchoaОценок пока нет

- Errata V0.1 For IT8212F V0.4.2Документ2 страницыErrata V0.1 For IT8212F V0.4.2tryujiОценок пока нет

- 2011 - Papanikolaou E. - Markatos N. - Int J Hydrogen EnergyДокумент9 страниц2011 - Papanikolaou E. - Markatos N. - Int J Hydrogen EnergyNMarkatosОценок пока нет

- E9 Đề khảo sát Trưng Vương 2022 ex No 1Документ4 страницыE9 Đề khảo sát Trưng Vương 2022 ex No 1Minh TiếnОценок пока нет

- Chapter 5 - Amino acids and Proteins: Trần Thị Minh ĐứcДокумент59 страницChapter 5 - Amino acids and Proteins: Trần Thị Minh ĐứcNguyễn SunОценок пока нет

- Corporate Valuation WhartonДокумент6 страницCorporate Valuation Whartonebrahimnejad64Оценок пока нет

- Lupon National Comprehensive High School Ilangay, Lupon, Davao Oriental Grade 10-Household ServicesДокумент4 страницыLupon National Comprehensive High School Ilangay, Lupon, Davao Oriental Grade 10-Household ServicesJohn Eirhene Intia BarreteОценок пока нет

- Adigrat University: College of Engineering and Technology Department of Chemical EnginneringДокумент39 страницAdigrat University: College of Engineering and Technology Department of Chemical EnginneringSeid Aragaw100% (1)

- Final Notice To Global Girls Degree CollgeДокумент2 страницыFinal Notice To Global Girls Degree CollgeIbn E AdamОценок пока нет

- Your Bentley Bentayga V8: PresentingДокумент9 страницYour Bentley Bentayga V8: PresentingThomas SeiferthОценок пока нет

- D15 Hybrid P1 QPДокумент6 страницD15 Hybrid P1 QPShaameswary AnnadoraiОценок пока нет

- HUAWEI PowerCube 500Документ41 страницаHUAWEI PowerCube 500soumen95Оценок пока нет

- AREMA Shoring GuidelinesДокумент25 страницAREMA Shoring GuidelinesKCHESTER367% (3)

- Intraoperative RecordДокумент2 страницыIntraoperative Recordademaala06100% (1)

- Useful Methods in CatiaДокумент30 страницUseful Methods in CatiaNastase Corina100% (2)

- NDT HandBook Volume 10 (NDT Overview)Документ600 страницNDT HandBook Volume 10 (NDT Overview)mahesh95% (19)

- Basler Electric TCCДокумент7 страницBasler Electric TCCGalih Trisna NugrahaОценок пока нет

- Tugas Inggris Text - Kelas 9Документ27 страницTugas Inggris Text - Kelas 9salviane.theandra.jОценок пока нет

- COMMISSIONING COUPLE Aafidavit SANKET DOCTORДокумент2 страницыCOMMISSIONING COUPLE Aafidavit SANKET DOCTORYogesh ChaudhariОценок пока нет

- Crown BeverageДокумент13 страницCrown BeverageMoniruzzaman JurorОценок пока нет

- Model Contract FreelanceДокумент3 страницыModel Contract FreelancemarcosfreyervinnorskОценок пока нет

- Onco Case StudyДокумент2 страницыOnco Case StudyAllenОценок пока нет

- Polyembryony &its ImportanceДокумент17 страницPolyembryony &its ImportanceSURIYA PRAKASH GОценок пока нет

- Session 1: Strategic Marketing - Introduction & ScopeДокумент38 страницSession 1: Strategic Marketing - Introduction & ScopeImrul Hasan ChowdhuryОценок пока нет