Вам также может понравиться

- Indirect Tax 2Документ35 страницIndirect Tax 2lowell789Оценок пока нет

- Profit & Loss Account of Idea Cellular - in Rs. Cr.Документ3 страницыProfit & Loss Account of Idea Cellular - in Rs. Cr.lowell789Оценок пока нет

- Indian Textile Industry: Higher Standards............ Making A Difference For YouДокумент18 страницIndian Textile Industry: Higher Standards............ Making A Difference For YouRaj KumarОценок пока нет

- TTPДокумент2 страницыTTPlowell789Оценок пока нет

- Off-Loading and Priority ManagementДокумент22 страницыOff-Loading and Priority Managementlowell789Оценок пока нет

- Athishi CaseДокумент4 страницыAthishi Caselowell789Оценок пока нет

- SwitchДокумент10 страницSwitchlowell789Оценок пока нет

- Project On Customer Satisfaction Towards Mobile Service ProvidersДокумент992 страницыProject On Customer Satisfaction Towards Mobile Service Providerslowell789Оценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Aquakultur Scylla (Kepiting Bakau)Документ100 страницAquakultur Scylla (Kepiting Bakau)sjahrierОценок пока нет

- Land Degradation and ConservationДокумент8 страницLand Degradation and ConservationsvschauhanОценок пока нет

- Summative Test No. 1 in Science 5 Fourth Quarter.Документ3 страницыSummative Test No. 1 in Science 5 Fourth Quarter.BALETEОценок пока нет

- Microorganisms Friend and FoeДокумент27 страницMicroorganisms Friend and Foedotcomddn100% (1)

- Forest EcosystemДокумент16 страницForest EcosystemThavakka PnmОценок пока нет

- Ti Bajssít Ajkáyo NaljjajjegénjДокумент8 страницTi Bajssít Ajkáyo NaljjajjegénjDennis ValdezОценок пока нет

- Scope and Prospectus of Organic Farming in PunjabДокумент64 страницыScope and Prospectus of Organic Farming in PunjabDr. MANOJ SHARMA100% (11)

- Labour, Material Ratio Vettikavala BlockДокумент1 страницаLabour, Material Ratio Vettikavala BlockVishnu DasОценок пока нет

- Piñatex Intro Card - A5Документ1 страницаPiñatex Intro Card - A5Samuel Arévalo GОценок пока нет

- Study of Value Chain and Value Additive Process of NTFP'S Like Tamarind in Indian States Aneesh Ghosh 20125010 MBAДокумент7 страницStudy of Value Chain and Value Additive Process of NTFP'S Like Tamarind in Indian States Aneesh Ghosh 20125010 MBAAneeshGhoshОценок пока нет

- Agbes Accomplishment Report On GPPДокумент4 страницыAgbes Accomplishment Report On GPPCharry Mae Jose CacabanОценок пока нет

- Self-Propelled Uniport 2000 PlusДокумент8 страницSelf-Propelled Uniport 2000 PlusMarceloGonçalvesОценок пока нет

- Vriksha Ayurveda Subhashini Sridhar Et Al (CIKS)Документ27 страницVriksha Ayurveda Subhashini Sridhar Et Al (CIKS)Samskrita Bharati Kanchi VibhagОценок пока нет

- Pdop Paquibato 06 June 2014Документ80 страницPdop Paquibato 06 June 2014Glorious El Domine100% (1)

- Social Development TheoryДокумент15 страницSocial Development TheoryNikon ArbusОценок пока нет

- Laka Dong TurmericДокумент4 страницыLaka Dong TurmericSam TanОценок пока нет

- Evaluation of Fruits Cultivar and Different Harvest Times of Damghan Pistachio To Early Split Complications and Contamination To The Aspergillus Flavus FungusДокумент14 страницEvaluation of Fruits Cultivar and Different Harvest Times of Damghan Pistachio To Early Split Complications and Contamination To The Aspergillus Flavus FunguserfikaОценок пока нет

- Goan CuisneДокумент3 страницыGoan CuisneSunil KumarОценок пока нет

- Soil FungiДокумент1 страницаSoil FungiDimasalang PerezОценок пока нет

- Historical Development of The Gulf Intracoastal WaterwayДокумент36 страницHistorical Development of The Gulf Intracoastal WaterwaykinoyhourglassОценок пока нет

- Chapter - 6 Natural Vegetation of IndiaДокумент9 страницChapter - 6 Natural Vegetation of IndiaMansha ChhetriОценок пока нет

- Ma. Aika S. Doronela 2015-10952 CRSC U-2LДокумент5 страницMa. Aika S. Doronela 2015-10952 CRSC U-2LMaika DoronelaОценок пока нет

- The Road To Sustainable Water and Nutrient Management in Soil-Less Culture in Dutch Greenhouse HorticultureДокумент8 страницThe Road To Sustainable Water and Nutrient Management in Soil-Less Culture in Dutch Greenhouse Horticulturekhaled bassalОценок пока нет

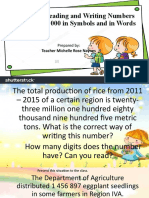

- Read and Write Numbers Up To 10 000 000 in Symbols and in WordsДокумент13 страницRead and Write Numbers Up To 10 000 000 in Symbols and in WordsMichelle Rose NaynesОценок пока нет

- Grade5 A English 12-11-2012 SmallerДокумент228 страницGrade5 A English 12-11-2012 Smallerapi-198270301100% (1)

- The Prospects For The Development of The Key Sectors in The Warmińsko-Mazurskie Voivodeship Research ReportДокумент43 страницыThe Prospects For The Development of The Key Sectors in The Warmińsko-Mazurskie Voivodeship Research ReportGarski MultimediaОценок пока нет

- Who Are The Personages Mentioned and What Is Their Relationship With Each Other?Документ6 страницWho Are The Personages Mentioned and What Is Their Relationship With Each Other?Gilbert TumampoОценок пока нет

- The Urban Gardener 5Документ5 страницThe Urban Gardener 5Anonymous HXLczq3Оценок пока нет

- ICL PR - Ecovadis Rating-V3royДокумент2 страницыICL PR - Ecovadis Rating-V3royAnonymous NjRXOWhMDOОценок пока нет

- Multi-Storied Residential BuildingДокумент43 страницыMulti-Storied Residential BuildingNitesh100% (1)