Вам также может понравиться

- Law of BankingДокумент18 страницLaw of BankingBHARATH JAJUОценок пока нет

- Commercial BankingДокумент3 страницыCommercial BankingVenkat IyerОценок пока нет

- Commercial BankДокумент11 страницCommercial BankVaibhavi BorhadeОценок пока нет

- Ibfs Unit 3Документ9 страницIbfs Unit 3220106062Оценок пока нет

- State BanksДокумент6 страницState BanksVikram LodhaОценок пока нет

- Econon Paper BanklendingДокумент61 страницаEconon Paper BanklendingDaipayan MajumderОценок пока нет

- Commercial Bank: Umashankar Patel (Mba-0901120527) Sibbu Kumar Tyagi (Mba-0901120526)Документ11 страницCommercial Bank: Umashankar Patel (Mba-0901120527) Sibbu Kumar Tyagi (Mba-0901120526)umapatelОценок пока нет

- Commercial Banking in IndiaДокумент3 страницыCommercial Banking in IndiaPallavi PatelОценок пока нет

- Q1 Banking 1Документ18 страницQ1 Banking 1Adarsh ShetОценок пока нет

- BRO - 4th BBAДокумент41 страницаBRO - 4th BBANithyananda PatelОценок пока нет

- GE - Money and Banking (443,449,508)Документ16 страницGE - Money and Banking (443,449,508)Kriti GandhiОценок пока нет

- Commercial BankingДокумент4 страницыCommercial Bankingsn nОценок пока нет

- Meaning of Banking: 1. Central BanksДокумент6 страницMeaning of Banking: 1. Central BanksMuskanОценок пока нет

- Ifs Cia 3Документ11 страницIfs Cia 3Rohit GoyalОценок пока нет

- U2 Banking InstitutionsДокумент12 страницU2 Banking Institutionssneha bhongadeОценок пока нет

- Chapter Three Commercial Banking: 1 by SityДокумент10 страницChapter Three Commercial Banking: 1 by SitySeid KassawОценок пока нет

- Banking Pricnciples and Practices Lecture Notes ch3Документ17 страницBanking Pricnciples and Practices Lecture Notes ch3ejigu nigussieОценок пока нет

- Financial Analysis at Indian BankДокумент93 страницыFinancial Analysis at Indian BankAbhay JainОценок пока нет

- Indian BankДокумент94 страницыIndian BankManzuhonnur100% (2)

- ACAD EDGE Edition 7 (Banking)Документ29 страницACAD EDGE Edition 7 (Banking)Damanjot SinghОценок пока нет

- Commercial BankingДокумент30 страницCommercial Bankinghameed.mba055336100% (1)

- Iqra AssignmentДокумент5 страницIqra AssignmentAymen ImtiazОценок пока нет

- Banking NotesДокумент84 страницыBanking NotesNitesh MahatoОценок пока нет

- Final Copy 1Документ15 страницFinal Copy 1gagana sОценок пока нет

- Business Services Part 2Документ11 страницBusiness Services Part 2Santa GlenmarkОценок пока нет

- Banking and InsuranceДокумент11 страницBanking and InsuranceGanpat SoundaleОценок пока нет

- Banking and Its TypeДокумент13 страницBanking and Its TypeJaidev KannanОценок пока нет

- Commercial Banks - Meaning and FunctionsДокумент4 страницыCommercial Banks - Meaning and FunctionsCharu Saxena16Оценок пока нет

- Commercial Banking: Prepared By: M2020 - Jeemol Raji Oommen M2021 - Jidnyasa DarneДокумент33 страницыCommercial Banking: Prepared By: M2020 - Jeemol Raji Oommen M2021 - Jidnyasa DarneJeemol RajiОценок пока нет

- Functions of Commercial Banks of IndiaДокумент5 страницFunctions of Commercial Banks of Indiajunaid sayyedОценок пока нет

- PanchatantraДокумент10 страницPanchatantraBinaya SahooОценок пока нет

- Role of Commercial Bank-1Документ9 страницRole of Commercial Bank-1TanzeemОценок пока нет

- Retail Banking in Allahabad BankДокумент45 страницRetail Banking in Allahabad Bankaru161112Оценок пока нет

- They Do Not Provide, Long-Term CreditДокумент5 страницThey Do Not Provide, Long-Term CreditalemayehuОценок пока нет

- Banking Module 1Документ64 страницыBanking Module 1abhishekmohanty2Оценок пока нет

- Commercial BankДокумент29 страницCommercial BankMahesh RasalОценок пока нет

- A) Central Bank: Types of Commercial Banks: Commercial Banks Are of Three Types I.e., Public SectorДокумент4 страницыA) Central Bank: Types of Commercial Banks: Commercial Banks Are of Three Types I.e., Public Sectorks211185Оценок пока нет

- Unit 1: Foundations For FinanceДокумент3 страницыUnit 1: Foundations For FinanceshruthiОценок пока нет

- Retail Banking of Allahabad BankДокумент50 страницRetail Banking of Allahabad Bankaru161112Оценок пока нет

- Structure of Banking in IndiaДокумент22 страницыStructure of Banking in IndiaTushar Kumar 1140Оценок пока нет

- COMMERCIALДокумент15 страницCOMMERCIALBadbitchОценок пока нет

- Ethiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry BanksДокумент9 страницEthiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry Banksመስቀል ኃይላችን ነውОценок пока нет

- Commercial BanksДокумент3 страницыCommercial BanksRAVIKUMAR RAVIОценок пока нет

- Unit 5 BankingДокумент13 страницUnit 5 BankingAZHAR MUSSAIYIBОценок пока нет

- Macro Economics LBA 402Документ12 страницMacro Economics LBA 402Harshita SarinОценок пока нет

- Commercial Banks (Concepts) - ROHITДокумент17 страницCommercial Banks (Concepts) - ROHITRohit SinhaОценок пока нет

- April 23 2021 12B, C, D, E, F, GChapter14BANKS NotesДокумент16 страницApril 23 2021 12B, C, D, E, F, GChapter14BANKS NotesStephine BochuОценок пока нет

- Assignment: Retail Banking, Rural Banking and Micro FinanceДокумент5 страницAssignment: Retail Banking, Rural Banking and Micro FinanceDipayan Drj SealОценок пока нет

- Financial Performance of BankДокумент14 страницFinancial Performance of BankManjunath ShettyОценок пока нет

- Functions of Commercial Banks ReportДокумент14 страницFunctions of Commercial Banks ReportAryan Khan50% (2)

- Bank ProjectДокумент2 страницыBank ProjectSalik AfzalОценок пока нет

- Title: Analysis of Retail Loans of Bank of Baroda Vis A Vis CompetitorsДокумент42 страницыTitle: Analysis of Retail Loans of Bank of Baroda Vis A Vis CompetitorsSmriti SinghОценок пока нет

- Banking Chapter ThreeДокумент17 страницBanking Chapter ThreeGemechis BussaОценок пока нет

- Commercial Bankes in Sri LankaДокумент15 страницCommercial Bankes in Sri LankaRaashed RamzanОценок пока нет

- Q3. Analyze The Various Functions of Commercial Banking Commercial BankДокумент2 страницыQ3. Analyze The Various Functions of Commercial Banking Commercial BankpraveenОценок пока нет

- Chapter 3 Commercial Banking New - 1535523282Документ13 страницChapter 3 Commercial Banking New - 1535523282Samuel DebebeОценок пока нет

- Functions of Commercial BanksДокумент19 страницFunctions of Commercial BanksAravind Kumar G100% (1)

- Bank Fundamentals: An Introduction to the World of Finance and BankingОт EverandBank Fundamentals: An Introduction to the World of Finance and BankingРейтинг: 4.5 из 5 звезд4.5/5 (4)

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceОт EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceРейтинг: 4 из 5 звезд4/5 (9)

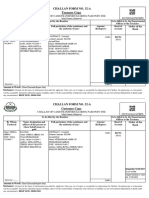

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheДокумент1 страницаChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into Theآرنولڈ دا فینОценок пока нет

- Fee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBLДокумент1 страницаFee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBL Fee Can Be Paid Through HBL Online Banking/HBLImtiaz HattarОценок пока нет

- Mã Ngân Hàng: Bank CodesДокумент20 страницMã Ngân Hàng: Bank CodesJimmy Quan100% (1)

- Mergers and ConsolidationДокумент2 страницыMergers and ConsolidationCarlo Columna100% (1)

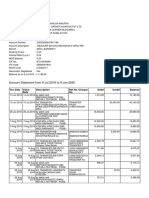

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeОценок пока нет

- Recruitment of Probationary Officers in State Bank of IndiaДокумент4 страницыRecruitment of Probationary Officers in State Bank of Indiaशेरसिंह खदावОценок пока нет

- Key Fact StatementДокумент6 страницKey Fact StatementChoudhary JaatОценок пока нет

- Customer Loyalty Program (Amazon Prime)Документ8 страницCustomer Loyalty Program (Amazon Prime)Navneet GattaniОценок пока нет

- UK Graduate BrochureДокумент24 страницыUK Graduate Brochureshivam markanОценок пока нет

- November 2010 India DailyДокумент147 страницNovember 2010 India DailymitbanОценок пока нет

- 0254J TP5 P8 R2Документ3 страницы0254J TP5 P8 R2meyulia100% (1)

- FaysalbankДокумент541 страницаFaysalbankAnnie DollОценок пока нет

- Fundamentals of Money and BankingДокумент104 страницыFundamentals of Money and BankingSiraajОценок пока нет

- Saving AccountДокумент9 страницSaving AccountpalkhinОценок пока нет

- Accounting Entries in ModulesДокумент88 страницAccounting Entries in ModulesSuresh Joshi100% (2)

- NMP Jun10Документ48 страницNMP Jun10Andrew T. BermanОценок пока нет

- Answers To Chapter 27 and 28 CasesДокумент4 страницыAnswers To Chapter 27 and 28 CasesVic RabayaОценок пока нет

- India's Banking System:: Introduction To Indian Banking IndustryДокумент3 страницыIndia's Banking System:: Introduction To Indian Banking IndustrySathish KumarОценок пока нет

- How The Government Uses Law and Deception To Enslave PeopleДокумент11 страницHow The Government Uses Law and Deception To Enslave Peoplenavenlorens100% (2)

- Jalandhar Amritsar PDFДокумент120 страницJalandhar Amritsar PDFBhagyashreeОценок пока нет

- QuickBooks CUser Study GuideДокумент36 страницQuickBooks CUser Study Guidepetitfm100% (1)

- GSISДокумент96 страницGSISHoven MacasinagОценок пока нет

- 236-Estrada v. Desierto G.R. No. 156160 December 9, 2004Документ7 страниц236-Estrada v. Desierto G.R. No. 156160 December 9, 2004Jopan SJОценок пока нет

- Greenlight Capital Letter (1-Oct-08)Документ0 страницGreenlight Capital Letter (1-Oct-08)brunomarz12345Оценок пока нет

- SBI Equity Savings Fund - Presentation PDFДокумент23 страницыSBI Equity Savings Fund - Presentation PDFPankaj RastogiОценок пока нет

- Corporate Governance Report Bangladesh PDFДокумент311 страницCorporate Governance Report Bangladesh PDFAsiburRahmanОценок пока нет

- Tally Material: Prepared byДокумент81 страницаTally Material: Prepared byfarhanОценок пока нет

- 10 Myths About Financial DerivativesДокумент6 страниц10 Myths About Financial DerivativesArshad FahoumОценок пока нет

- Financial Accounting Chapter 4Документ59 страницFinancial Accounting Chapter 4abhinav2018Оценок пока нет

- Tutorial 1Документ4 страницыTutorial 1Thuận Nguyễn Thị KimОценок пока нет