Вам также может понравиться

- SWOT Analysis of Grameen BankДокумент9 страницSWOT Analysis of Grameen Bankনিশীথিনী কুহুরানীОценок пока нет

- WCAMLF 2019 Distribution ListДокумент11 страницWCAMLF 2019 Distribution ListShubendu DeyОценок пока нет

- MicrofinanceДокумент21 страницаMicrofinancegyanprakashdeb302Оценок пока нет

- Basics of Micro FinanceДокумент49 страницBasics of Micro FinanceFarasat Khan100% (1)

- School of Economics: Davv, IndoreДокумент18 страницSchool of Economics: Davv, IndoreAnveshak PardhiОценок пока нет

- Role of Self Help Groups in Financial InclusionДокумент6 страницRole of Self Help Groups in Financial InclusionSona Kool100% (1)

- TOPIC 3-Microfinance Institutions and OperationsДокумент4 страницыTOPIC 3-Microfinance Institutions and OperationsIsaack MohamedОценок пока нет

- Promotion of Self Help Groups Under The SHG Bank Linkage Programme in IndiaДокумент84 страницыPromotion of Self Help Groups Under The SHG Bank Linkage Programme in IndiaSarveshwar GargОценок пока нет

- SHG Report WorkДокумент86 страницSHG Report Workraja14feb2000Оценок пока нет

- Screenshot 2023-08-04 at 2.35.29 PMДокумент1 страницаScreenshot 2023-08-04 at 2.35.29 PMCb BansalОценок пока нет

- Comparing Microfinance Models PDFДокумент15 страницComparing Microfinance Models PDFlotdonОценок пока нет

- Micro FInancingДокумент54 страницыMicro FInancingShivam SachdevaОценок пока нет

- Self Help Groups (SHGS)Документ24 страницыSelf Help Groups (SHGS)abhinavjogОценок пока нет

- Subject: Central Banking: Name Roll NoДокумент9 страницSubject: Central Banking: Name Roll NoPranav PatoleОценок пока нет

- Concept Paper On The Bank of The Poor - Grameen Bank Microfinance SystemДокумент4 страницыConcept Paper On The Bank of The Poor - Grameen Bank Microfinance SystemGanesh ShakyaОценок пока нет

- Micro FinanceДокумент14 страницMicro FinanceAnjum MehtabОценок пока нет

- Research Paper Suhail Khakil 2010Документ13 страницResearch Paper Suhail Khakil 2010Khaki AudilОценок пока нет

- How It Is PractisedДокумент8 страницHow It Is PractisedmamedurwaaОценок пока нет

- Sterling Institute of Management StudiesДокумент12 страницSterling Institute of Management StudieskristokunsОценок пока нет

- A Study On Thrift and Lending PerformancДокумент12 страницA Study On Thrift and Lending PerformancHarsh DubeyОценок пока нет

- 03 Literature ReviewДокумент13 страниц03 Literature ReviewAmitesh KumarОценок пока нет

- 1752 - SEEP - Delivering Formal Financial Services To SGs - A Handbook For FSPs FINAL 20170407Документ32 страницы1752 - SEEP - Delivering Formal Financial Services To SGs - A Handbook For FSPs FINAL 20170407Tony SsenfumaОценок пока нет

- The Importance of Microcredit Programs in Sustainable DevelopmentДокумент4 страницыThe Importance of Microcredit Programs in Sustainable DevelopmentSafdar IqbalОценок пока нет

- Finding, Recommendation & ConclusionДокумент4 страницыFinding, Recommendation & ConclusionipshahedОценок пока нет

- Synopsis For Analysis of Microfinance in India: BY Jose T George 092103104Документ5 страницSynopsis For Analysis of Microfinance in India: BY Jose T George 092103104Jose GeorgeОценок пока нет

- Women Saving Scheme (Self Help Group)Документ17 страницWomen Saving Scheme (Self Help Group)Revathi RamaswamiОценок пока нет

- Self Help GroupДокумент32 страницыSelf Help GroupRishi KeshavОценок пока нет

- Assgnment On MFIДокумент3 страницыAssgnment On MFINitin MehndirattaОценок пока нет

- CH Allen EgsДокумент5 страницCH Allen EgsY N S Y SОценок пока нет

- The Scope of Micro Finance in Rural AreaДокумент23 страницыThe Scope of Micro Finance in Rural AreavirugargОценок пока нет

- Role of NABARD in Rural DevelopmentДокумент9 страницRole of NABARD in Rural DevelopmentabhinavjogОценок пока нет

- Microfinance in NepalДокумент13 страницMicrofinance in NepalGyan PokhrelОценок пока нет

- Unit 4: Self Help Groups and Micro FinanceДокумент15 страницUnit 4: Self Help Groups and Micro Financeknsvel2000Оценок пока нет

- Micro FinanceДокумент15 страницMicro Financeapi-3774614Оценок пока нет

- Name: Syed Shehryar Ali Zaid ID: 63850 Assignment # 3 SfadДокумент4 страницыName: Syed Shehryar Ali Zaid ID: 63850 Assignment # 3 SfadAsad MemonОценок пока нет

- 3B VillerozДокумент10 страниц3B VillerozTrixie Ros VillerozОценок пока нет

- Notes - Unit 2Документ10 страницNotes - Unit 2ishita sabooОценок пока нет

- Microfinance: The Kalanjiam Community Banking ProgrammeДокумент15 страницMicrofinance: The Kalanjiam Community Banking ProgrammeYash KumarОценок пока нет

- Unit 3 MFRBДокумент41 страницаUnit 3 MFRBSweety TuladharОценок пока нет

- MicrofinanceДокумент58 страницMicrofinanceSamuel Davis100% (1)

- Credit UnionsДокумент5 страницCredit Unionsjamesamani2001Оценок пока нет

- CARE RWANDA Case Study Version 8-22-07Документ56 страницCARE RWANDA Case Study Version 8-22-07Poverty Outreach Working Group (POWG)Оценок пока нет

- SHGДокумент4 страницыSHGsurya_rathiОценок пока нет

- Share Microfin LimitedДокумент2 страницыShare Microfin Limiteddasarup24123Оценок пока нет

- Concept Paper: Business Development & Planning DeptДокумент13 страницConcept Paper: Business Development & Planning DeptArefayne WodajoОценок пока нет

- Introduction To MicrofinanceДокумент19 страницIntroduction To Microfinancedchauhan21Оценок пока нет

- Chapter Four: Micro-Financing InstitutionsДокумент16 страницChapter Four: Micro-Financing InstitutionsBekele DemissieОценок пока нет

- Microfinance: Dr. Amalia G. Dela CruzДокумент35 страницMicrofinance: Dr. Amalia G. Dela CruzAmalia Dela CruzОценок пока нет

- Women Needed Opportunity, Not Charity - They Want Chance, Not Bleeding Hearts" - Prof. Mohammed YunnsДокумент28 страницWomen Needed Opportunity, Not Charity - They Want Chance, Not Bleeding Hearts" - Prof. Mohammed YunnsAf UsmanОценок пока нет

- A Microfinance Institution With A Difference: What We Mean by ShgsДокумент5 страницA Microfinance Institution With A Difference: What We Mean by ShgsnishaОценок пока нет

- plugin-BOrcutt - MicrofinanceДокумент20 страницplugin-BOrcutt - MicrofinanceashishglaitmОценок пока нет

- Research Paper On Self Help GroupsДокумент4 страницыResearch Paper On Self Help Groupscar93zdy100% (1)

- Financial InclusionДокумент3 страницыFinancial Inclusionputul6Оценок пока нет

- Economics Project - Arpit JainДокумент24 страницыEconomics Project - Arpit Jainarpit100% (1)

- The Functional Microfinance Bank: Strategies for SurvivalОт EverandThe Functional Microfinance Bank: Strategies for SurvivalОценок пока нет

- Capital Strategies for Micro-Businesses: Micro-Business Mastery, #1От EverandCapital Strategies for Micro-Businesses: Micro-Business Mastery, #1Оценок пока нет

- Mastering Your Financial Future: A Comprehensive Guide for Gen ZОт EverandMastering Your Financial Future: A Comprehensive Guide for Gen ZОценок пока нет

- Consolidate and Conquer: Winning Strategies for Managing Your DebtОт EverandConsolidate and Conquer: Winning Strategies for Managing Your DebtОценок пока нет

- Guide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1От EverandGuide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1Оценок пока нет

- Annual Rate Contract For The Supply of Electrical Items at IIM IndoreДокумент22 страницыAnnual Rate Contract For The Supply of Electrical Items at IIM IndoreBhavik PrajapatiОценок пока нет

- Proforma Undang-Undang Sekuriti Islam 20182019Документ9 страницProforma Undang-Undang Sekuriti Islam 20182019Ahmad Luqman HakimОценок пока нет

- Chap 002 NotesДокумент43 страницыChap 002 NotessamiullahaslamОценок пока нет

- LIC Jeevan Saral - Best Insurance Plan FromДокумент18 страницLIC Jeevan Saral - Best Insurance Plan FromRohit JagtapОценок пока нет

- Xtreme Dance January Newsletter 2012Документ1 страницаXtreme Dance January Newsletter 2012incontroltechОценок пока нет

- Statement of Affairs of The State Bank of Pakistan Banking Department As On The 27 April, 2018Документ1 страницаStatement of Affairs of The State Bank of Pakistan Banking Department As On The 27 April, 2018muhammad nazirОценок пока нет

- Estudio BrandZ 2018Документ101 страницаEstudio BrandZ 2018Kit CatОценок пока нет

- Pag Ibig Foreclosed Properties Pubbid 2017 05 25 NCR No Discount PDFДокумент25 страницPag Ibig Foreclosed Properties Pubbid 2017 05 25 NCR No Discount PDFrochie cerveraОценок пока нет

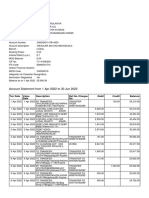

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент8 страницStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePushkar PandeyОценок пока нет

- Statement 517057 86377450 18 06 2020 17 09 2020Документ4 страницыStatement 517057 86377450 18 06 2020 17 09 2020YeazeОценок пока нет

- TK BAI2Документ23 страницыTK BAI2saurabh_565Оценок пока нет

- Bank of America V Associated Citizens Bank (Lacurom)Документ2 страницыBank of America V Associated Citizens Bank (Lacurom)Kako Schulze Cojuangco100% (1)

- Car Owner's Guide and Automotive NewsДокумент12 страницCar Owner's Guide and Automotive NewsNDD1959Оценок пока нет

- 10 - Chapter 2 - Background of Insurance IndustryДокумент29 страниц10 - Chapter 2 - Background of Insurance IndustryBounna PhoumalavongОценок пока нет

- Hsslive-Chapter 12 Not For Profit OrganisationsДокумент7 страницHsslive-Chapter 12 Not For Profit OrganisationsChandreshОценок пока нет

- Key Fact Statement For Deposit Accounts: To OpenДокумент4 страницыKey Fact Statement For Deposit Accounts: To OpenMaqsood akhtarОценок пока нет

- Statement of Account: Transaction Amount Balance Transaction Details Transaction DateДокумент5 страницStatement of Account: Transaction Amount Balance Transaction Details Transaction DatehyhОценок пока нет

- Consolidated Digest of Case Laws Jan 2013 March 2013Документ179 страницConsolidated Digest of Case Laws Jan 2013 March 2013Ankit DamaniОценок пока нет

- Account Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницAccount Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceParveen SainiОценок пока нет

- Last Minute Tax TipsДокумент2 страницыLast Minute Tax TipsIncome Solutions Wealth ManagementОценок пока нет

- Asian CurrencyДокумент62 страницыAsian CurrencyDemar DalisayОценок пока нет

- TIM101Документ5 страницTIM101coffeepathОценок пока нет

- BillДокумент11 страницBillKat SriramОценок пока нет

- Manufacturers Vs MeerДокумент4 страницыManufacturers Vs MeerAlandia GaspiОценок пока нет

- 1554382617CA Final Audit MCQ BookletДокумент72 страницы1554382617CA Final Audit MCQ BookletLakshay SinghОценок пока нет

- STMNT 112013 9773Документ3 страницыSTMNT 112013 9773redbird77100% (1)

- BibliographyДокумент8 страницBibliographySachin B BarveОценок пока нет

- Mode of OperationsДокумент5 страницMode of OperationsArchana SinhaОценок пока нет

- FinanceДокумент24 страницыFinanceRajendra LamsalОценок пока нет